Electric Ford Mustang Mach-E RoschetzkyIstockPhoto/iStock Editorial via Getty Images

Ford Motor Company (NYSE:F), the third-largest automaker in the U.S. by vehicle sales, posted a 4.8% drop in fourth-quarter vehicles sales – and a 2.2% drop in 2022 – closing out a year that turned out to be the weakest in more than a decade for the entire industry.

Reducing some of the sting, Ford was able to grab an additional 0.7% share of the weaker U.S. market, following a 2021 marked by a 6.8% drop in unit sales and a 1.3% loss of market share.

One of the prominent components of Ford’s 2022 U.S. sales volume was its results in selling battery electric vehicle (“BEV”) models, consisting of the Mustang Mach-E, Ford F-150 Lightning, and the E-Transit commercial van, which is not included in the count of passenger vehicles. Ford’s BEV sales more than doubled to 61,575 last year thanks to the F-150 Lightning’s launch and that of E-Transit, which lead their respective light-truck segments.

Mach-E growing

Sales of the electric SUV, Mustang Mach-E, last year increased 45 percent, to 39,458 vehicles. The sales of the three models ratified Ford’s claim that it is now the No. 2 seller of battery-powered vehicles in the U.S., behind Tesla, Inc. (TSLA).

Vehicle unit sales are a critical driver of earnings: fourth-quarter and year-end financial results will be posted on February 2. According to Zacks Investment Research, based on 5 analysts’ forecasts of Ford’s earnings, the consensus EPS forecast for the quarter is $0.59. The reported EPS for the same quarter last year was $0.26.

Retail transaction prices for Ford models were up 11% from a year ago, reflecting a tight inventory of vehicles, to an average of $55,652 for the quarter. Likewise, incentives paid by Ford to close deals were down 49% from a year ago to an average of $1,227 per vehicle.

Cash is key

Ford, which is investing $50 billion on BEVs, relies heavily on current cash flow and profits to finance its migration to the new technology from vehicles powered by internal combustion engines. The automaker’s most important single model for generating cash is the gasoline-powered F-150 full-size pickup truck. December was an excellent month for F-150, due to an improved inventory available to dealers; for the year, however, F-150 retail sales were down 10%.

Although F-150 is the most popular full-size pickup brand in the U.S., it competes with several others from General Motors Company (GM), Stellantis N.V. (STLA), and Toyota Motor Corp. (TM). Eventually, Ford aims for its battery-powered F-150 Lightning to replace the gasoline version as the automaker’s show horse – though when or even if that will happen is unclear.

2021 Ford F-150 pickup (Ford Motor)

In the meantime, Ford – which has virtually eliminated sedans from its lineup – can ill afford its gasoline F-150 to falter, since cash from those sales paves the path to BEVs. According to the Automotive News Research Center, 2022 was the F-150’s weakest sales year since 2012. Ford sold 653,957 F-Series last year, including 15,617 F Series Lightning battery-powered pickups.

I have been cautious on Ford stock, because BEV models – while growing – face serious barriers to mainstream consumer acceptance. Notably, the insubstantial public charging infrastructure, on top of the limited range of most BEV models between charges and premium pricing of new models, means that many consumers will be wary of and may delay switching from gasoline to battery models.

Better days ahead

In time, the BEV charging infrastructure is likely to improve and batteries are likely to charge more quickly – but how quickly those improvements will unfold is difficult to forecast. Less expensive BEV models will be introduced for price-sensitive buyers.

Mercedes charging station (Mercedes-Benz)

On January 5, Mercedes-Benz – noting the lagging buildout of North American charging capacity – announced it will invest billions of euros to build 10,000 of its own branded fast-charging points on the continent. Mercedes will team with MN8 and Charge Point, aiming to operate 400 hubs comprised of 2,500 chargers by 2027.

Tesla already operates its own charging network – and other automakers could follow. In September, Ford told its nearly 3,000 North American retail franchisees they must agree to no-haggle pricing for BEVs and to pay for the installation of charging outlets at their stores in order to qualify to sell new BEV models. As of December, about two-thirds of the dealers had agreed.

Restoration of the dividend in November 2021 was taken as a sign of Ford’s management confidence. Unfortunately, the move coincided with the Federal Reserve’s signal that tighter credit and harder economic times lay ahead. After breaching the $25 a share mark in early January, Ford shares tumbled through July and have wallowed sideways for the past five months, lately hovering between $11 and $16.

Current sentiment on Ford stock reflects polarization, the bulls seeing a breakout driven by BEV sales and the pessimists eyeing the company’s relative lack of financial depth, big capital spending commitment for BEVs and a disproportionate reliance on the future of its large pickup trucks.

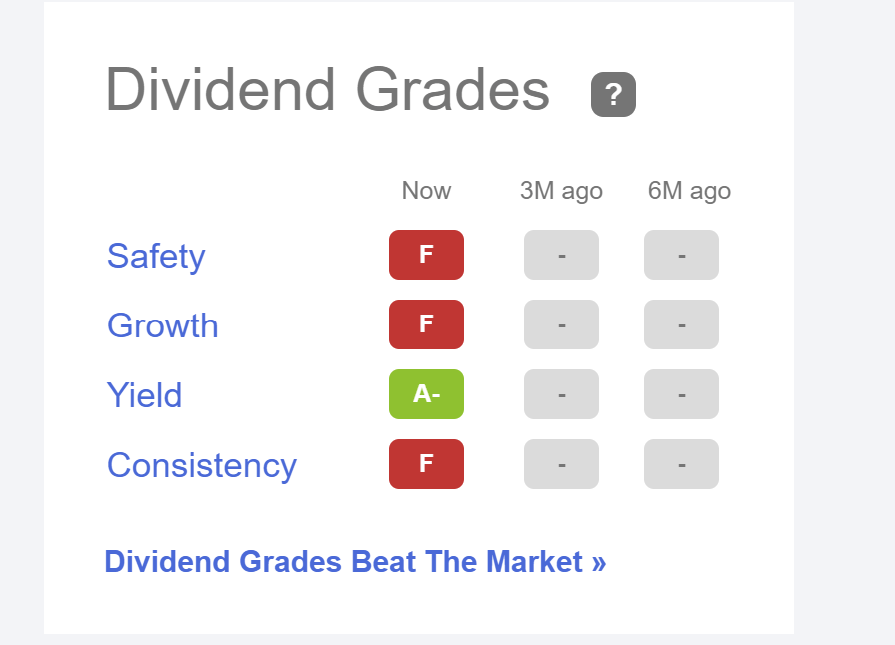

Ford scores a “Buy” Quant rating from Seeking Alpha, based largely on its profitability, which has been improving even while revenue has slowed due to the elimination of underperforming products. Seeking Alpha’s evaluation of Ford stock, however, also includes a flashing-red warning that its dividend is in danger of being cut or omitted.

Dividend warning (Seeking Alpha)

I am in the camp of other Seeking Alpha authors and Wall Street equity analysts, the consensus of which sees Ford Motor Company shares as a hold. The next two years will be consequential as proof for the case that BEVs are headed soon for mainstream adoption – or not. Ford Motor Company has bet big on BEVs; purchasing or adding shares now reflects a conviction that the gamble will pay off.

Be the first to comment