gorodenkoff

Published on the Value Lab 12/26/22

Flow Traders (OTCPK:FLTDF) is a liquidity provider and a registered dealer that buys and sells exchange traded products and other financial products too. Exchange traded products are baskets of products from various asset classes that serve similar purposes as mutual funds and ETFs but is its own market. As a principal trader and dealer, FT’s aim across products is to earn on spreads between bid and ask prices, and therefore when liquidity provision becomes more valuable, in other words when there’s volatility, they can make more money. It’s a good countercyclical bet, and it’s a play on crypto volatility as FTX collapses, which could create circumstances for earnings higher spreads if FT quotes well. The downside is in the Flow Traders Capital division which has a lot of digital asset investments. The values of these have surely fallen as crypto takes a hit following the FTX blow-up. Nonetheless, the income at risk is rather limited on this side, and things should go pretty well for FT if they can be on the right side of trades when spreads are getting large in crypto.

Q3 Breakdown

The areas of substantial activity have been crypto and fixed income, markets where liquidity provision is already more appreciated by markets with larger spreads. Value of trade in these areas is seeing the most substantial growth, and volatility in the secondary fixed income markets thanks to the rate cycle have been a boon to the FT business. On the other side, general volatility in crypto and greater presence of FT in these markets continues to grow their income.

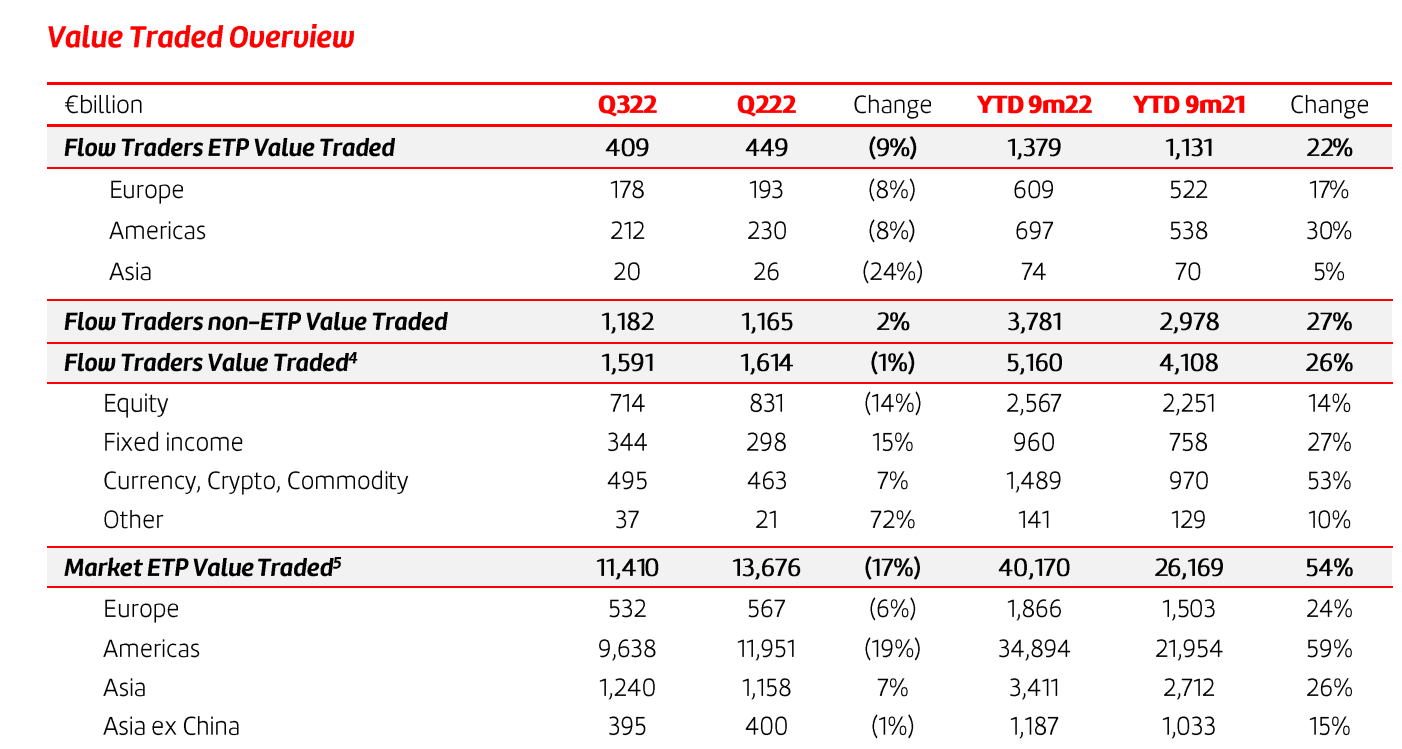

Values Traded (Q3 2022 PR)

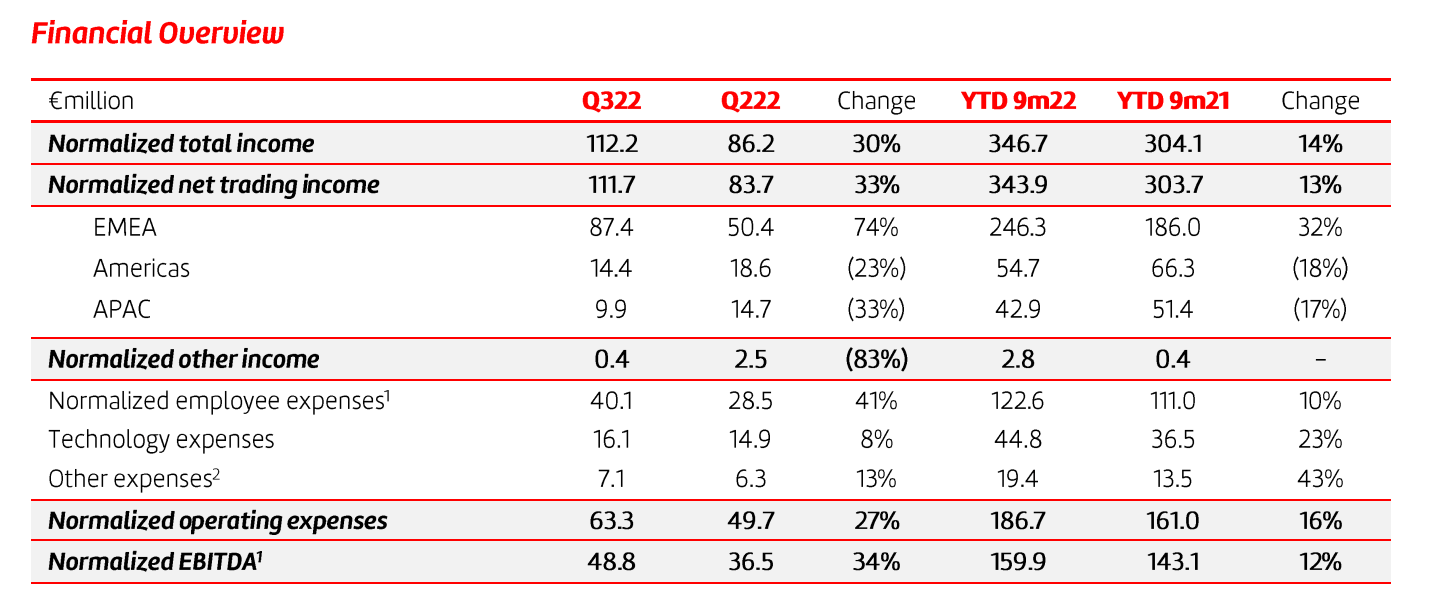

Earnings (Q3 2022 PR)

Crypto is basically 30% of the value that FT trade, so with the collapse of FTX and the introduction of another wave of volatility in the markets, caused specifically by negative liquidity effects from a fallen exchange, liquidity provision should be earnings nice spreads into the Q4.

In other markets like fixed income, difficulties in the secondary markets, both OTC and on the exchanges, are creating opportunities for earning spreads as speculation over the dynamics of the rate cycle evolves.

Generally, the VIX is up YoY, but the approach to the year-end has seen relaxing in volatility. VIX growth has persisted into November.

FT is growing its exposure in the US, noted by the higher trading values as it offers liquidity provisions for a range of equity and fixed income ETFs and it is growing its ISIN coverage. Still, Americas remains a pretty limited market. In the Asian markets FT is moving towards establishing its presence as an on-shore dealer in China and continuing to develop its presence in the HK market as well. They have just gained a key license to do that with. Volumes are up, but the trading environment in the US and China remains difficult, and it’s tough to be on the right side of trades as liquidity is provided in these bear markets, and growth in volumes is coming from products with less spreads to offer.

Bottom Line

Crypto volatility could be an incremental opportunity for FT, but what is for sure to take a hit is the DeFi investments that FT have been accumulating in their Flow Traders Capital business, which contain longer-term assets whose values have surely plummeted. We estimate there’s about a $15 million EUR income at risk, which should be around a 5% hit to FT’s overall EBITDA. Besides that, there should still be some energy to Q4 results on a YoY basis.

There’s something to say about Flow Trader’s value. It’s a market maker for a lot of interesting products. Volatility in crypto is a short-term opportunity, although the longer-term prospects of the asset class remain a lot more unclear, especially as scrutiny over crypto grows. This explicit exposure to the asset class’s growth is what likely contributes to the FT discount. It trades at 10x with a yield of 6%, reflecting a valuation at about half of a typical broker or trader. While a 30% exposure to crypto is substantial, the other assets are seeing growth as well. Fixed income should be an interesting class for as long as the current rate cycle lasts, and it’s not a guarantee that crypto’s days are numbered. Other exchanges stand strong like Binance (BNB-USD). It’s also succeeding in business development in new markets like China, which should still offer an interesting trading environment on a secular basis. A valuation at half of other businesses with similar economics, despite FT’s crypto exposure, seems excessive.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment