William_Potter

Investment Thesis

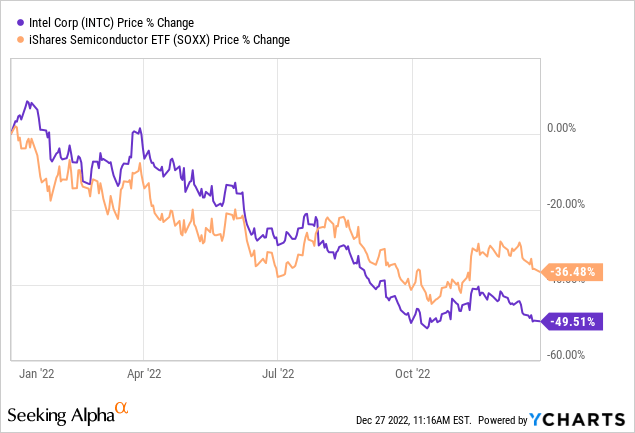

Intel Corporation (NASDAQ:INTC) has lost nearly 50% of its value in 2022, substantially underperforming the market and iShares Semiconductor’s ETF (SOXX). While the market is disappointed with Intel, the promises of Pat Gelsinger have not yet convinced investors that a turnaround is happening anytime soon. Instead, the market believes that Intel has lost its way and has no way back.

However, several geopolitical moving parts and the ongoing US-China Chip wars will continue to damage both parties in the short run. In addition, Intel’s revenues might be hurt in the short run due to the US export controls imposed on China. Still, as we approach the end of the semiconductor cycle and the end of the shortage by the end of 2023, Intel is well-positioned to defend its market share and meet its targets.

China Export Control Casts A Cloud Over Intel

The US-China trade war has intensified over the past couple of months, with the United States implementing export controls over certain items to China, including semiconductors. The export restrictions by the USA are part of the US’s long-term strategic shift towards decreasing its reliance on outside suppliers and winning in the tech war. By denying China access to advanced US-origin chip design software, silicon, and semiconductor manufacturing equipment, the US aims to stifle the Chinese government’s technological advancement.

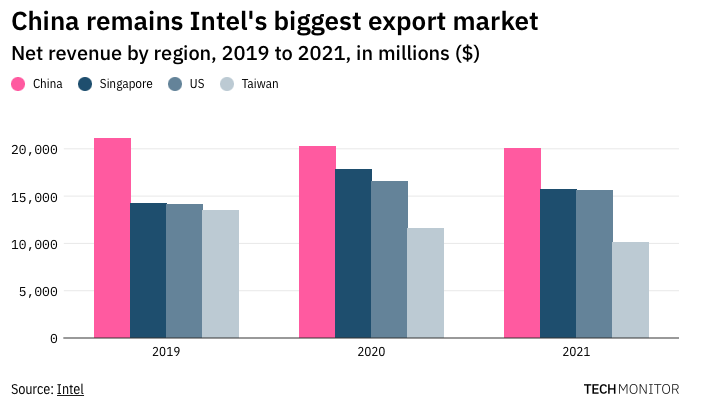

As per the set restrictions, companies cannot export semiconductors to China that are more sophisticated than 16nm or 14nm processors with 3D structures, 18nm DRAM chips, or NAND flash chips with above 128 layers. It is no secret that China is the single biggest market for Intel. Although the company has been trying to diversify its revenue stream, that will likely take many years. China is expected to remain an important region for the company in terms of its established customer base.

techmonitor.ai

INTC does not break down its product sales by geographic region, so at this point, it is difficult to estimate the impact of China’s export control over the company’s top line and profit margins. However, according to the company’s last annual report, China was the company’s largest export market by a wide margin. For example, between 2019 and 2021, Intel sold over $60 billion worth of processors, PCs, and data center equipment to China, with Singapore coming in second with $48 billion. During the same time, sales to American organizations totaled $46.2 billion.

While the shift towards establishing American leadership in advanced tech is set to benefit INTC, as the company stands to get $20 billion under the CHIPS act and $5/$10 billion under the FABS act, the US’s move to isolate China from access to advanced chips is a significant challenge for the company to navigate through, given the importance of the region in terms of revenue contribution.

Q3 Results & 2023 Outlook

Looking ahead into 2023, INTC expects PC unit TAM to be flat to down 8% from the 2022 mark of 295 million units on consumer PC weakness, while data center TAM is in a better position given continued US hyper-scale plans for cloud infrastructure expansion tempered somewhat by China weakness.

Given the weak environment heading into 2023, the team is taking prudent action on areas it can control by identifying structural cost reductions that should drive $3 billion in savings to COGS/OpEx in 2023 and $8-$10 billion in savings by the end of 2025.

Cost-Cutting Aiding Preservation Of Its Book Value

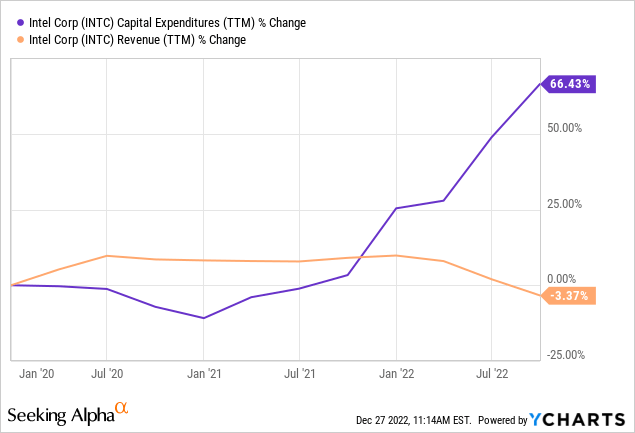

The company continues to cut down on net CapEx and has reduced Q4 CapEx outlay by $2 billion amidst a weak demand environment. In addition, management has laid out a plan to reduce costs significantly, a marked departure from the beginning of CEO Pat Gelsinger’s tenure and a welcome initiative to investors.

If they can even partially execute on their lofty goal to reduce CapEx by $2 billion this year, provide $3 billion in cost savings in 2023 and $8-$10 billion annually by the end of 2025, the improvement to FCF and the subsequent preservation of BV should put a floor on valuation. As a result, we should expect a gradual margin improvement as 2023 unfolds. Although the company hasn’t given a figure for CapEx going forward in 2023, the company targets to keep the net CapEx to around 35% of revenue.

PC Share Is Stabilizing

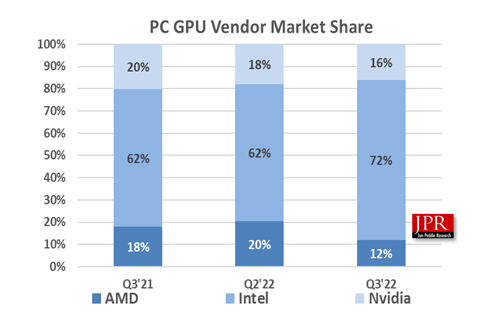

One of the key bear theses for INTC has been the PC market share loss to Advanced Micro Devices, Inc. (AMD). The share fell from 75% in Q3 2021 to 72% in the previous quarter. However, in Q3 2022, Intel increased its GPU market share by 10.3% compared to the loss in market shares by both NVIDIA Corporation (NVDA) and AMD. The stabilization in the CPU share indicates that we might be near the bottom of the PC share range for Intel, and there is a limited downside from current levels.

www.notebookcheck.net

Product-line Re-positioning Continues

The launch of Granite Rapids and Sierra Forest (both of which CEO Pat Gelsinger had a much larger role in developing/optimizing than preceding products) will then pose a more formidable lineup to enable the company to regain share. INTC stressed it has not become particularly aggressive on price in recent quarters, but acknowledged more aggressive efforts to optimize its product placement at customers.

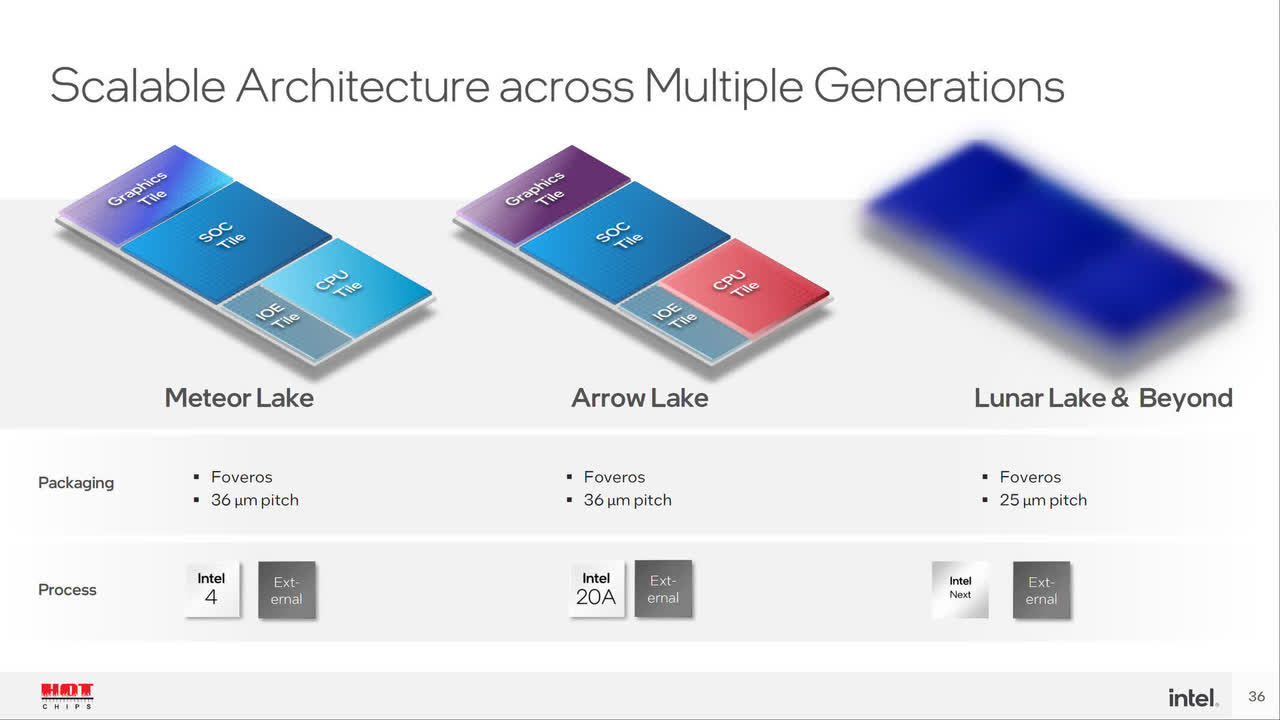

Meteor Lake Delays

The bad news for Chipzilla comes from an information leaker, “Raichu,” who claims that Meteor Lake for desktop is “maybe” canceled because Intel views it as uncompetitive. Intel originally planned six performance cores and 16 efficiency cores. Meteor Lake would be a step backward since the Raptor Lake flagship has eight performance cores and 16 efficiency cores. Thus, it’s possible that Intel does not believe it to be competitive against AMD’s upcoming offerings, and it’s also possible that the new delay is real.

www.techpowerup.com

The Internal Foundry Model

Intel is now embracing an “Internal Foundry Model” that establishes consistent processes, systems, and guardrails between manufacturing teams and business units. As a result, business units will be the same as external foundry customers with the hope to make the manufacturing group and business units more agile, better decision makers, more efficient, and that it discover new cost savings.

Intel has identified nine sub-categories for operational improvement already and expects this will allow the company to benchmark itself against other foundries to drive better performance. Additionally, better transparency for shareholders is expected as there will be a complete “Internal Foundry” income statement starting in 2024.

Separating design from a more foundry-like manufacturing business will drive $8-$10 billion in long-term cost savings. INTC’s philosophical and operational shift from a homogenous, near-monopolistic manufacturing organization to a more heterogeneous, flexible, and competitive operating structure should help to drive significant efficiencies to enable the company’s long term cost savings target (albeit with this target still somewhat dependent on revenue growth).

For example, INTC estimates some of its existing tools to operate at only 20-25% of the efficiency of equivalent tools of its leading foundry competitor. However, this statistic exemplifies the potential efficiency gains that can be unlocked down the road. INTC aims to achieve these efficiencies via its IDM 2.0 Acceleration Office, and the ultimate goal is to restore the margins of a leading-edge foundry and a fabless semi, yielding a ~60% GPM and ~40% OPM.

Concluding Thoughts

Intel is gradually reducing its reliance on the PC-centric market by entering data-centric industries like AI and autonomous driving. Future development prospects for Intel are indicated favorably by its leadership in the PC industry, strength in servers, expanding influence in the software, IoT, and ADAS domains, and progress in process technology.

The semiconductor sector is going through a downward cycle due to inventory adjustments. INTC now offers a fantastic entry point to new investors and a great DCA point for existing shareholders to average down their investments. As we have discussed in earlier articles, turnarounds take time, and inpatient investors with short-term investment horizons should consider avoiding the stock. Nevertheless, INTC is a strong buy near its Book Value of $24 per share, with a rewarding dividend yield of 5.6% and massive upside potential in the next three to five years.

Be the first to comment