designer491/iStock via Getty Images

Introduction

These selections continue as ongoing tests and active portfolios for members looking for value stocks using one of the best fundamental value models in peer-reviewed financial literature with additional customized enhancements. The schedule of portfolio selections, research analysis, and the 2023 forecast article for members are available here:

Top Forensic Value Stock Selections: Highest Positive & Negative Scoring Stocks For January 2023

This quantitative study continues a series of multi-year tests now using the top four forensic algorithms applied to detect bankruptcy risk, earnings manipulation, and financial irregularities. This forward testing study makes portfolio selections from the highest positive and highest negative scoring stocks across the U.S. stock exchanges to measure performance variances between portfolios and benchmark indexes.

The different algorithms created by Beneish, Ohlson, and Altman are well documented from financial literature and rely exclusively on fundamental data including year over year operational performance measures. The combination of all three bankruptcy and financial irregularity algorithms creates a unique “deep dive” on key value characteristics and applies a total of 22 different fundamental financial variables for assessment. The newest addition of the Montier C-Score began in August 2020 and now increases the total combination of accounting variables to 28 across all four algorithms.

Frequently Asked Questions

1. Why would the negative forensic stocks perform well if they are the top outliers for negative forensic characteristics?

Enron was a top negative forensic stock that rapidly gained over 600% in a few years before whistleblowers finally revealed the financial irregularities that eventually led to bankruptcy. Extreme forensic outliers can be products of incredible positive growth conditions or financial irregularities that have not been addressed. In either case, the stock price has proven to benefit greatly over significant periods of time.

bigcharts.marketwatch.com

2. Why would the positive forensic stocks perform well with outliers in positive conditions across all the forensic characteristics?

Stocks with extremely favorable forensic scores are likely to have excellent operations, strong stable financial ratios, solid fundamental valuations and attract premium pricing from investors. These stocks may have attractive low valuations as a result of receiving less hype, less glamorous operations, or out of favor industries that are still going strong.

Examples of Forensic Algorithm applications

Prior examples of the application of these forensic financial algorithms can be found in my published articles and interviews:

Prior articles and published references detail the composition and methods of each of the forensic algorithms used in this article. For simplicity, here is a summary of what each of the forensic algorithms used by fraud examiners and investigators scan for at high levels:

- The Beneish model uses eight variables to detect earnings manipulation. Created by Professor Messod Beneish, an M-Score greater than -2.22 signals that the company is likely to be a manipulator.

- The Altman model is used to predict whether a firm is likely to go into bankruptcy within 2 years and uses many variables from the income and balance sheets for this analysis. Distress is considered high with a value below 1.81.

- The Ohlson model also predicts bankruptcy risk using a multi-factor financial algorithm developed by Dr. James Ohlson in 1980. Any percentage values above 50% indicate the risk of a firm’s bankruptcy within 2 years.

- Lastly, James Montier developed a C-Score that creates a simple scoring system to highlight firms that may be “cooking the books” with values above 4 being at risk firms.

The firms listed below for negative scoring all qualified in the high adverse levels for each of the forensic models described above. The positive scoring stock selections have the lowest or most favorable combined values of the forensic scores across the US exchanges.

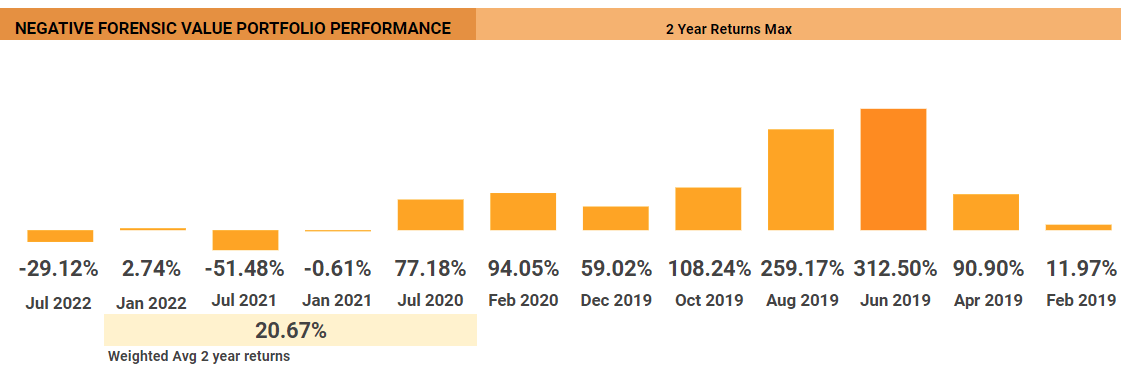

Prior Negative Forensic Returns

2022 delivered the worst half-year start to the stock market since 1970 and the worst full-year returns since 2008. Those who followed the Momentum Gauges® to avoid record downturns further enhanced these portfolio returns.

FinViz.com

Despite these large market downturns, the Negative Forensic value portfolios have a two-year weighted average return of +20.67% NOT including large dividends.

2022 End of Year Returns – Negative Forensic

Portfolios are measured for 2 years with current returns, average weighted returns, and peak gains tracked on the V&M Long Term Dashboard.

VMBreakouts.com

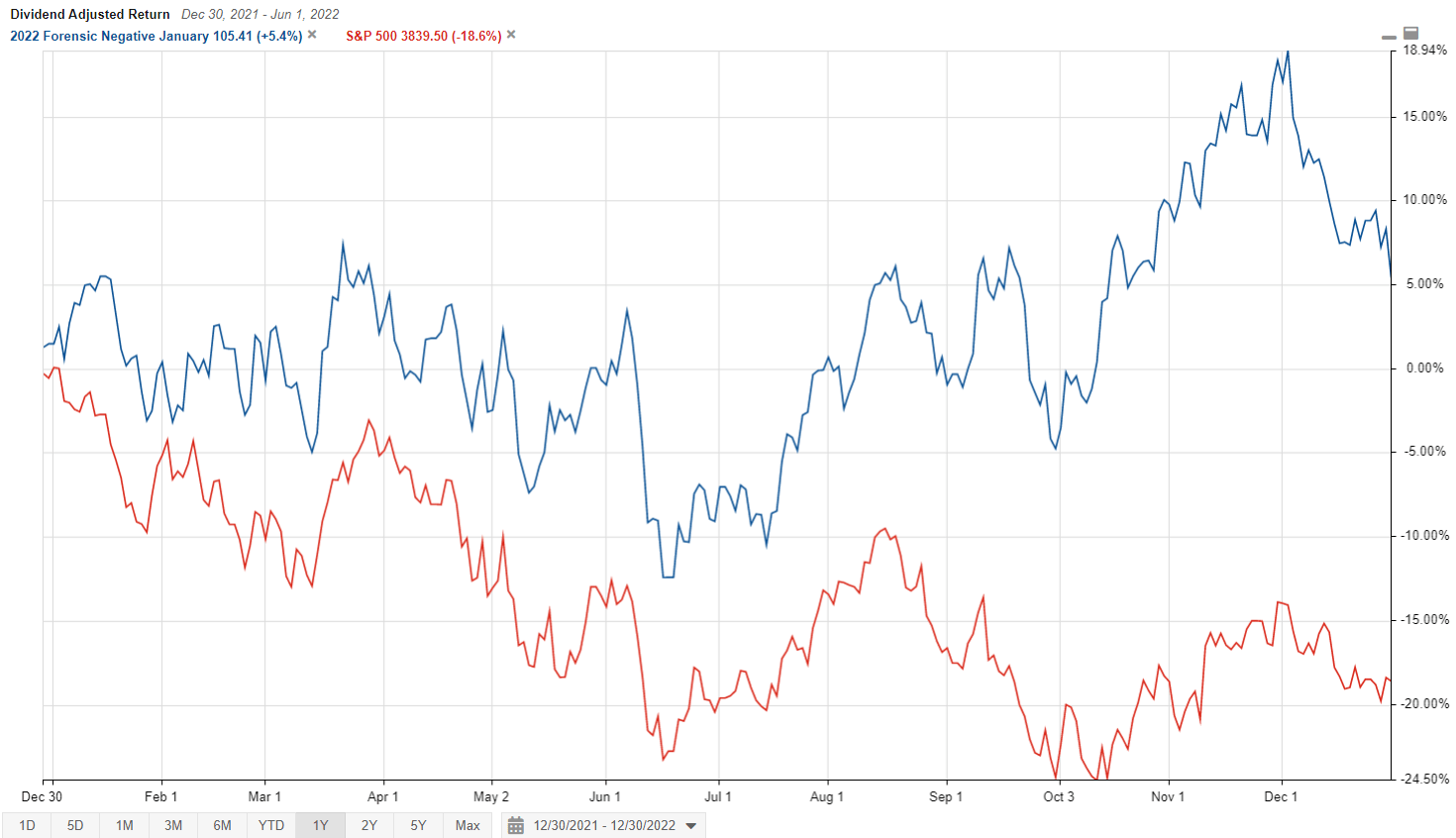

January Dividend Adjusted Returns vs. S&P 500

The January Negative Forensic portfolio 1-year dividend adjusted returns are up +5.4%, peaking in early December at +18.94% near the negative Momentum Gauge signal on December 5th. The total return Negative Forensic portfolio beat the S&P 500 (SPY) (SP500) by +24.84% in 2022.

StockRover.com

Members have smartly asked me to delay selections until the Momentum Gauges turn positive again for the best results. Regrettably, I am not trying to time selections just for the best returns, but focused on consistent release and testing of these portfolios through the worst market conditions. Rather I would suggest you consider making your own entry timing using Momentum Gauges when they turn strongly positive again.

January 2023: Negative Forensic Value Enhanced Selections

Out of more than 8,000 stocks screened for January 2023 there were only eight highly adverse scoring stocks across each of the four forensic algorithms. This is down significantly from 35 adverse stocks in July 2022 and may reflect lower levels of financial distress. By that I mean that fewer warning signals are turning up suggesting conditions are not as bad as they had been in the Covid years.

| Date of Search | Number of highly adverse stocks |

| January 2023 | 8 |

| July 2022 | 35 |

| January 2022 | 21 |

| July 2021 | 41 |

| January 2021 | 187 |

| February 2020 | 11 |

| December 2019 | 6 |

| October 2019 | 7 |

| August 2019 | 9 |

It is very likely the impact of the global pandemic caused the significant increase in highly negative forensic scoring stocks between July of 2020 to January 2021. The number of negative scoring stocks is dropping off again toward pre-pandemic levels with fewer extremely adverse stocks. The top 10 highest negative results for January are sorted along the Ohlson O-score probability percentage in descending order.

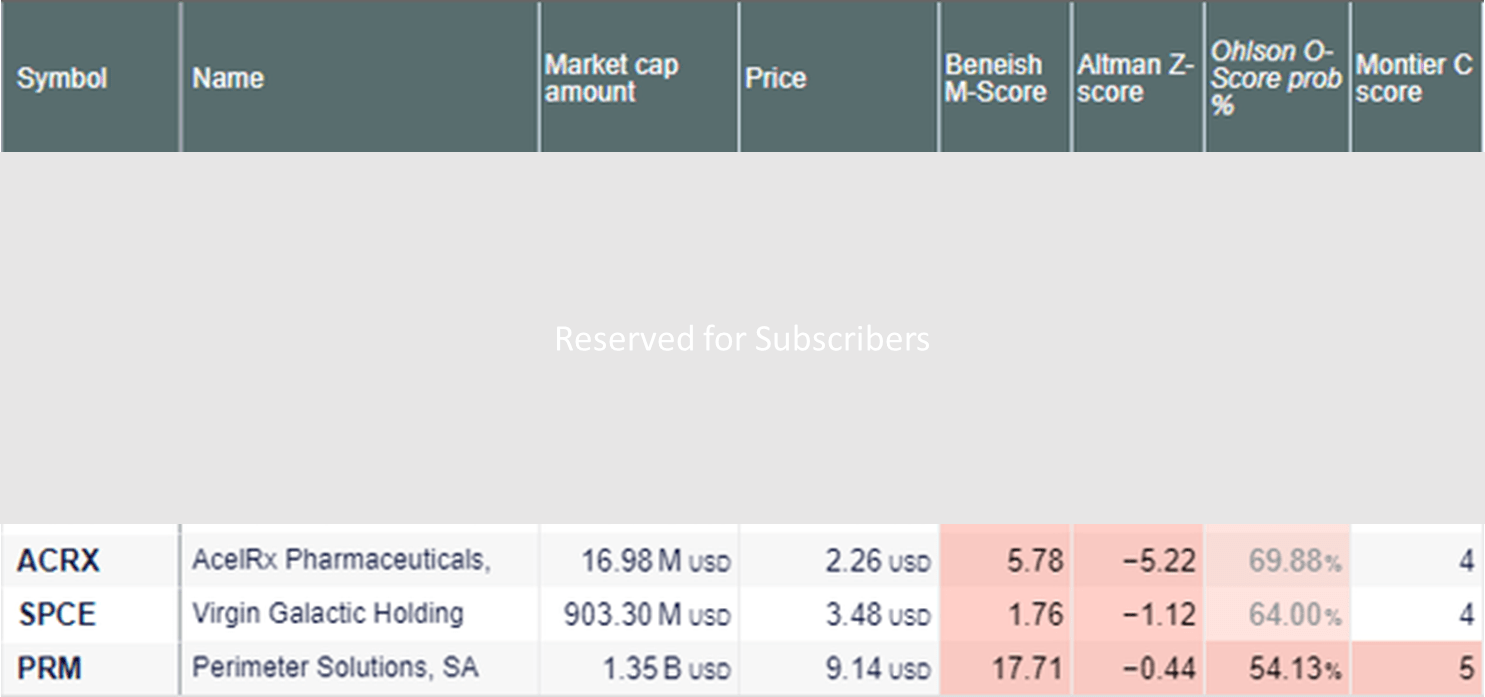

Top Negative Forensic stocks for January 2023

UncleStock

Overall Scores Independent of the Negative Forensic Selections

An independent ranking of these firms using other value and growth scores is shown below that may provide additional insight into the risk of these firms.

StockRover.com

Morningstar Financial Health Grade

StockRover.com

These highly negative forensic stocks seem unlikely to perform well based on fundamental analysis and the red flags of four different forensic algorithms. However, as we can see from several years of past performance the results have produced above average market performance, even beating the major benchmarks the last 6 years.

Prior Positive Forensic Returns

2022 delivered the worst half-year start to the stock market since 1970 and the worst full-year returns since 2008. Those who followed the Momentum Gauges® to avoid record downturns further enhanced these portfolio returns.

FinViz.com

Despite these large market downturns, the Positive Forensic value portfolios have a two-year weighted average return of -13.45% NOT including large dividends.

2022 End of Year Returns – Positive Forensic

Portfolios are measured for 2 years with current returns, average weighted returns, and peak gains tracked on the V&M Long Term Dashboard. Because at least two of the forensic algorithms in the published financial research used 2-year models we will also follow at least 2 years of returns from these portfolios as shown below:

VMBreakouts.com

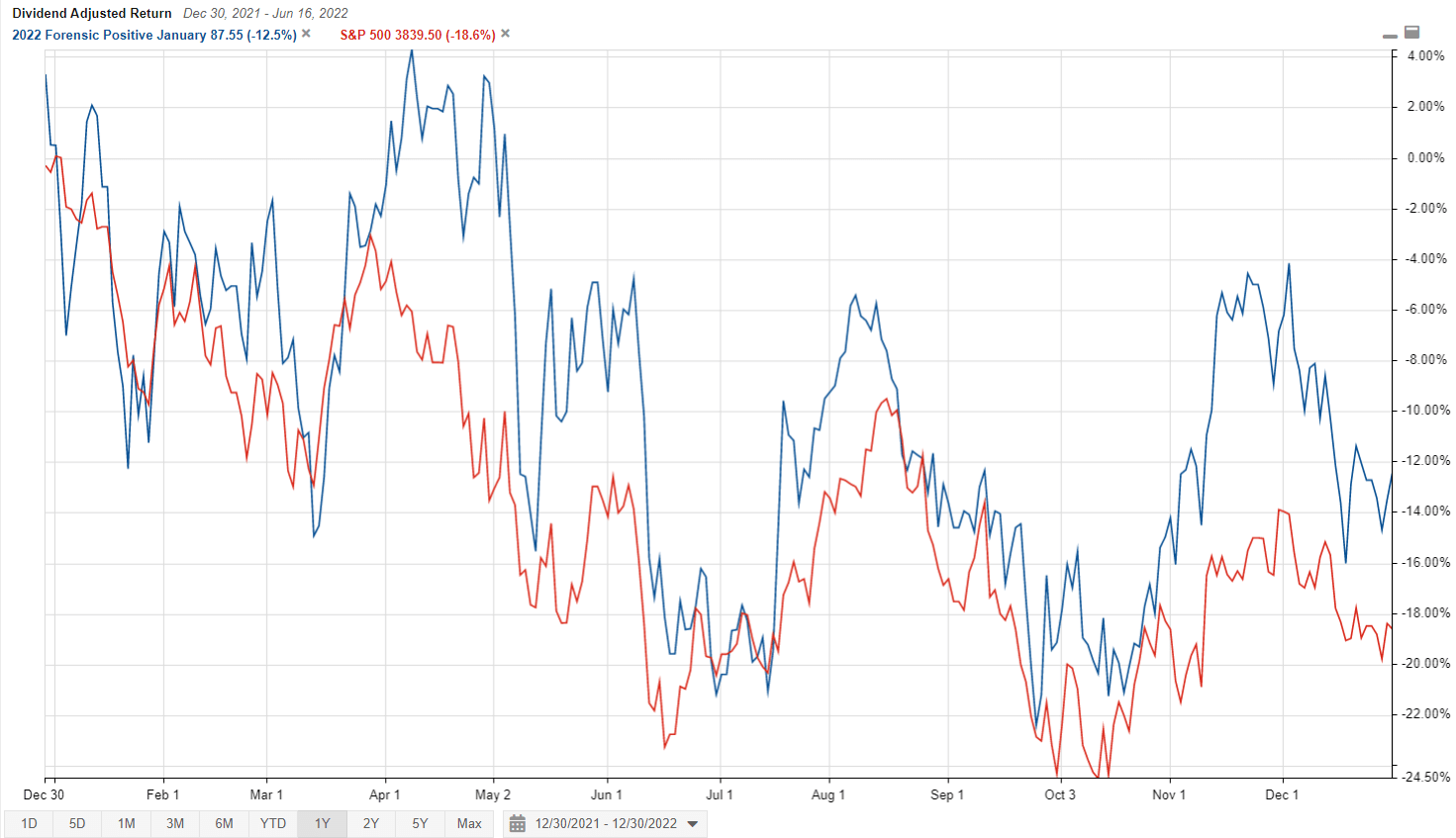

January Dividend Adjusted Returns vs. S&P 500

The January Positive Forensic portfolio 1-year dividend adjusted returns are down -12.5% peaking in early April at +4.27% near the negative Momentum Gauge signal on April 5th. The total return Positive Forensic January portfolio beat the S&P 500 by +6.94% in 2022.

StockRover.com

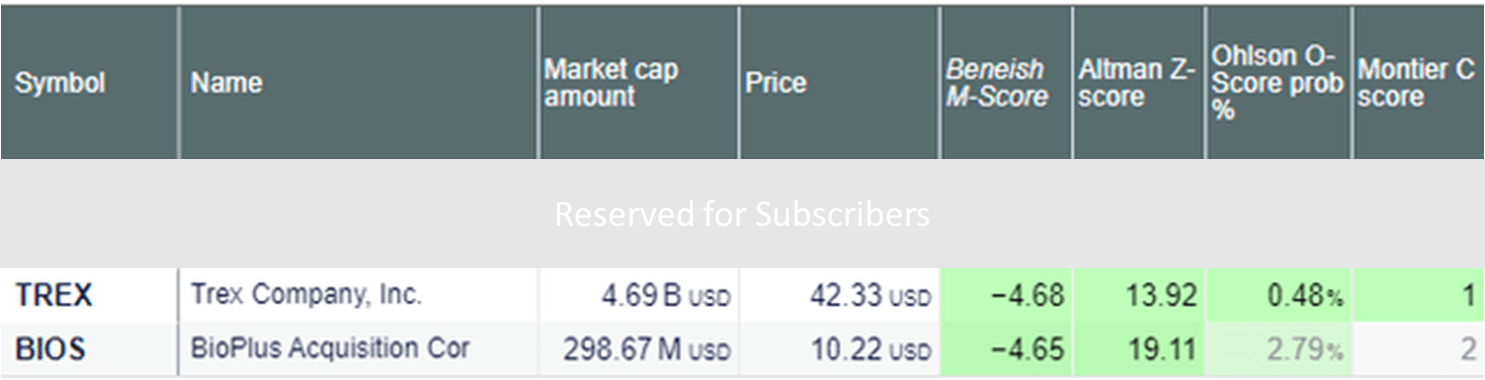

Out of more than 8,000 stocks screened across all the US exchanges, only 4 stocks qualified as highly positive across all the forensic algorithms for low risk of bankruptcy or financial irregularities. Most years the selections are fewer than 10 and this is a particularly small qualifying group. It is typical for there to be fewer qualifying positive than negative forensic stocks across all the algorithms. The Beneish model is the only forensic algorithm tested in peer reviewed literature that shows higher performance results. As a result the four qualifying stocks sorted by the most favorable Beneish M-score are as follows:

January 2023: Positive Forensic Value Enhanced Selections

UncleStock

These forensic scores do not necessarily forecast stock price growth. It would seem likely that stocks with low risk of bankruptcy, low probability of corporate distress, low chance of earnings manipulation, and low probability of financial irregularities on deep fundamental analysis should provide a safer value proposition for investors going forward. Prof. Beneish has documented positive returns from a favorable M-score in his research.

Overall Scores Independent of Top Forensic Algorithms

An independent ranking of these firms using other value and growth rankings is shown below that may provide additional insight into the risk of these firms.

StockRover.com

Morningstar Financial Health Grade

StockRover.com

Positive Forensic Charts

BioPlus Acquisition (BIOS)

FinViz.com StockRover.com

StockRover.com

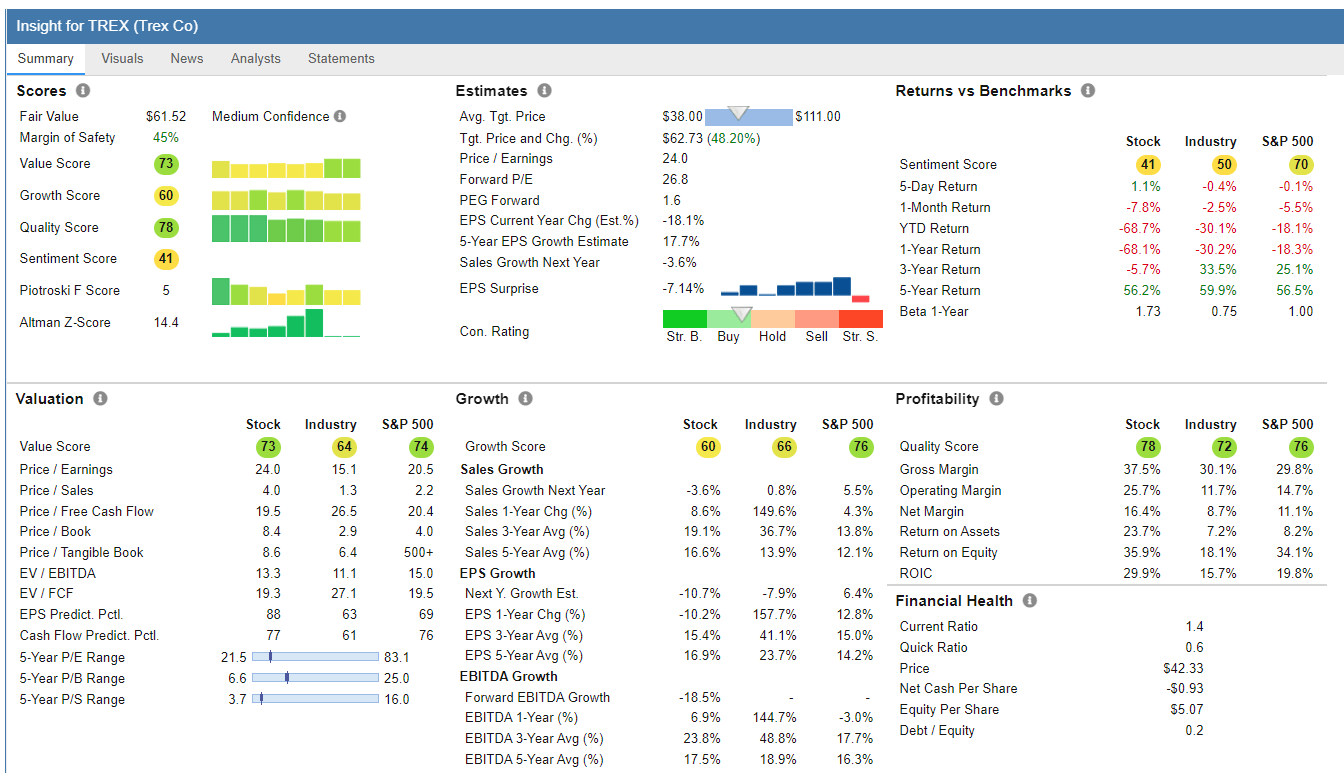

Trex Co. (TREX)

FinViz.com StockRover.com

StockRover.com

Methodology Review

The purpose of this multi-year forensic analysis study is to provide investors with additional tools to evaluate financial irregularities according to four different detection models from academic research. Circumstances surrounding firms are always subject to change, open to extenuating circumstances, and models by their very nature always contain a degree of error.

Again, it is important to stress that firms identified by these academic models may not be in actual distress or suffer from any adverse irregularities whatsoever. These models are certainly not foolproof and were designed by academic researchers to improve the chance of detection of irregularities leading to bankruptcy, earnings manipulation, or flag the presence of financial distress.

At the same time, these models are among the best peer-reviewed forensic models in the financial literature and have some significant documented value.

The Beneish model for example has “correctly identified, in advance of public disclosure, a large majority (71%) of the most famous accounting fraud cases that surfaced after the model’s estimation period” (Beneish, Lee, & Nichols, 2013, p. 57).

Further, in a survey of 169 chief financial officers of public companies, Dichev, Graham, and Rajgopal (2012) reported that respondents estimated that approximately 20% of all companies manage earnings to misrepresent economic performance. While three different financial forensic models are applied in the selection of these portfolios, researchers associated with testing the M-score described their approach this way:

Our main hypothesis was that companies that share traits with past earnings manipulators (i.e., those that “look like manipulators”) represent a particularly vulnerable type of growth stock. Because of their strong recent growth trajectory, these companies are likely to be more richly priced. At the same time, they exhibit a number of potentially problematic characteristics, indicative of either lower earnings quality or a more challenging economic environment. Although the accounting games such companies engage in might not be serious enough to warrant legal action, we posited that their earnings trajectory is more likely to disappoint investors (i.e., they have lower earnings quality)”

(Beneish, Lee, & Nichols, 2013, p. 57).

To my knowledge no similar longitudinal study of positive and adverse forensic scoring using all three models simultaneously has ever been conducted before. It is also important to constructively consider why such anomalies may exist in these stock selections at this moment in time. The resulting data which varies from month to month may prompt firms and investors to consider further due diligence of publicly available financial characteristics to mitigate any risk or error present in the marketplace.

Conclusion

44 forensic portfolios (22 positive forensic value / 22 negative forensic value) have been formed for evaluation since the testing period began in July 2017.

Over multiple one-year test periods, we are seeing strong differentiation in results between negative and positive forensic portfolios. Most notably delistings of stock symbols (merger, acquisition, leaving the exchange) are approximately 10x higher among negative forensic stock selections than for positive forensic stocks. Over the years, we see that price behavior is more stable among individual positive selections, but that greater returns are coming from the negative portfolios. In several years with nearly 30% better average returns across eight portfolios. Overall, the negative forensic stocks are producing higher returns, with larger variability and at a much higher rate of mergers/delisting.

In prior years of this study, these portfolio selections were made every 2 months. The overlap of selections was found to be quite high for these long term portfolios. Now the selections are made every six months with a minimum 2-year measurement period and there are still overlapping stocks from prior selections. Prior tests in the literature of the Beneish M-score have shown the algorithm to generate excellent results on an annual basis for positive scores. The tests continue and more explanations may develop over time.

I trust this research and stock selections will give you added value to your investment goals and returns in 2023!

JD Henning, PhD, MBA, CFE, CAMS

References

Altman, E. I. (1968). The Prediction of Corporate Bankruptcy: A Discriminant Analysis. The Journal of Finance, 23(1), 193–194. doi:10.1111/j.1540-6261.1968.tb03007.x

Beneish, M. D. (1999). The Detection of Earnings Manipulation. Financial Analysts Journal, 55(5), 24–36. doi:10.2469/faj.v55.n5.2296

Beneish, M. D., Lee, C. M. C., and Nichols, D. C. (2013). Earnings Manipulation and Expected Returns. Financial Analysts Journal, 69.2, 57-82.

Ohlson, J. A. (1980). Financial Ratios and the Probabilistic Prediction of Bankruptcy. Journal of Accounting Research, 18(1), 109. doi:10.2307/2490395

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment