monsitj/iStock via Getty Images

First Solar (NASDAQ:FSLR) is surging to new highs as the market becomes increasingly cognizant of the US surge of utility-scale solar deployments. This is on the back of an energy crisis and an Inflation Reduction Act reinvigorated drive to net zero. The Tempe, Arizona-based company recently released its fiscal 2022 third quarter which showed double misses on revenue and earnings but nonetheless caused its stock price to surge to an 11-year high.

The company has been able to capitalize on the domestic content requirements of the IRA to build new orders. Essentially, new utility-scale solar projects are eligible for a 10% domestic content credit if any manufactured product that’s a component of their project was produced in the United States. This drove continued demand for First Solar’s Made in USA thin film solar panels whose technology stack uses cadmium and telluride to provide advantages over conventional options like crystalline silicon. This means panels that are not only highly recyclable at end of life but that comes with a higher theoretical efficiency limit.

Critically, Made in USA now forms a material part of First Solar’s long-term bull case as the IRA is set to radically transform the green energy landscape over the next decade. First Solar is the largest solar manufacturing company in the USA and stands amidst this great ray of change as the controversial domestic content tax credits stand to boost the company’s pricing power with buoyant demand meaning its sold out until 2026.

A Solar Surge, Made In USA

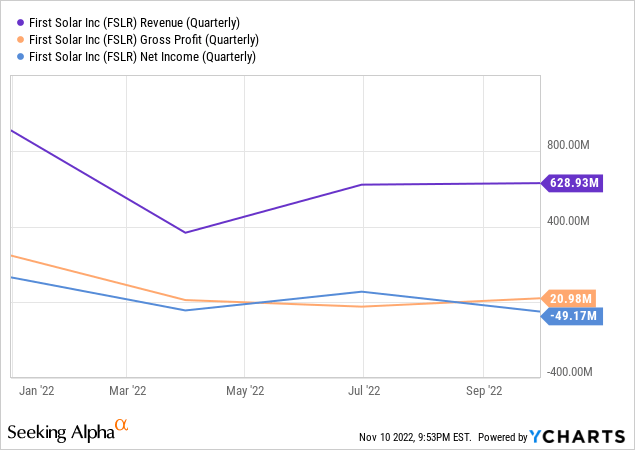

The company’s recent earnings report for its fiscal 2022 third quarter saw revenue come in at $628.93 million, a 7.8% increase from the year-ago quarter but a miss of $119 million on consensus estimates. This came on the back of 16.6 GW of new bookings during the quarter with a base average selling price of $0.316 per watt. Year-to-date bookings stood at 43.7 GW with the total backlog for future deliveries rising to a record 58.1 GW. This includes an agreement to supply Swift Current, a utility-scale solar energy developer, with 2 GW of thin film solar modules in 2025 and 2026.

The company manufactured 26.6 MWs per day as its Ohio manufacturing plant upgrade remains on schedule. First Solar is investing $185 million to expand production capacity by 0.9 GW for a cumulative annual production capacity of over 7 GW by 2025. Negative GAAP EPS of $0.46 was a miss by $0.28 on consensus estimates and a deterioration from positive EPS of $0.43 in the year-ago quarter. Bears have flagged this and the company’s low gross margins as reasons for concern.

The low single-digit gross profit margin of 3% during the quarter meant a gross profit of just $20.98 million. This was a fall from its year-ago figure and came with guidance for gross profit to be between $75 million to $110 million for the full fiscal year. This was a downward revision from prior guidance for gross profit to be between $115 million and $165 million. Net sales for the full fiscal year were also revised down to between $2.6 billion and $2.7 billion versus a prior ceiling of $2.8 billion.

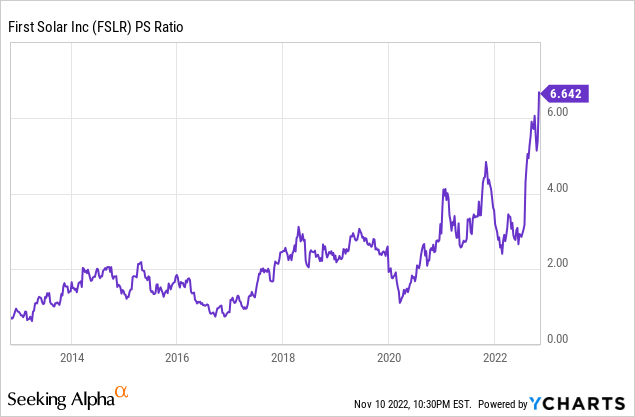

The company’s liquidity position stood at $1.9 billion at the end of the quarter but management stressed the need for raising more capital for its expansion needs with a new 3.5 GW facility planned for the US and continued international expansion in view. The most obvious choice would be an equity offering with its common shares trading at a significant premium to the 10-year average.

This premium has created a material level of risk for shareholders as a pullback is highly likely against a market still weary of broadly unprofitable companies in high-growth industries.

The Drive To Net Zero

First Solar’s rally is unique against the risk-off environment that has already collapsed valuations across the board for its peers but the enthusiasm is understandable. The IRA represents an 800-pound gorilla set to further bolster its industry already experiencing long-term structural growth. The domestic content requirements will inundate First Solar with orders and enhance its pricing power with there being no other Made in USA company of its scale.

The company has been a big winner from the historical growth of utility-scale solar. This is now set to experience a big bang in the decade ahead as national governments around the world make clean energy a critical building block for their post-pandemic economic recoveries and as part of their long-term response to the current energy crisis. But it is hard to recommend the company as a buy against its recent surge and with earnings that were mediocre at best. Hence, whilst the drive towards net zero through clean and renewable solar energy is picking up, the near-term outlook for First Solar is likely not great.

Be the first to comment