PhonlamaiPhoto

A Quick Take On Flux Power

Flux Power (NASDAQ:FLUX) reported its FQ1 2023 financial results on November 10, 2022, beating revenue and EPS estimates.

The firm sells lithium-ion batteries for a variety of industrial mobility applications.

Given management’s focus on achieving breakeven, its recent revenue ramp due to supply chain improvements, and improving margin and operating loss trajectory, my outlook on Flux is a cautious Buy at around $4.80 per share.

Flux Power Overview

Vista, California-based Flux Power was founded in 1998 to design, develop, manufacture and market lithium-ion batteries for lift trucks, airport ground support equipment, and other industrial applications.

Management is headed by President, CEO and Director Ronald F. Dutt, who has been with the firm since 2012 and was previously COO and CFO at Famgro Farms.

Flux Power has developed the LiFT battery pack technology.

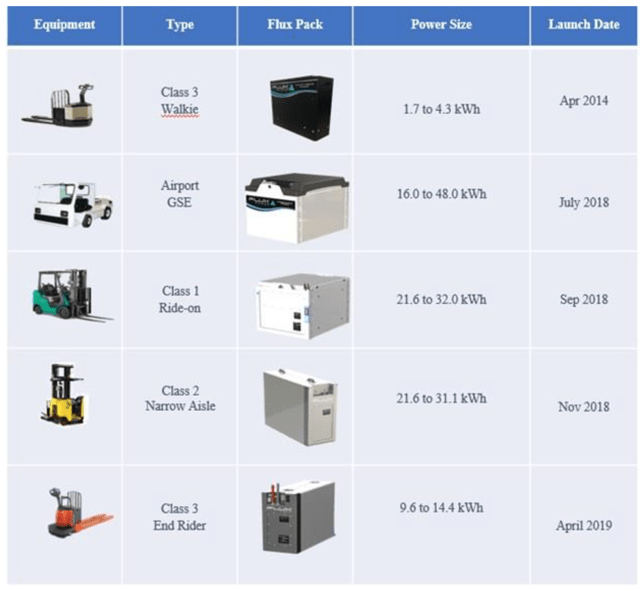

Below is an overview of certain of the company’s product lines:

Company Products (SEC)

Flux Power markets its products both directly to end-users, OEMs, and lift equipment dealers as well as through battery distributors.

The company’s direct sales staff is assigned to major geographies to collaborate with its sales partners on an established customer base.

Additionally, the firm has a call center as well as a nationwide network of service providers, most commonly forklift equipment dealers and battery distributors, tasked with providing local support to large customers.

Flux Power’s Market & Competition

According to a 2019 market research report by Adroit Market Research, the global lithium-ion battery market is projected to reach $105 billion by 2025.

The main factors driving market growth are increasing carbon emissions as well as a shift in the automobile industry from conventional fuel vehicles to electric vehicles.

Per the report, approximately 14% of global car sales by 2025 will be electric, consequently raising the demand for lithium-ion batteries.

Automobile and electronics manufacturers are moving their manufacturing operations in China to reduce labor and logistics costs as well as gain access to uninterrupted raw material supply due to the country’s status as a global leader in the lithium-ion battery value chain.

The Asia-Pacific region is projected to grow at the fastest CAGR of over 15% owing to China’s lithium-ion battery industry.

Major competitors that produce lithium-ion batteries include:

-

LG Chem

-

Tesla

-

BYD Company

-

GS Yuasa

Flux Power’s Recent Financial Performance

-

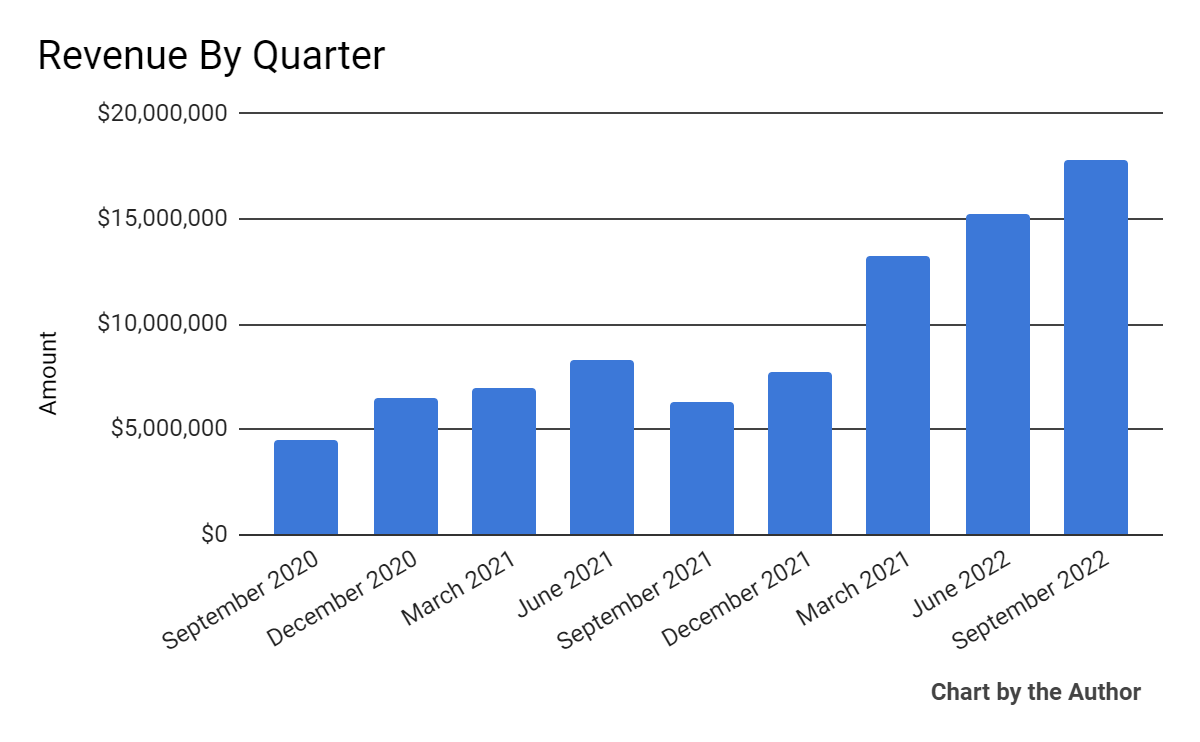

Total revenue by quarter has risen sharply recently:

9 Quarter Total Revenue (Seeking Alpha)

-

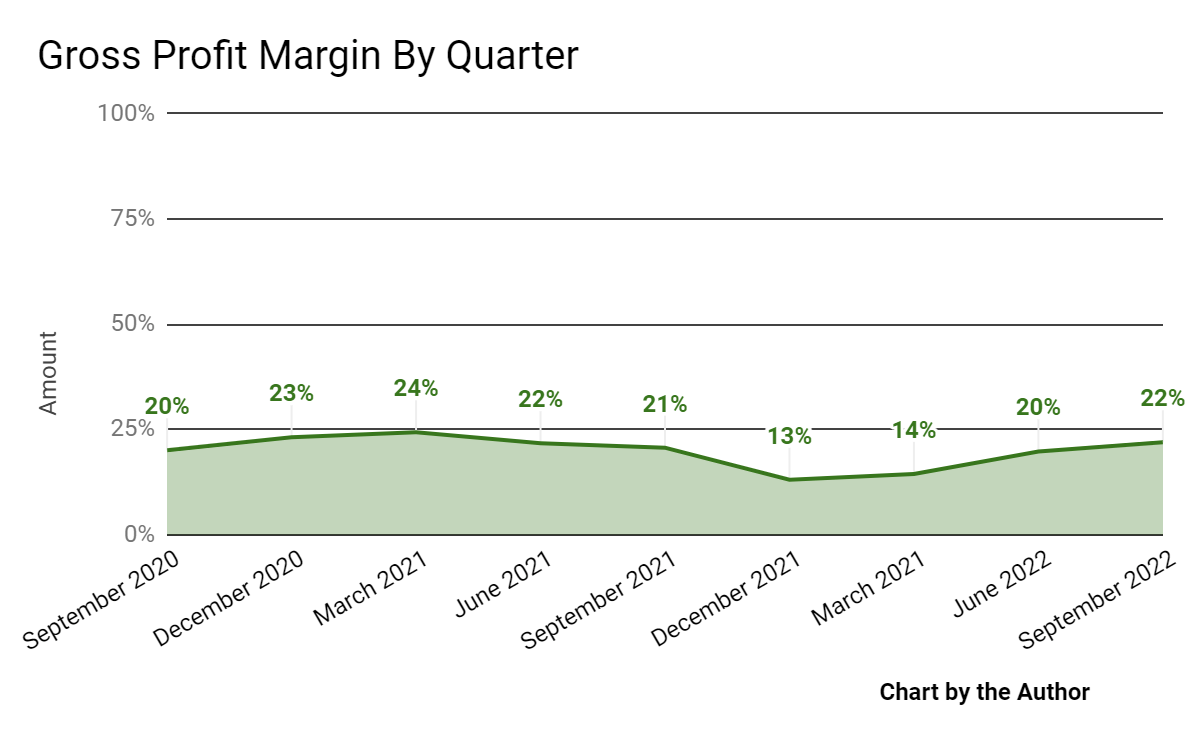

Gross profit margin by quarter has varied markedly in recent quarters:

9 Quarter Gross Profit Margin (Seeking Alpha)

-

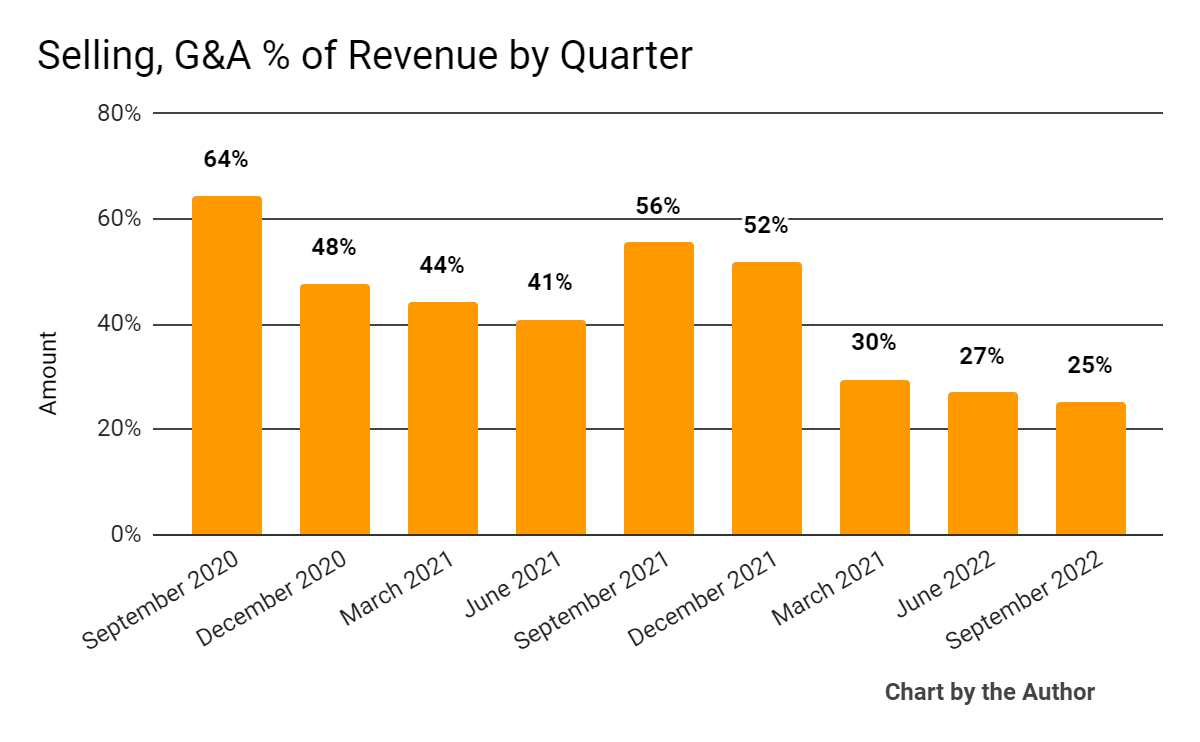

Selling, G&A expenses as a percentage of total revenue by quarter have dropped materially in recent reporting periods:

9 Quarter Selling, G&A % Of Revenue (Seeking Alpha)

-

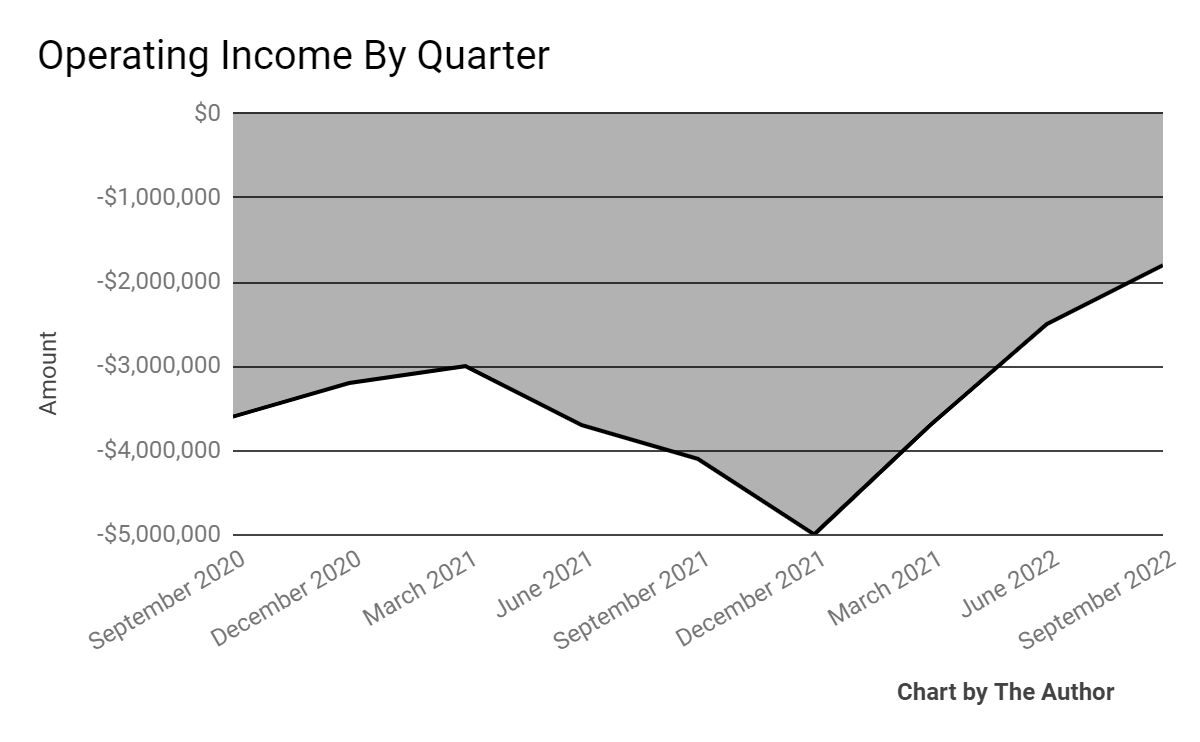

Operating losses by quarter have been reduced more recently:

9 Quarter Operating Income (Seeking Alpha)

-

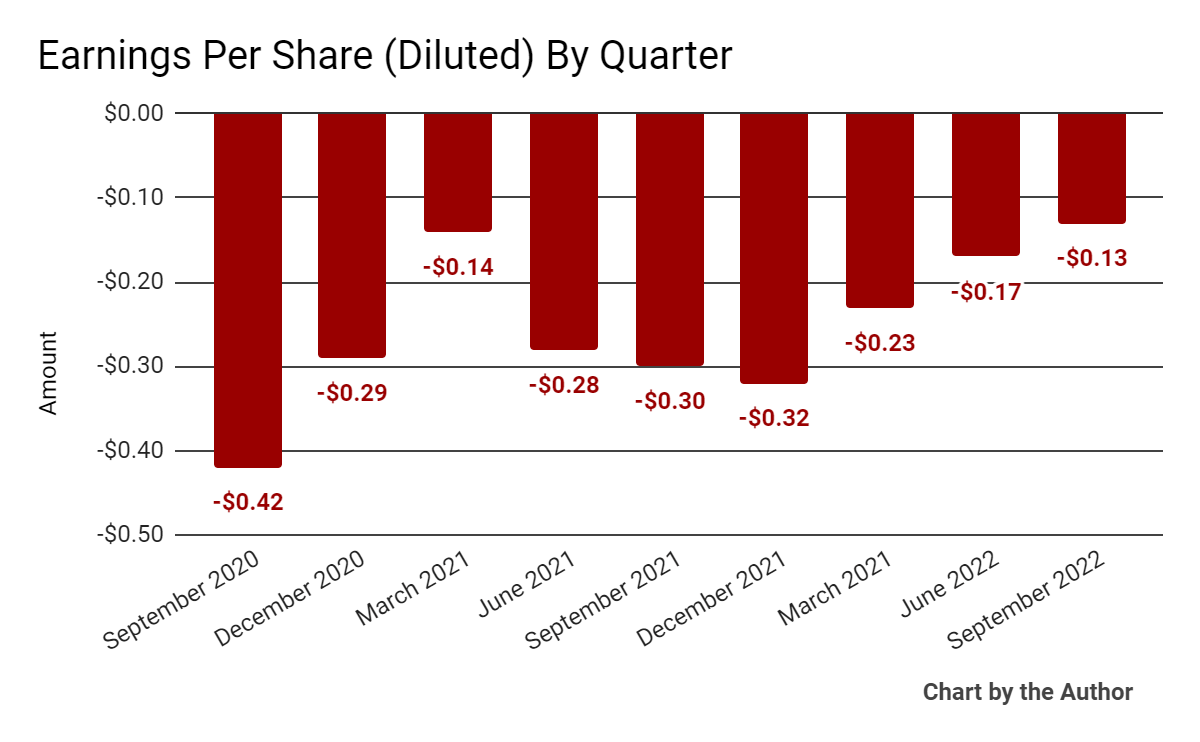

Earnings per share (Diluted) have made some progress toward breakeven:

9 Quarter Earnings Per Share (Seeking Alpha)

(All data in the above charts is GAAP)

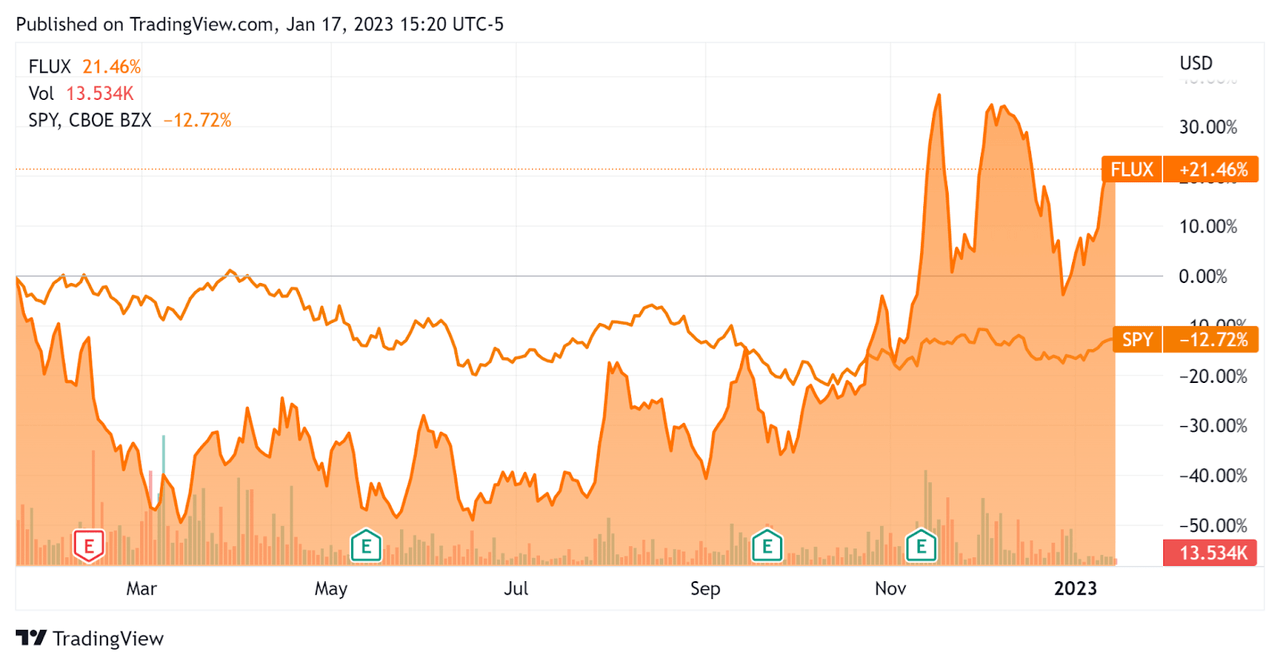

In the past 12 months, FLUX’ stock price has risen 21.5% vs. the U.S. S&P 500 index’s drop of around 12.7%, as the chart below indicates:

52-Week Stock Price Comparison (Seeking Alpha)

Valuation And Other Metrics For Flux Power

Below is a table of relevant capitalization and valuation figures for the company:

|

Measure [TTM] |

Amount |

|

Enterprise Value / Sales |

1.6 |

|

Enterprise Value / EBITDA |

NM |

|

Revenue Growth Rate |

92.3% |

|

Net Income Margin |

-25.3% |

|

GAAP EBITDA % |

-23.0% |

|

Market Capitalization |

$77,740,192 |

|

Enterprise Value |

$85,898,192 |

|

Operating Cash Flow |

-$20,066,000 |

|

Earnings Per Share (Fully Diluted) |

-$0.85 |

(Source – Seeking Alpha)

Commentary On Flux Power

In its last earnings call (Source – Seeking Alpha), covering FQ1 2022’s results, management highlighted the reduction in customer order backlog due to improving sourcing efforts that have mitigated shortages of components.

The firm has also launched new product designs based on customer feedback and the need to improve performance, reduce the total cost of ownership and provide new features.

Management has continued to focus on improving profitability through improved production processes and other cost-reduction efforts.

Also, the company is seeking to broaden its coverage into related industries such as robotics.

As to its financial results, revenue rose 184% year-over-year and 17% sequentially.

Gross profit margin improved year-over-year and sequentially, while SG&A as a percentage of revenue dropped.

As a result, operating losses were reduced, as were negative earnings.

For the balance sheet, the firm ended the quarter with $300,000 in cash and equivalents and $5.7 in short-term borrowings.

Over the trailing twelve months, free cash used was $21.0 million, of which capital expenditures accounted for $900,000. The company paid $600,000 in stock-based compensation.

Looking ahead, management did not provide any forward guidance but appears to be managing to reach operating breakeven and said they would not seek additional equity investment until doing so.

Regarding valuation, the market is valuing FLUX at an EV/Revenue multiple of 1.6x on very strong revenue growth.

However, the primary risks to the company’s outlook are the ‘lumpiness’ of its order flow and ability to deliver given supply chain limitations as well as a slowing macroeconomic environment in 2023.

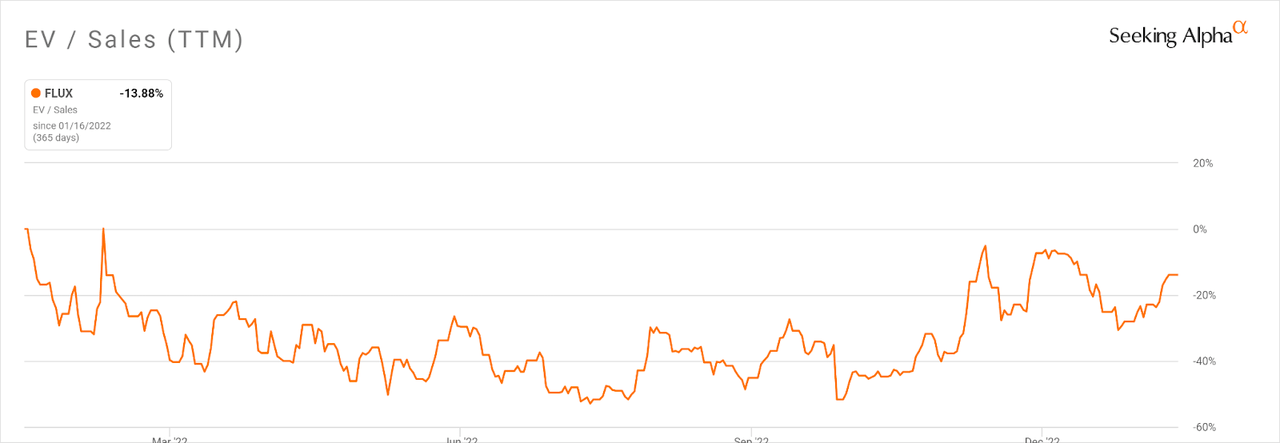

Notably, FLUX’ EV/Sales multiple [TTM] has fallen by only 13.9% in the past twelve months, far less than many technology companies, as the Seeking Alpha chart shows here:

Enterprise Value / Sales Multiple (Seeking Alpha)

A potential upside catalyst to the stock could include a ‘short and shallow’ downturn in 2023 and continued growth in orders and decreasing supply chain constraints.

Given management’s focus on achieving breakeven, its recent revenue ramp due to supply chain improvements, and improving margin and operating loss trajectory, my outlook on Flux is a cautious Buy at around $4.80 per share.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment