Flexsteel Industries (FLXS) is a furniture manufacturer, largely focused on higher-end residential products including sofas, recliners, and beds. The name “Flexsteel” is derived from their trademark blue steel springs that come inside each piece of furniture and carry a lifetime warranty – a strong value proposition.

Flexsteel has been in business since 1893, and has typically focused on this upper-middle market segment. They largely sell to retailers, but maintain direct-to-consumer channels as well as a burgeoning e-commerce presence – though I was unable to find much aside from a Wayfair page with two products. Perhaps they could use some SEO.

Collapsing Stock Price

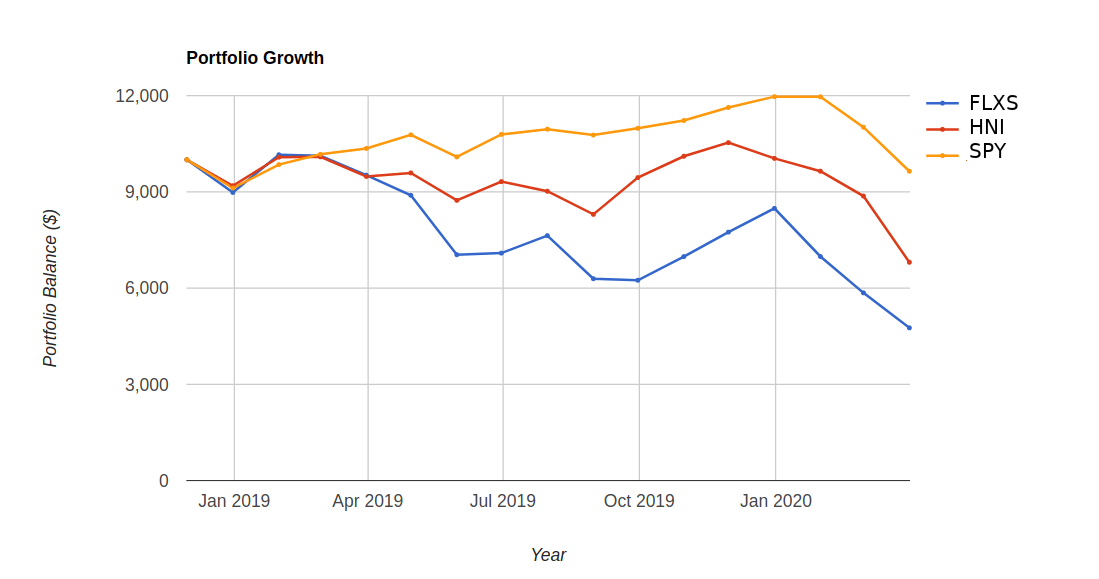

The stock is down more than 50% over the past twelve months, due to a few key reasons – mostly coronavirus, but also some more typical problems like secular industry declines, restructuring charges, and GAAP operating losses.

Management has chosen to raise cash by drawing on credit lines and pushing out accounts payable – moves that I believe are sensible, given the state of capital markets and the massive uncertainty we face going forward. Cash reserves are vital here, and Flexsteel holds nearly $60mm worth, likely enough to meet expenses for at least a year of virtually no revenues. Flexsteel has a current ratio around 3x, and holds cash just under current liabilities.

Management Track Record

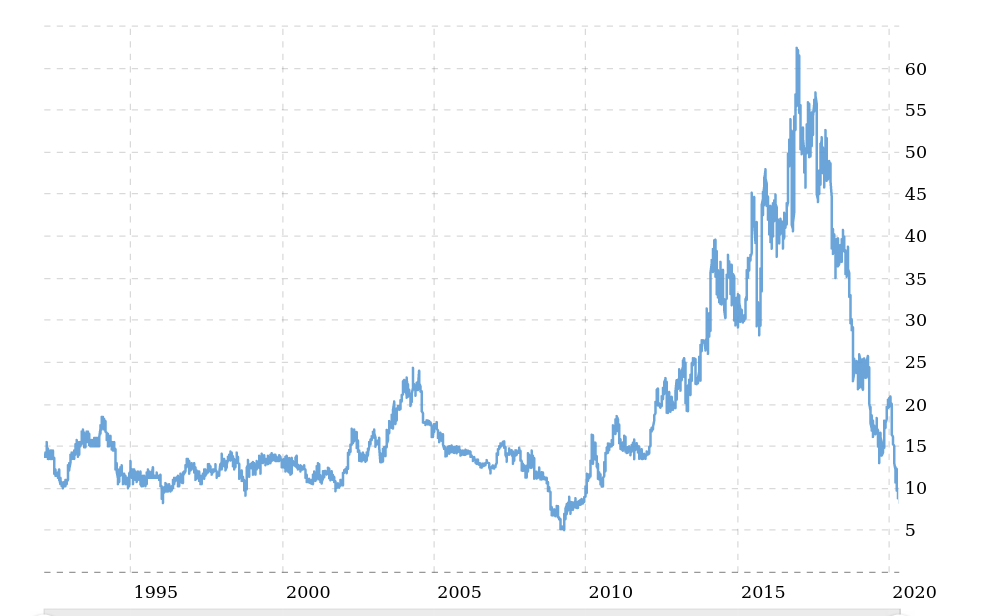

Flexsteel’s CEO is Jerry Dittmer, a furniture executive who holds an MBA from the University of Michigan. He has a successful 25+ year record in furniture, largely in Hon Co. and HNI Corporation (HNI). HNI Corporation is publicly traded, which makes Mr. Dittmer’s record easy to assess: he came on as VP/CFO in 2004, and became Executive Vice President in 2008, a role that he held until 2017, where he pivoted to SVP of Strategic Development.

HNI was greatly impacted by the housing bubble. Mr. Dittmer came on with the stock price at all-time highs in the $40s, which then fell to a bottom in the high-$9 range in 2008. I believe it is most appropriate to judge his record from this point on, when he was promoted to EVP.

Mr. Dittmer’s track record at HNI was not particularly remarkable – it roughly matched the S&P and Russell 2000 indices, albeit with more volatility. For a furniture retailer, I view this as an accomplishment.

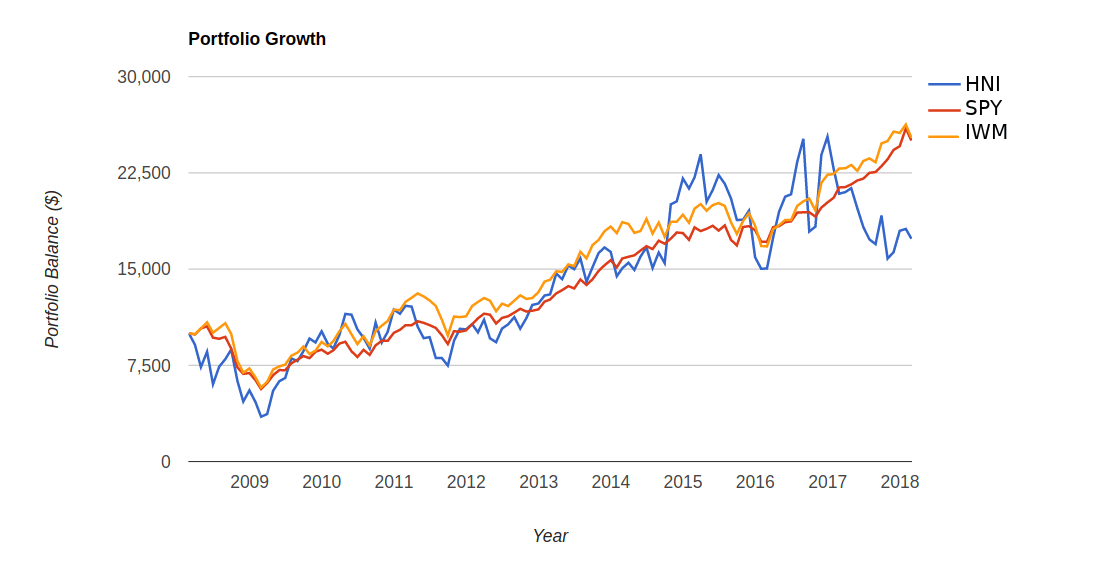

Since he took the helm of Flexsteel, the stock price has been plummeting – a fate shared by HNI, but to a lesser extent. It is not a wonderful picture, but given his pro-shareholder attitude I believe Mr. Dittmer is a good man for the job and faces a difficult turnaround.

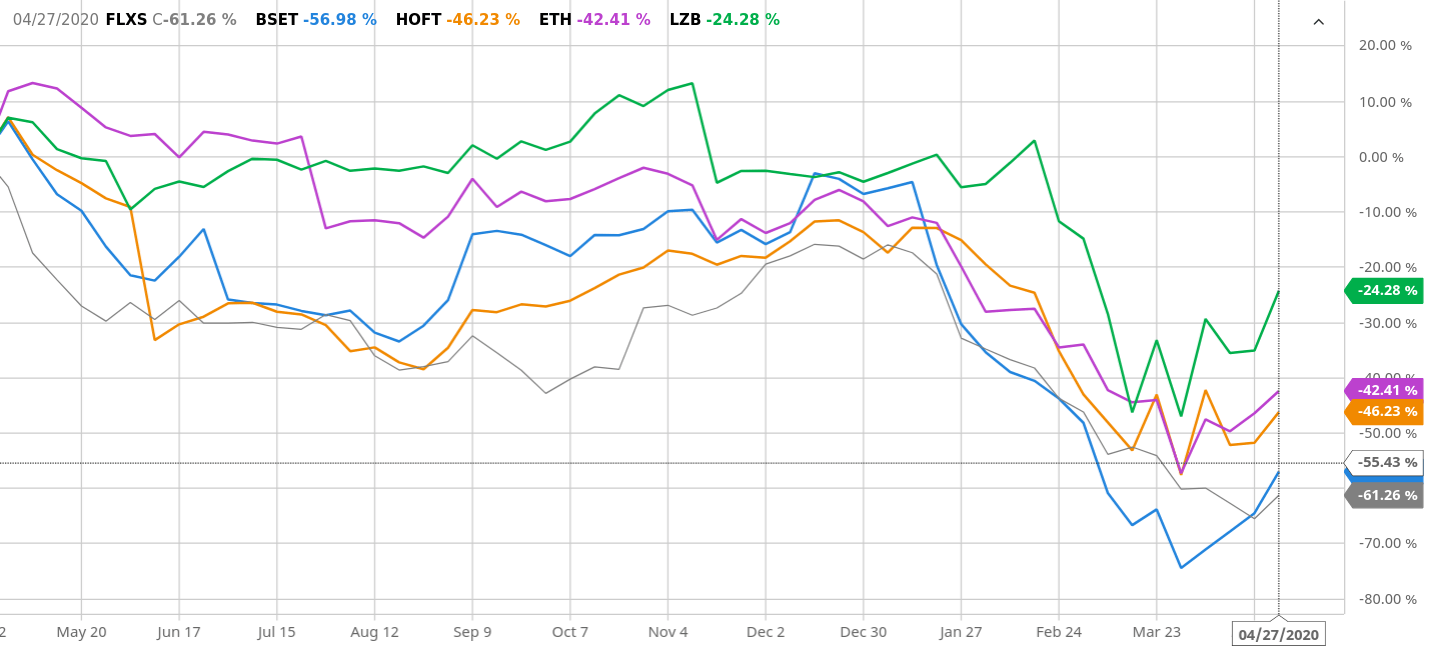

Flexsteel’s primary competitors are Bassett Furniture Industries, Inc. (BSET), Hooker Furniture Corporation (HOFT), Ethan Allen Interiors Inc. (ETH) and La-Z-Boy Inc. (LZB). All furniture has been struggling – between intense competition from Amazon, manufacturing issues, tariffs, and now an economic shutdown, it has been a rough year and the stock prices reflect it. It’s worth noting that Flexsteel has been a bit more troubled than its peers, which is likely a function of its size – Bassett has roughly matched the performance of Flexsteel.

Valuation

There is no doubt that Flexsteel isn’t exactly a wonderful business between stagnating revenues, difficulty pivoting to e-commerce, and secular industry challenges. It is very much a “cigar butt” business – a bit gross, but practically free for the last puff or two.

Flexsteel sells at almost exactly 2/3rds of NCAV, with $62.5mm in cash, $34mm in receivables, and $90mm in inventory and other current assets. Flexsteel has increased their liabilities to shore up cash, with total liabilities of around $73.5mm and a market cap in the “sweet spot” for net-net stocks of $77mm. This depressed valuation suggests at least 50% upside, just on the discount to net current assets, while the stock traded just below $26 in the past year – a material premium to NCAV.

The stock has some interesting valuations relative to its peers – it commands a much lower P/B, a roughly in-line P/Sales, and a far higher EV/EBITDA. This makes it difficult to find a true comparison, and likely suggests that Flexsteel has quite a bit of room to improve on the profitability front. Comparisons to peers, especially BSET and HOFT, suggest that the market is valuing the stock more on revenues and assets than on the bottom line.

|

FLXS |

BSET |

HOFT |

ETH |

LZB |

|

|

EV/EBITDA |

40.23 |

13.81 |

9.63 |

8.01 |

9.81 |

|

P/Sales |

0.19 |

0.17 |

0.31 |

0.42 |

0.63 |

|

P/Book |

0.38 |

0.44 |

0.69 |

0.82 |

1.55 |

Governance

Flexsteel’s managers and board have demonstrated a remarkably pro-shareholder attitude, paying regular dividends for decades, taking large pay cuts during this crisis, and making difficult decisions like furloughs and divesting non-core business lines like commercial office products and RV furniture. CRO Jerry Dittmer has stated that cash preservation is a top priority, and, if need be, expenses will be slashed further.

Insiders also hold just over 5% of the stock and it is not dual-class – each equity stake has an equal vote and economic interest in the business. This makes Flexsteel an excellent candidate for an activist investor or a buyout, and protects the interests of minority shareholders from poor governance. This is a rare quality in a net-net stock – typically, firms that trade at large discounts to liquid assets alone have very serious governance problems.

On the April 29th earnings call and on their recent 8-K filing, a “review” of the dividend was discussed. Given the >10% yield and positive market reaction to the discussion, I believe a dividend cut would be quite appropriate, and extend Flexsteel’s cash runway by at least 15%.

On the call I floated the idea that if the board believes capital must be returned to shareholders, then they ought to reduce the $7mm dividend and use some of the savings to repurchase stock – though I would prefer we sit tight and wait for this to pass. Any critical examination of capital allocation policies is determinedly pro-shareholder, even if I may not agree with the particular outcome.

Catalysts

The obvious catalyst for just about any stock is the coronavirus pandemic ending – with vaccine trials and promising results from Gilead’s (GILD) remdesivir, a surprisingly fast end is far from impossible. However, it may very well go on for longer than the market is pricing for, which would be a negative for stocks as a whole.

When we inevitably re-open the country, Flexsteel stock is almost certainly going to rise, especially since they have been re-opening factories where it is safe to do so. However, we will likely need meaningful stimulus of aggregate demand to prop up GDP and by extension earnings – and Flexsteel is a cyclical stock, making it sensitive to consumer demand.

Additionally, divestments of non-core and poorly performing business lines (in this case, RV and hospitality) will streamline operations and possibly fetch a beneficial sale price when the time comes. Management has stated that they are in no rush to sell these businesses, and will not engage in a “fire sale” transaction.

Successful product launches and growing revenues would greatly enhance Flexsteel’s value, and the management team appears committed to keeping up with consumer trends. Their current product lineup is largely modern, comfortable, and feature-rich, and their marketing team is dedicated to cutting non-performing products while growing those that have consumer success.

Though the management team seems extraordinarily hesitant to spend cash, it is possible that they make a meaningful acquisition at some point in the future. This may drive the stock up, down, or sideways – most M&A activity is actually value-destructive – but is worth noting as a future catalyst for the stock’s value to be fully realized.

As with all net-net stocks, it is very possible that it simply creepy back up to net current asset value over some time. However, I believe that such depressed valuations with a higher-quality business are not sustainable, and an activist or buyout firm would eventually pounce on the opportunity once some economic uncertainty is removed. Flexsteel has a steep margin of safety and so long as consumer demand picks up eventually it would be difficult to lose money.

Risks

A major risk that practically all companies face is that of a continued shutdown that they simply cannot afford – a second wave, a lapse in social distancing, or hostile governments could all contribute to greater cash burn than Flexsteel’s balance sheet can handle. While I believe this is unlikely, investing with so many unknowns exposes risks that were not visible, or sometimes present, before.

This could precipitate a bankruptcy or a forced sale of the business at a price that is unfavorable to the common stock – however, given the lack of a controlling shareholder, this strikes me as extremely unlikely.

As with most cigar butt stocks, Flexsteel has an element of cash burn or net losses, and therefore may erode NCAV over time while driving down the share price. Slow-moving inventory and defaults on receivables may accelerate this process.

Strategy

Flexsteel is without a doubt my highest-conviction holding at this time. I believe net-net investing is done best in a diversified, equally-weighted portfolio of 10-30 names. This manner of portfolio management aligns with the statistical edge of investing with a steep margin of safety without sacrificing long-term returns. To learn more about investing in net-nets, feel free to read some of my other articles on the strategy, or check out Evan Bleker’s Net Net Hunter for more great resources.

The stock is dirt-cheap and ripe for an activist or buyout once some uncertainty evaporates, and is in an excellent position to weather the coronavirus pandemic even if it goes on substantially longer than expected. The steep discount to current assets net of all liabilities offers a practically unbeatable margin of safety, while the corporate structure and management team set the company up to outperform in the pandemic and moving forward from it.

Disclosure: I am/we are long FLXS. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment