Ford Motor Company (NYSE:F), one of our high-conviction picks at Leads From Gurus, reported Q4 2022 earnings on February 2, sending its shares tumbling in after-hours trading. The events surrounding the earnings report have got many investors scratching their heads, including yours truly. Last Friday, Ford stock dipped 10% at one point before recovering to end the day down 7%, and this market reaction had a lot to do with both disappointing earnings and surprising comments made by CEO Jim Farley. To make matters worse, some Wall Street analysts downgraded Ford as well, including Deutsche Bank analyst Emmanuel Rosner who slashed the price target for Ford from $13 to $11. In this analysis, I will share my thoughts on a couple of surprising developments that came to light with the recent earnings announcement.

wellesenterprises

Leaving Profits On The Table

CEO Jim Farley started the earnings call by saying Ford left $2 billion in profits on the table. This not only came as a surprising remark to many investors but also caught analysts off-guard.

I’ll start by addressing the obvious. Our fourth quarter and full-year financial performance last year fell short of our potential. And while we generated record cash flow, we left about $2 billion of profit on the table due to cost and especially continued supply chain issues. These are the simple facts and to say I’m frustrated is an understatement because the year could have been so much more for us at Ford. – Jim Farley

Ford was one of the hardest-hit U.S. automakers from the global supply-chain crisis in 2021, and these challenges continued throughout 2022 although many of its peers recovered from the crisis comparatively better. As an investor, it would be easy to dismiss these remarks by putting the blame on supply-chain issues, but in reality, Ford’s failure in dealing with supply-chain challenges seems to have stemmed from operational and structural inefficiencies that have existed for many years.

According to CEO Farley, Ford’s business transformation is centered around two distinct objectives.

- Transforming the industrial system (product development, manufacturing, and supply chain management).

- Achieving growth.

Although Ford has been firing on all cylinders to achieve growth through electrification and new software (such as autonomous driving systems and in-vehicle software), the company has found it difficult to transform its industrial system, according to Mr. Farley. The CEO seemingly has nothing to hide and claims that the industrial transformation has been difficult because of deeply rooted “dysfunctionalities” that have existed for many years.

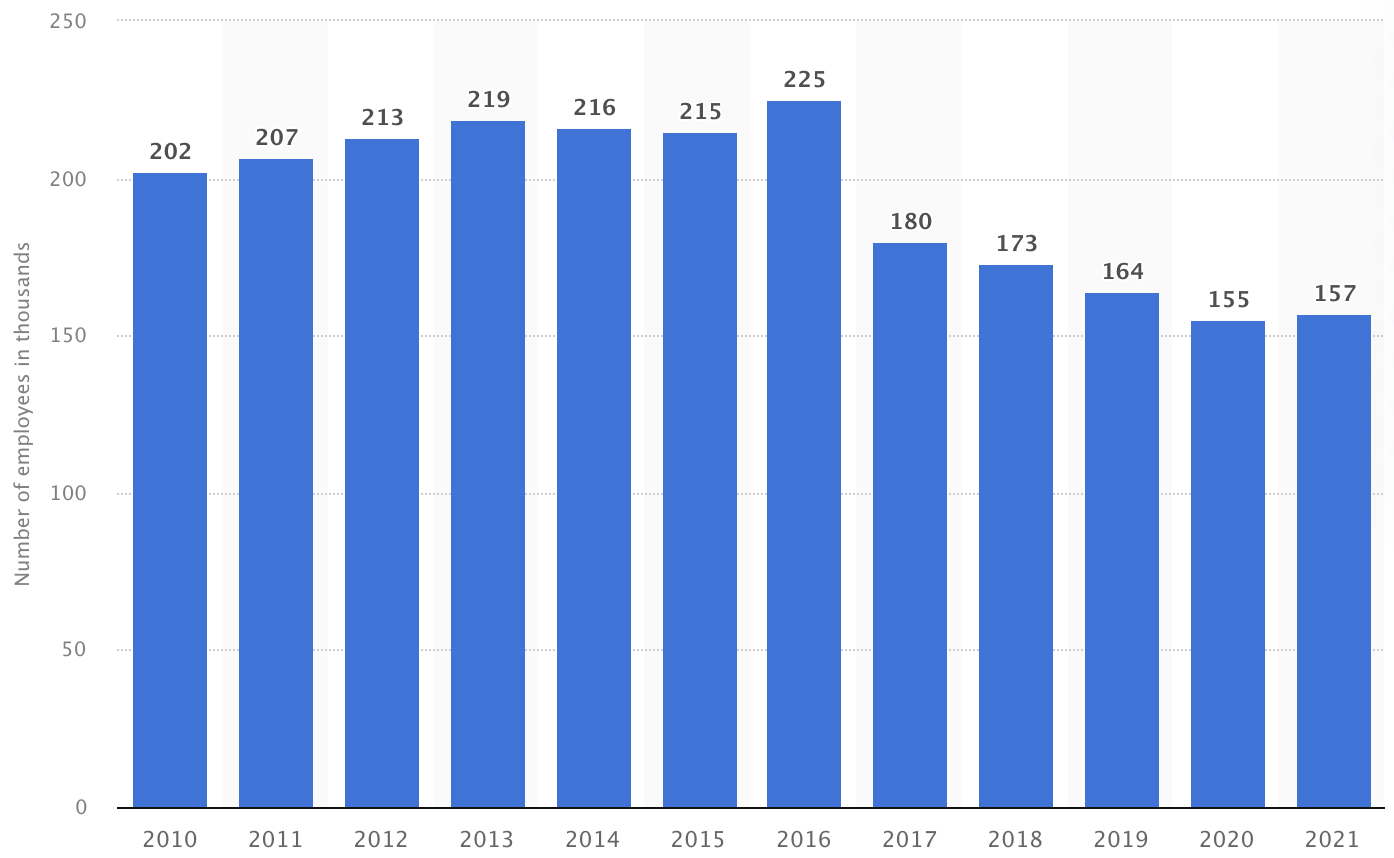

One of these dysfunctionalities, in my opinion, is Ford’s late reaction to macroeconomic shifts in the auto industry. Ford’s arch-rival, General Motors Company (GM), has used a different approach since 2015 under the leadership of CEO Mary Barra to rightsize the company and improve operational efficiencies. General Motors has reduced its headcount meaningfully in the last 8+ years, and this was a strategic decision to allocate resources to the company’s new priorities at a time when the auto industry was changing dramatically.

Exhibit 1: Number of General Motors employees

Statista

Source: Statista

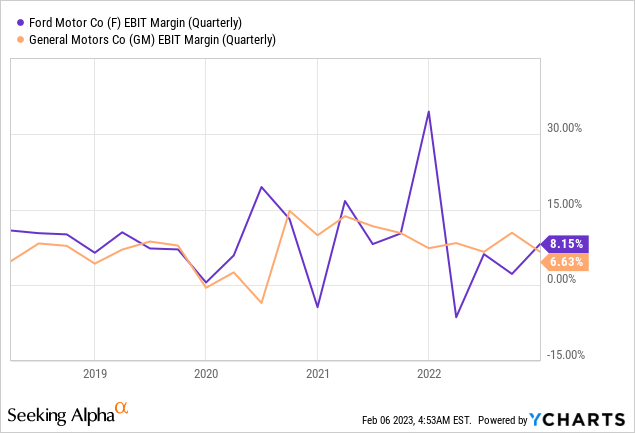

Ford was not as lean as General Motors going into supply-chain challenges that came to light in 2021, and this resulted in a larger-than-expected hit on its operating margins. As illustrated below, Ford’s margins nosedived last year while General Motors fared much better.

Exhibit 2: EBIT margin comparison between Ford and General Motors

One thing that I appreciate as an investor is how CEO Farley has been forthcoming and transparent about the difficulty in transforming the business. Acknowledging these challenges is the first step toward overcoming them, but actions do speak louder than words, and investors will have to patiently wait a few more quarters to see whether there will be any material improvements.

Ford’s Supplemental Dividend

Ford’s quarterly dividend of 15 cents per share yields a handsome 4.5% today, and for me, this is an acceptable return for holding Ford stock until its restructuring plans deliver desired results. The company announced a supplemental dividend of 65 cents per share last week to distribute the cash proceeds from the liquidation of Rivian Automotive, Inc. (RIVN) stake. As a growth-oriented investor, I prefer companies that pump retained earnings (and gains from investments) back into the business when a dollar invested back in the business is likely to be worth more than a dollar distributed to shareholders, in the long run.

Ford is not a young business. The company had more than $32 billion in cash at the end of 2022, and this massive liquidity allows Ford to reward shareholders with dividends today. However, a closer look at the company’s cash flow profile and investment targets reveals Ford needs to be cautious about payouts.

Ford plans to invest $50 billion in EVs through 2026. That would come to approximately $12.5 billion/year from 2023 onwards. At the current rate, Ford will distribute just over $2.4 billion a year in dividends as well. The company has guided for $6 billion in free cash flow this year. I am not suggesting that a company’s entire capital expenditure budget should be covered by free cash flow, but it makes a lot of sense for an automaker facing recessionary risks in a rising high-interest-rate environment to pay down debt aggressively while preserving the liquidity to invest in the business. Since the auto business is highly cyclical, the increasing odds of a recession this year paints a gloomy outlook for even the most well-established automakers such as Ford. Not so long ago, General Motors filed for Chapter 11 in 2009, highlighting how the cyclicality of the auto business could push established automakers to the brink of bankruptcy.

I will enjoy the supplemental dividend – like many of you – but I do have a feeling that this special dividend may come to haunt investors in the coming quarters.

Reasons Why Ford Is Still A Good Bet

Ford has a long way to go to deliver on its expectations but the company is making the right moves, especially when it comes to electrifying its vehicle fleet. General Motors embraced EVs years ahead of Ford, but the latter has quickly gained market share by electrifying the F-150; one of the most-loved trucks in U.S. history. Ford’s aggressive push into EVs can be seen in the company’s performance in 2022 – a year that was characterized by macroeconomic challenges and supply-chain losses.

Exhibit 3: General Motors EV/BEV sales in 2022

| Model | Units sold |

| Cadillac (Lyriq) | 122 |

| Chevrolet (Bolt EV/EUV) | 38,120 |

| Hummer EV Pickup |

854 |

| Total | 39,096 |

Source: InsideEVs

Exhibit 4: Ford EV/BEV sales in 2022

| Model | Units sold |

| Mustang Mach-E | 39,458 |

| F-150 Lightning | 15,617 |

| Ford E-Transit | 6,500 |

| Total | 61,575 |

Source: InsideEVs

Ford’s strategy to focus on electrifying its popular vehicle models is already paying off, and I believe this strategy will help the company establish itself as Tesla Inc’s (TSLA) top competitor in the United States.

Ford has not completely given up on combustion engine vehicles as well, which is another characteristic that I find value accretive. The company is focused on striking a balance between EVs and its existing line of conventional vehicles, which I believe is the right strategy given it will take years to turn up profits from EVs alone.

Valuation is the other factor that stands out. Ford offers exposure to the EV sector at a forward P/E of below 9 in complete contrast to many pure-play EV companies that are yet to see any profits at all. While I am not against paying a premium to invest in market leaders, I believe the EV industry still has a long runway for growth and that today’s market leaders may not be leaders in the long run. Investing in an automaker that gives exposure to the best of both worlds seems like the right strategy for my portfolio.

Takeaway

In my previous articles on Ford, I have extensively discussed its new business model and the prospects for its EV division. In this article, my focus was on the somewhat confusing earnings announcement that carried a few surprises. Ford, even after missing Wall Street estimates for revenue big time, seems to be heading in the right direction with its new strategy. This year is likely to be an important one in the history of the company as investors are now expecting Ford to deliver on its promises to improve operational efficiency. I will keep a close eye on the company’s performance this year to determine whether Ford continues to deserve a place in our portfolios.

Be the first to comment