Brandon Woyshnis/iStock Editorial via Getty Images

We have previously covered Ford (NYSE:F) and General Motor (NYSE:GM) here as a post-FQ3’22-earnings article in November 2022. Having compared their performance extensively, we concluded Ford may have been the better investment at that time. This is partly attributed to its robust Free Cash Flow generation and forward dividend yields.

For this article, we will focus on the massive tailwind for F’s growth, attributed to the robust consumer demand for F-150 Lightning. Its partnership with multiple battery makers also proves critical to the 2M EV ramp-up through 2026. The alternative factory arrangement with Contemporary Amperex Technology’s [CATL], the largest global battery manufacturer, may eventually result in the latter bringing the Qilin technology to the US. These strategies may boost the stock closer to the consensus price target of $18.50, partly attributed to the new technology’s doubled battery capacity.

The F-150 Lightning Investment Thesis Is Still Robust

The Ford F-150 Lightning needs no introduction, seeing that it recently won Motor Trend’s Truck of the Year award, beating out several other popular pickup trucks. It is no wonder since the F-150 model remains America’s best-selling vehicle for the 40th straight year and the industry’s top-selling truck for the 46th consecutive year in 2022.

As a testament to the insatiable consumer demand, F has added the third shift to the Michigan plant to expand its annual F-150 Lightning output to 150K units by Q3’23. These numbers are impressive indeed, since it indicates a remarkable ramp-up of 272.7% from its initial plans of 55K units by 2023. In addition, we must highlight the tremendous price hikes of 40% thus far, from the introductory debut price of $40K to $56K by December 2022, attributed to the rising inflationary pressure across labor and material costs.

We reckon that there is little to moderate risk for the automaker now, since the F-150 Lightning’s MSRP remains well below the $80K cutoff point to qualify for the $7.5K IRA tax credits. On the other hand, the consumer index for new vehicle sales has notably moderated sequentially from 0.7% in September to 0.0% in November 2022, potentially attributed to reduced discretionary spending during worsening macroeconomics. Depending on how the situation develops over the next few quarters, we may see a deceleration in consumer trend, triggering further headwinds in F-150 Lightning demand ahead, despite the supposed pre-order volume of 200K as of December 2022. Even TSLA had to extend its $7.5K credit for Model S and X pre-orders to boost sales in the US, suggesting slowing market demand.

However, we are confident about F’s forward execution over the next few years, due to the robust $50B investment through 2026. As a result of its expanded partnership with long-term battery suppliers, SK Innovation and LG Energy Solution, over 70% of its battery capacity for over 2M electric vehicles has already been secured. In addition, it seeks to manufacture up to 180 GWh of batteries in the US under BlueOval SK, a joint venture with SK On. Raw materials will also be sourced from trade-friendly countries, such as Australia and Indonesia, attributed to the IRA tax credits.

Due to the worsening geopolitical relationship between the US and China, F is also reportedly exploring an alternative arrangement to qualify CATL battery under the IRA tax credits. According to market rumors, F is considering an unconventional plant and infrastructure ownership in Virginia, while allowing the battery maker to operate the factory according to its LFP battery technology. However, as CATL noted in an emailed statement, it is unclear how the new battery plant will be structured:

CATL is still deliberating on investing in the US and we have not made the decision yet. There are multiple models being discussed regarding our investment in the US, and all of those choices are purely based on and only based on business concerns. (Bloomberg)

Ford’s EV Sales By 2023

Ford

These strategies may aid F in achieving impressive 600K EV sales by FY2023, increasing by nearly 6-fold from the FY2022 projection of 101.85K. Notably, the sales for Mustang Mach-E are expected to grow tremendously by 337.5%, Ford E-Transit by 2,321.9%, and the F-150 Lightning by 979.1% YoY. In addition, it expects to launch and sell up to 30K units of a new mid-sized SUV model for the fiscal year. Impressive indeed, despite the supposed 70% chance of a recession in 2023 and GM’s cautious commentary thus far.

An Expanded Battery Capacity May Boost F-150 Demand Tremendously

CATL has announced a new battery for electric vehicles called the Qilin Battery, which may offer up to 620 miles per full charge, increasing tremendously by 258.3% against the basic battery used by F-150 at 240 miles and by 93.75% against the extended battery at 320 miles. It is also interesting to note that the new battery would outperform Tesla’s (TSLA) 4680 cells by 24%, with the latter offering a range of up to 500 miles per full charge. Most importantly, the battery boasts the highest volume utilization of EV batteries at 72% against the previous 50% and a rapid charging technology within ten minutes.

In addition, the CATL management hinted at developing a five-minute charging technology for up to 80% battery capacity, indicating massive tailwinds for global adoption. These numbers suggest a tremendous improvement from market standards of up to fifteen minutes through Level 3 charging, six hours through Level 2, or 40 hours through Level 1. For example, a TSLA Model Y owner with the new 4680 battery pack has reported that it took approximately an hour to reach 97% charge.

Based on CATL’s new Qilin NMC battery system (speculatively lithium, manganese, and cobalt oxide), we are looking at a tremendous energy density of up to 255 Wh/kg, compared to 160Wh/kg for Qilin’s LFP battery systems. In addition, the Qilin batteries will offer a service life of up to 1.24M miles or the equivalent of sixteen years, against the standard LFP of ten years. According to market reports, these batteries will go into mass production by early 2023, potentially driving up global demand. However, the $7.5K IRA tax credit will likely dampen domestic demand, due to its impact on the non-domestic supply chain.

That is a shame, since the F-150 Lightning would likely benefit from the breakthrough Qilin technology. Due to the vehicle’s bi-directional charging capability, drivers may utilize its battery as a stationary power source for multiple home or work uses. The new CATL technology will come in handy during a time of power outage or severe storms, such as one currently witnessed in various states within the US. The majority of drivers have already suggested ditching generators at their work sites to run power tools from the electric truck.

While some drivers have complained about F-150 Lightning’s towing capabilities, Qilin’s expanded capacity would lift most of those headwinds. Early tests have shown that the vehicle only offered up to 90 miles in range while towing trailers, which is lacking compared to the 200 miles offered by the F-150’s ICE equivalent. However, the new technology offered by CATL may push this boundary, more than doubling the F-150 Lightning’s towing mileage, matching its predecessor. Combined with the company’s partnership with Qualcomm (QCOM) and AT&T (T) on the F-150 Lightning and the 2023 Super Duty, F may also offer improved 5G connectivity on their EVs’ dashboard nationwide, due to the telecom’s aggressive expansion thus far.

Although it remains to be seen how the partnership between F and CATL will be forged, we are hopeful that a workaround will allow both companies to innovate in the US. Taking this into account, we may see the automaker produce over 2M electric vehicles by 2026, while simultaneously debuting a cutting-edge battery range in the domestic market.

So, Is F Stock A Buy, Sell, or Hold?

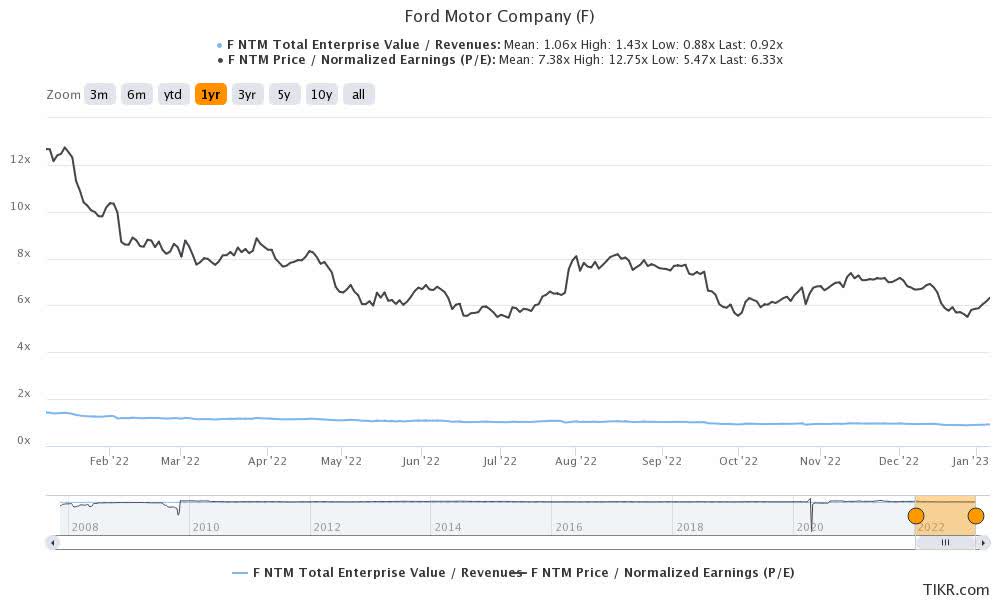

F 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

F is currently trading at an EV/NTM Revenue of 0.92x and NTM P/E of 6.33x, lower than its 3Y pre-pandemic mean of 1.16x and 7.12x, respectively. Otherwise, it is still moderated from its 1Y mean of 1.06x and 7.38x, respectively.

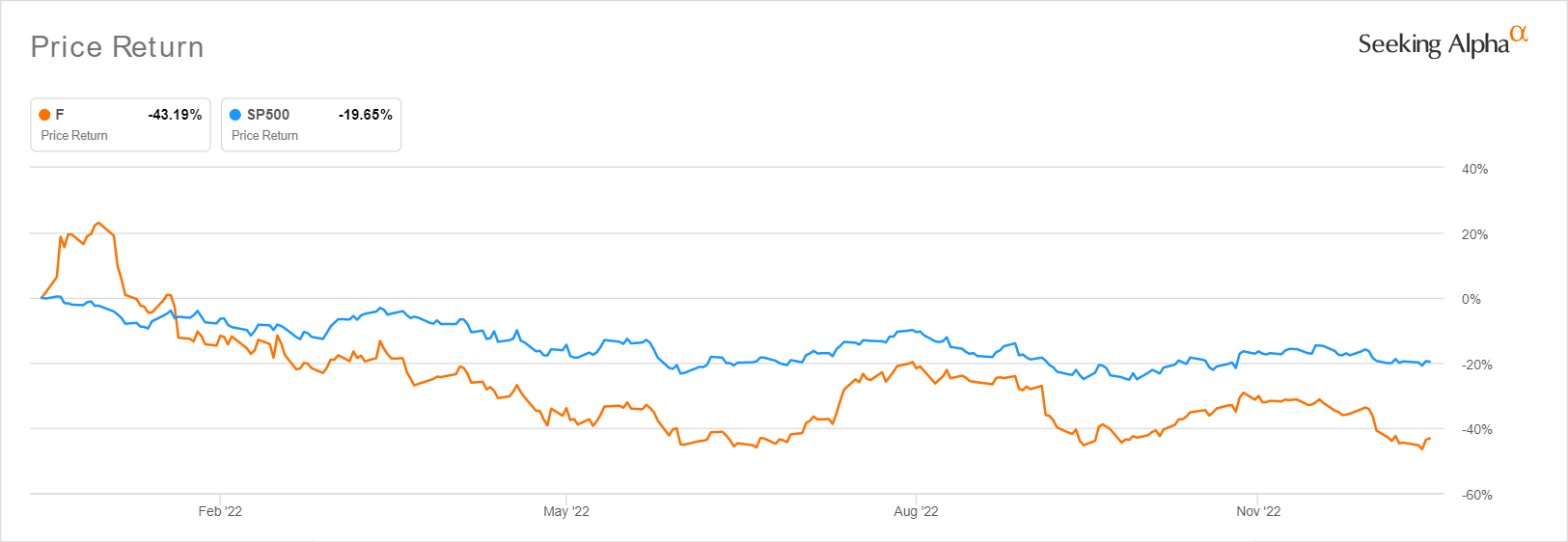

F 1Y Stock Price

Seeking Alpha

Based on F’s projected FY2025 EPS of $2.09 and current P/E valuations, we are looking at a moderate price target of $13.22. However, we concur with the consensus estimate’s more bullish target of $18.50, suggesting a 47.06% upside potential from current levels. Those pessimistic valuations were mainly attributed to Mr. Market’s pessimism about the worsening macroeconomics, with many other automakers impacted as well. General Motors and TSLA are also trading below their 3Y pre-pandemic and 1Y means, with their stock prices similarly compressed.

Once market pessimism lifts, we may potentially see the F stock’s valuation recover to its normalized P/E mean of 7.5x, nearing the normalized automotive market mean of 7.02x. This implies a price target of $15.67 and an improved upside potential of 24.56%. The upward rerating may eventually occur once the company reports expanded profit margins from its raised prices all-around, once the rising inflation is successfully tamped down to the Fed’s target of 2% by 2024. Market analysts are already projecting the increase in its FY2025 EBIT/ net income/ FCF margins by 2.9/ 1.8/ 3.1 percentage points compared to FY2019 levels. This will further supplement the company’s robust balance sheet of $31.9B of cash/investments in the latest quarter, suggesting an excellent automaker net debt level of -$12.9B.

Naturally, the automaker may also lower the MSRP accordingly at that time, depending on market demand. However, we choose to be more optimistic, since the F-150 model remains one of the most well-loved American vehicles thus far, suggesting the sustained forward demand through the company’s electrification efforts. Despite the volatile stock market, these levels already provide an attractive risk/reward ratio with an improved margin of safety.

Therefore, we continue to rate the F stock as a Buy, especially since market analysts project dividend payouts of up to $0.64 by FY2025, suggesting an expanded yield of 5.5% then, compared to the 4Y average of 3.86% and sector median of 2.12%. These numbers may help temper some of the stock’s volatility over the next few quarters, before the Feds reduce interest rates, possibly triggering the recovery of a bull market over the coming decade.

Be the first to comment