toondelamour

Introduction

Shares of Floor & Decor (NYSE:FND) have risen 30% YTD. Since my publication on October 20, 2022, the stock is up 45%, outperforming the S&P index, which is up 12%. Based on the current stock price, updated macro data, company reporting and my own expectations, I decided to amend my model and change my recommendation. So, in my personal opinion, declining home sales and high inflation could have a negative impact on future cash flows over the coming quarters.

The survey of current trends

First of all, I would like to draw attention to the decline in existing home sales. Thus, rising inflation, declining consumer confidence, declining real incomes, high interest rates and increased interest costs continue to have a negative impact on home sales in the US. In my personal opinion, at the moment the market does not fully take into account the potential for a decrease in the company’s revenue in the coming quarters due to a decrease in demand for the company’s products. You can see the details in the chart below.

Existing home sales (bea.gov)

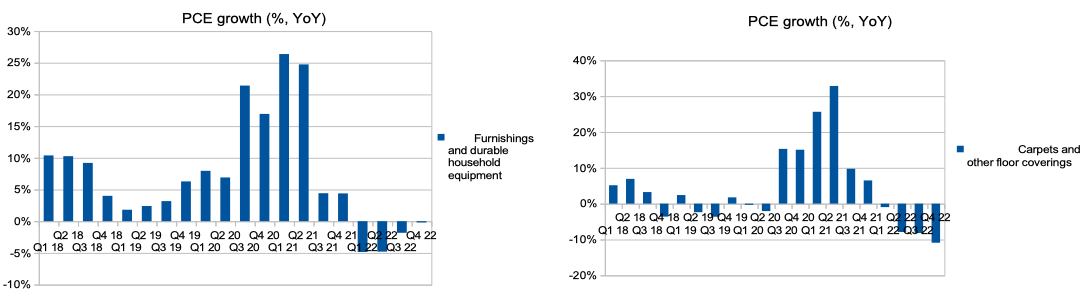

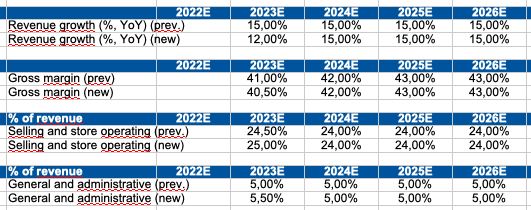

Thus, in view of declining home sales and declining real incomes, we may see a decline in furnishings and durable household equipment spending throughout 2022. In addition, one of the furnishing spending segments is the “carpets and other floor coverings” segment, where the rate of decline in consumer spending even outpaces the rate of decline in furnishing costs. Thus, in Q4 2022, expenses on carpets and floor covering decreased by 11% YoY, while total expenses on furnishings decreased by less than 1% YoY. You can see the details in the charts below.

PCE expenditures by category (bea.gov)

Projections

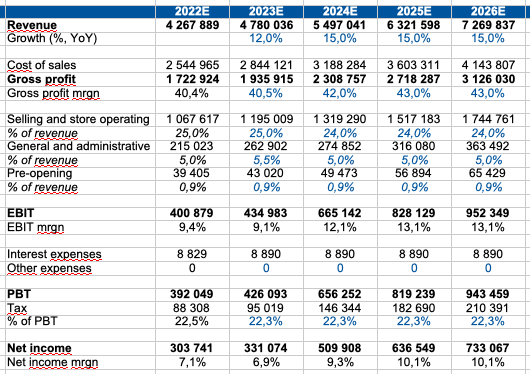

Thus, based on the company’s results for the 3rd quarter of 2022, current macro trends and my own expectations, I decided to make a change to my model. I believe we will see revenue growth slow down to 12% in 2023. In addition, I slightly lowered my own expectations regarding the gross margin. So, I lowered my forecast from 41% to 40.5% in 2023. In addition, I slightly increased operating expenses (% of revenue) due to the expected increase in inflation, rising costs and decreasing economies of scale. You can see the details of changing the main input data in my model in the table below.

Forecasts (Personal calculations)

So at the moment my model is based on the following data:

Revenue growth: I believe that the company’s revenue growth will be about 12% by the end of 2023, then I predict a stable level of about 15% until 2026.

Gross margin: I expect the gross margin to recover to 43% by 2026 after a weak 2023 due to lower demand and rising supply chain costs.

Selling and store expenses: I predict spending to rise to 25% (% of revenue) in 2023, then I predict a slight decrease to 24% through 2026 due to normalization of consumer patterns.

General and administrative expenses: I expect expenses to rise to 5.5% (% of revenue) in 2023, then I expect a decrease to 5% due to accelerated revenue growth and increasing economies of scale.

You can see the details of my predictions in the chart below.

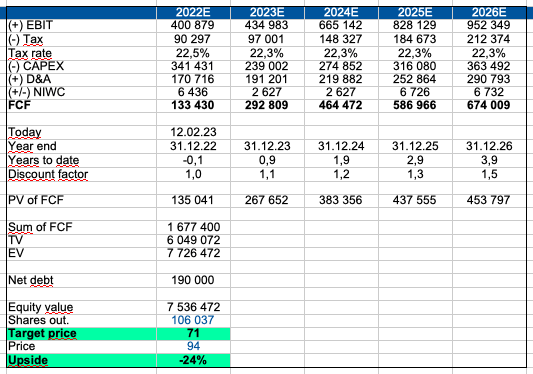

Yearly projections:

Forecasts (Personal calculations)

Valuation

For company valuation, I prefer to use the DCF approach, because building a DCF model allows me to take into account the impact of macro factors on the future cash flows of the business. In addition, the construction of DCF allows you to take into account changes in the growth rate of revenue and the level of operating profitability of the business. Moreover, the company operates in a stable and predictable market where the use of DCF is most preferred.

The main inputs in my model are:

WACC: 10.7%

Terminal growth rate: 3%

DCF model (Personal calculations)

Multiples

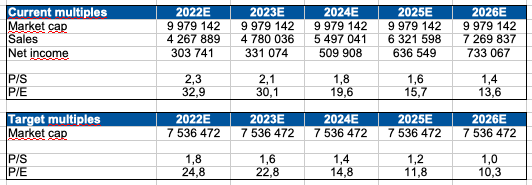

Based on my own sales and net income forecasts, I calculated current and target P/S and P/E multiples for the company. On the chart below you can see the results of my calculations.

Multiples (Personal calculations)

Risks

Macro: weak housing market, declining real incomes, declining consumer confidence and rising inflation could lead to lower consumer spending in the segment, which could have a negative impact on business revenue dynamics. Traffic & ticket: a decrease in traffic in the company’s stores and a decrease in the average check due to weak housing sales and a decrease in real income may lead to a decrease in the growth rate of the business’s revenue.

Margin: an increase in operating costs (labour, supply chain), a decrease in economies of scale can lead to a decrease in profitability.

Drivers

Macro: rising real incomes, rising consumer confidence, declining inflation and a recovery in home sales could lead to higher demand for the company’s products, which could have a positive impact on the business’s revenue going forward.

Margin: increase in product prices, increase in average check and increase in traffic in stores, effective control of operating costs, growth in market share and increase in economies of scale can have a positive impact on the company’s operating profitability.

Conclusion

So, in my personal opinion, the fair share price is $71 with a downside potential of 24%. I believe that now is not the best time to go long. Firstly, in my personal opinion, the market does not sufficiently assess the risks of a decrease in the company’s revenue due to weak macro indicators. I think we will see revenue pressure in 2023 from lower home sales and real incomes, and reduced economies of scale could lead to lower operating margins. I look forward to revisiting my view of the company in the future as I see signs of normalization at the macro level. Let me remind you that on February 23, 2022, the company plans to announce results for the 4th quarter of 2022.

Be the first to comment