S&P 500, FOMC, Dollar, GBPUSD and USDJPY Talking Points:

- The Market Perspective: USDJPY Bearish Below 141.50; Gold Bearish Below 1,680

- All attention is on the FOMC rate decision later today, but the question of whether the central bank hikes 75 or 100 basis points likely has limited influence over follow through

- Rate forecasts from the SEP will be important, but I’m looking more closely at the growth forecasts and the backdrop of rate decisions and growth updates due in the days to follow

Recommended by John Kicklighter

How do you create a strategy to trade the FOMC?

The Time Has Come: The FOMC’s Decision on 75 or 100 Basis Points

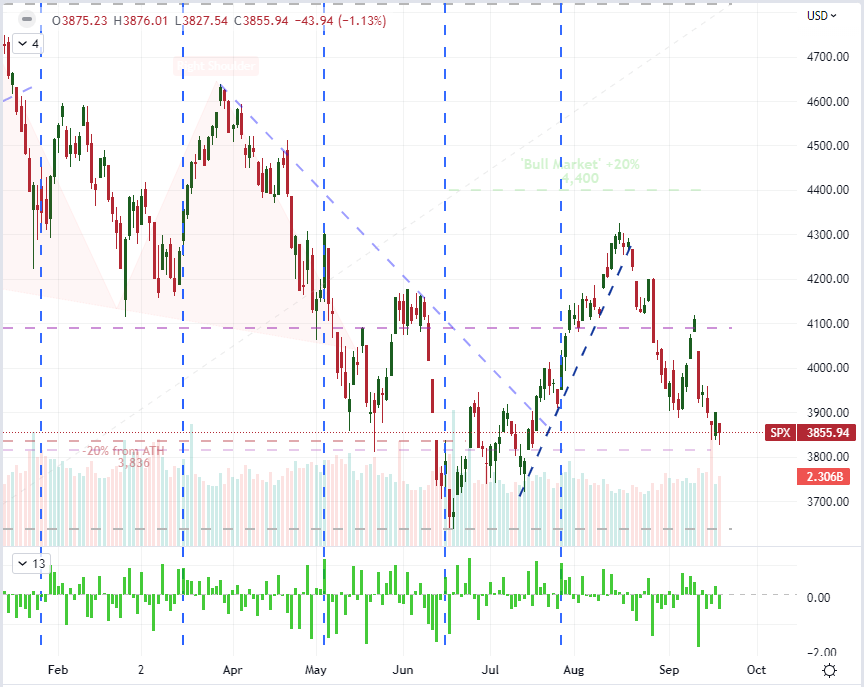

The event we have been waiting for is finally at hand. At 18:00 GMT, the Federal Open Market Committee (FOMC) will announce its policy decision following its scheduled two-day meeting. The markets have put some heavy speculation behind the outcome of this event with a health debate over whether the group fights inflation with an extraordinary third 75 basis point (bp) rate hike or to escalate their efforts with an incredible 100bp move. This event carries an inordinate weight beyond just the performance of local speculative assets like the S&P 500 and the relative strength of the US Dollar. There are global ramifications from what these group decides to do. Should it escalate the inflation fight with the larger move, it is likely to encourage peers around the world struggling with inflation to follow suit. Should they downgrade their growth outlook, it is likely that we see similar admissions from other groups not far behind. For most people the initial reaction to the announcement matters most. It’s worth noting that the S&P 500 has actually rallied on the day of the last four rate decisions with three of the instances spurring medium-term runs (counter trend thus far). What is in store for this event?

Chart of S&P 500 with Volume, 20 and 200-Day- SMAs with COT Net Spec Positioning (Daily)

{kind=link}

Chart Created on Tradingview Platform

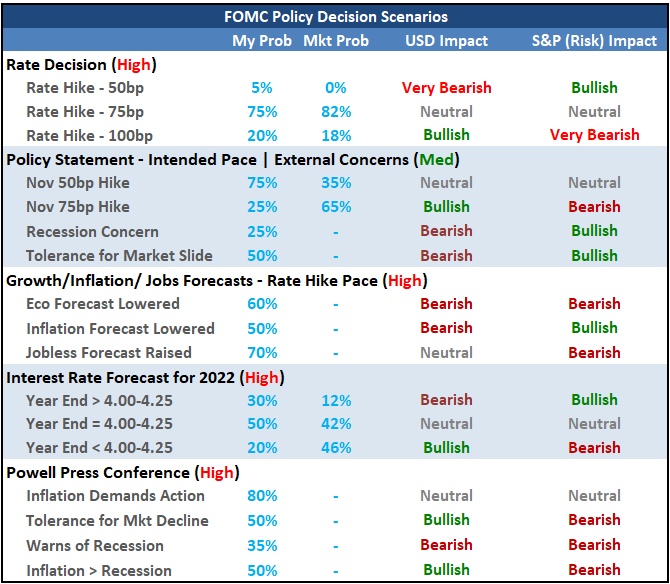

To help clear my mind of the many possible scenarios that can come from a multi-faceted event and transition my thinking from absolutes to probabilities, I like to work out a table of elements and market response. Below, is the result of my analysis. While most will be focused on the rate decision itself – and it is important – I believe the outcome will matter relatively little when it comes to the ultimate trend. If the Fed keeps to the 75bp pace, the immediate assessment from me would be that it ‘meets expectations’ and I will quickly shift to the simultaneous release of the Summary of Economic Projections (SEP). First look will go to the forecast of interest rates through year end and into 2023. However, I believe the views of the economic outlook will matter more here as relative interest rate paths as the financial restrictions bite expansion.

FOMC Scenario Table with Potential Market Impact

Table Created by John Kicklighter

USDJPY and Relative Monetary Policy

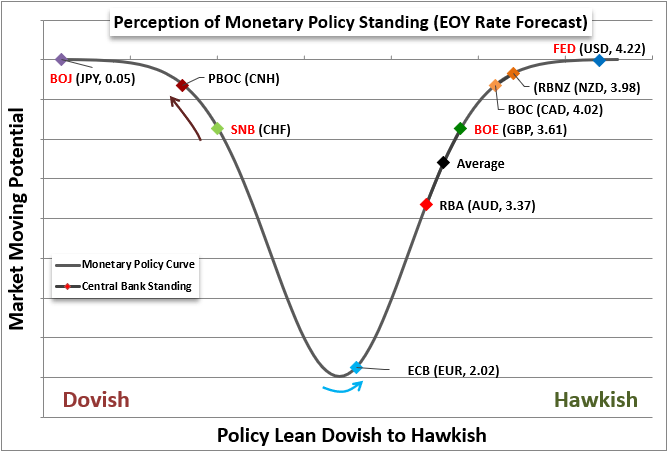

For those operating on a one-dimensional view of interest rates: the assumption is that higher rates is bad for growth (and thereby capital market assets) and a boon to the local currency for carry potential. The markets seem to me to be living with a remarkably obliviousness around the threat ahead between a natural slowing of economic expansion, the impact of monetary policy and the rich pricing behind so many benchmarks; but that spell can take time to dispel. For those monitoring relative yield, like FX trading, that distraction can align itself to a very basic yield differential view. Another 75bp hike from the Fed would bring the benchmark rate range from 2.25 – 2.50 percent to 3.00 – 3.25 percent. Fed Fund futures are pricing in a benchmark year end above 4.00 percent, but the last SEP is still behind that pacing. As remarkable as the pace is, there are not many central banks far from that clip (RBNZ, BOC, RBA) and those that are catching up (ECB). As such, there isn’t as much untapped potential here.

Chart of Relative Monetary Policy Standings Among Major Central Banks

Chart Created by John Kicklighter

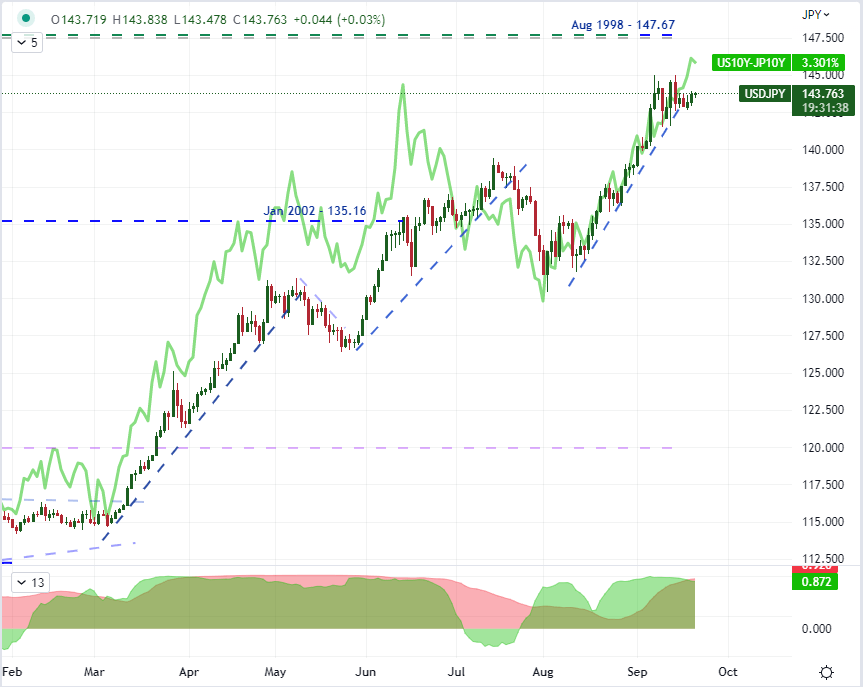

One pair where the current and outlook for the US interest rate will matter is USDJPY. This contrast between the Federal Reserve and Bank of Japan (BOJ) could not be any more extreme on the spectrum. The BOJ has been adamant with its effort to bolster economic growth via an extremely accommodative monetary policy stance. That is very different from most of its largest economic counterparts, and the result is a run from Yen crosses that is nothing short of extraordinary. Looking at USDJPY compared to the US-Japan 10-year yield differential, the correlation is remarkably strong. There aren’t many other Dollar cross where this same statement can be earnest voiced.

Chart of USDJPY Overlaid with US-Japan 10-Year Yield Differential and Correlations (Daily)

Chart Created on Tradingview Platform

GBPUSD and the Deeper Cut on Monetary Policy: Recession Risk

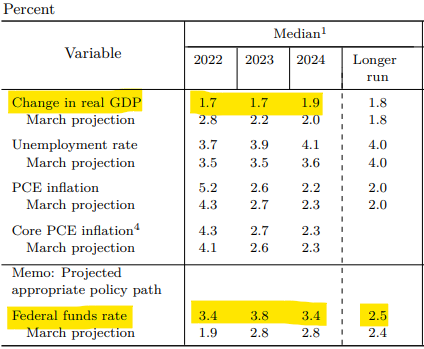

Rates and rate forecasts are an important consideration for the pricing of the financial markets, but my focus moving through the FOMC decision is on a consideration further into the fundamental schema. The inflation fight is to avoid a systemic economic crisis and it is willing to sacrifice short-term growth to achieve the effort. Ultimately, the risks is for near-term or long-term economic trouble. As such, I believe the market will eventually hone its focus on the probability of economic struggle or ultimately recession – which is poorly accounted for in current market pricing. Looking back at the last SEP, the outlook for GDP through 2022 was holding at 1.7 percent and there was little explicit warning of serious economic contraction. Perhaps we get this from the SEP this go around or Chairman Powell’s remarks at the press conference. Regardless, I will be watching.

FOMC Summary of Economic Projections from June 15, 2022 Meeting

Table from Federal Reserve’s SEP

Views of economic health matter…a lot. If we were to compare the S&P 500’s response to rate forecasts and economic projections, I would think that we follow closer to the lines from the latter factor. Where can we see this play out? A good example is GBPUSD. First and foremost, the current yield differential between the 10-year of Great Britain and the United States is far off the path of GBPUSD. What can explain this divergence? It isn’t the Pound is so ‘risky’ a currency that it is a safe haven play. Instead, it is the disparity in economic forecasts. The BOE has already warned recession is ahead. Should the Fed follow suit, it can offer serious fundamental balance here.

Chart of GBPUSD Overlaid with UK-US 10-Year Yield Differential (Daily)

Chart Created on Tradingview Platform

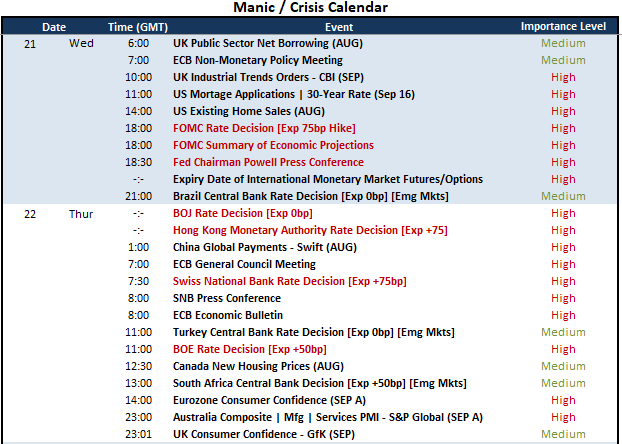

While all the attention is on the US event risks of the next 24 hours, how much impact they elicit will be seriously influenced by the currents from the rest of the world. We will consider growth elements on Friday with the release of September PMIs (and later considerations like the October IMF’s WEO), but for now, the focus is monetary policy. Following in the wake of the Fed on Wednesday afternoon, we have developed central bank decision including the Bank of Japan , Swiss National Bank and Bank of England. In addition we also, have key emerging central banks like the Brazilian, Turkish and South African authorities. Assess the context.

Critical Macro Event Risk on Global Economic Calendar for Next 48 Hours

Calendar Created by John Kicklighter

Trade Smarter – Sign up for the DailyFX Newsletter

Receive timely and compelling market commentary from the DailyFX team

Subscribe to Newsletter

Be the first to comment