DarioGaona

While the gold and silver miners have enjoyed a multi-month rally, and this outperformance vs. other indices has continued into 2023, First Majestic (NYSE:AG) has been the proverbial runt of the litter. This is evidenced by its negative year-to-date performance and December return vs. a double-digit positive return for many of its peers. The reason? Not only did the company have a tough Q4 operationally, but its FY2023 outlook has left much to be desired, and the turnaround at Jerritt Canyon is moving slower than some had hoped. In fact, the asset will be lucky to produce 130,000 ounces this year, suggesting the 200,000-ounce per annum goal could be more elusive than previously anticipated.

Often, a tough quarter or softer full-year guidance can be an opportunity to pick up a high-quality name as it moves onto the sale rack. However, in the case of First Majestic, its valuation continues to be rich relative to what investors are getting for that price. Worse, the short and medium-term outlook regarding replacing reserves doesn’t appear to have become any more favorable after two years of inflationary pressures, while the silver price has struggled to remain above $22.00/oz on a sustainable basis. Let’s take a closer look below:

Jerritt Canyon Mine Operations (Company Presentation)

Q4 & FY2022 Production

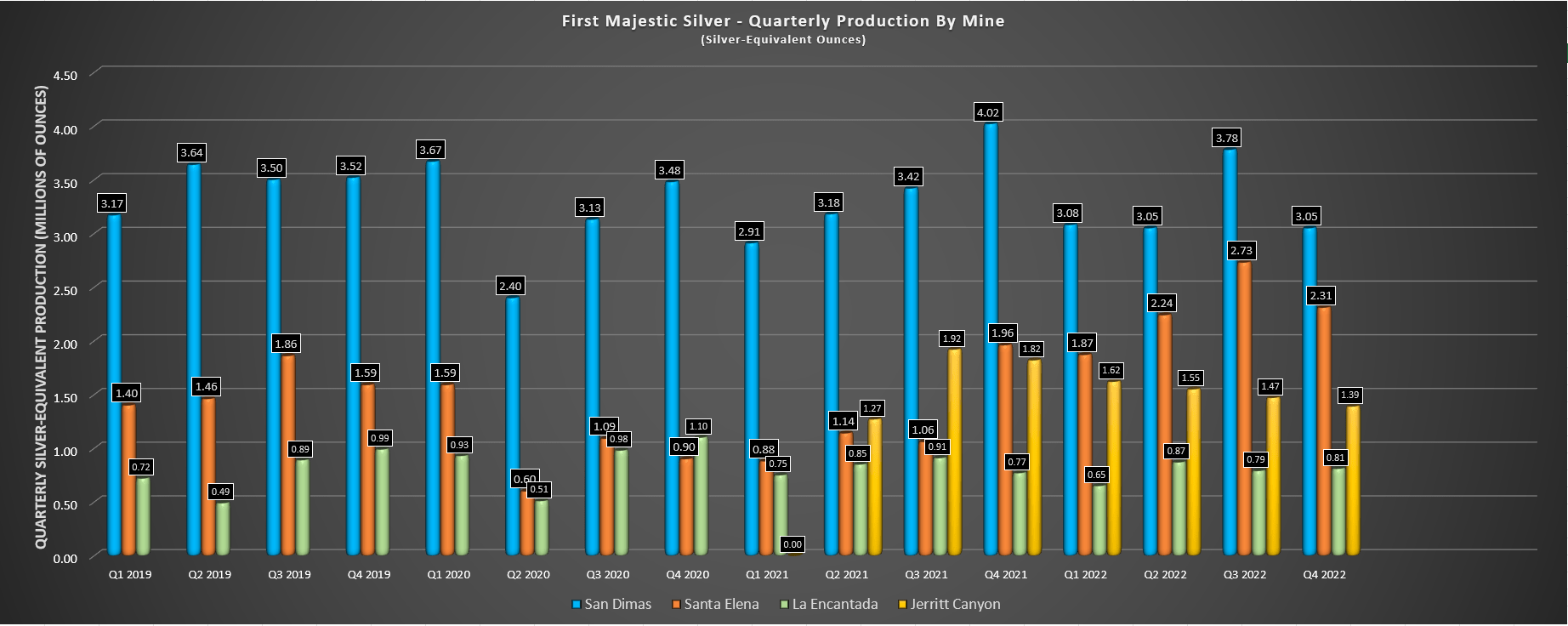

First Majestic Silver released its Q4 and FY2022 results this week, reporting quarterly production of ~2.40 million ounces of silver and ~63,00 ounces of gold. This represented an 18% decline in silver production on a year-over-year basis, with production impacted by the lower silver grades at Santa Elena, where ore feed is predominantly from Ermitano (gold-rich vs. silver-rich), with 80% of tonnes from the mine in Q4. Meanwhile, San Dimas saw a sharp dip in output year-over-year (3.05 vs. 4.02 million ounces), with the asset up against difficult comps year-over-year, impacted by lower grade development ore from the Perez vein. During the quarter, grades averaged 220 grams per tonne of silver and 3.12 grams per tonne of gold, down from 347 grams per tonne of silver and 3.71 grams per tonne of gold in Q4 2021.

First Majestic Silver – Quarterly Production by Mine (Company Filings, Author’s Chart)

Moving to La Encantada, production came in at ~805,000 ounces of silver, a 5% increase over prior-year levels. This was helped by slightly better grades and higher silver recoveries, offset by a dip in tonnes processed. The good news is that grades should improve by Q2 2023 with stope ore available from the Beca-Zone orebody. Overall, this resulted in a mixed year for its Mexican silver operations, with an exceptional year from Santa Elena (81% increase in silver-equivalent production) helped by Ermitano, offset by a weaker year at San Dimas and higher costs due to inflationary pressures. Meanwhile, the company’s newest operations hobbled through the year, and it ended on a low note, especially considering that Q4 was supposed to be much stronger for the Nevada asset, as discussed in the Q3 prepared remarks (shown below).

“However, we continue to anticipate a strong recovery at Jerritt Canyon in the fourth quarter and into early 2023 as Smith Zone 10, West Generator and Saval II mines come online in November. The inclusion of these new production areas are expected to increase ore deliveries to 3,000 tpd and substantially reduce costs.”

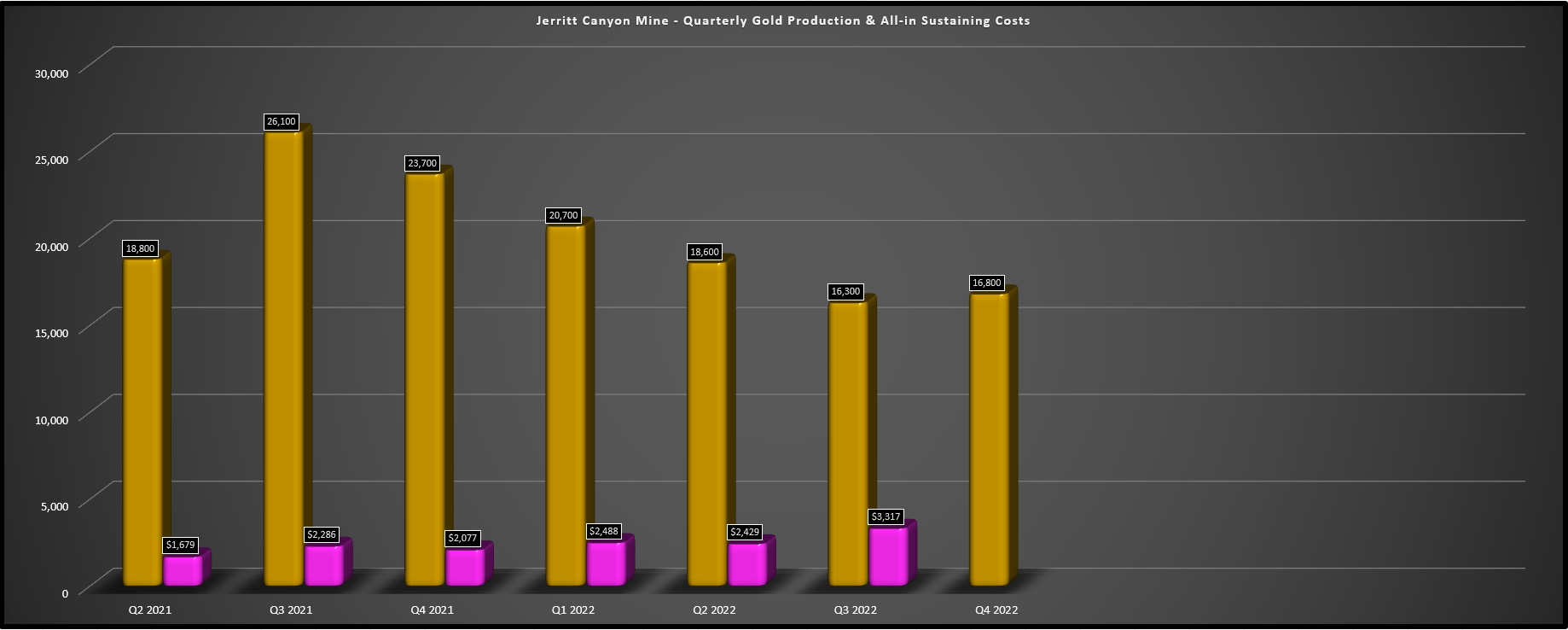

Unfortunately, not only was Q4 not a high point, it was near the low point for the quarter, with a measly 1,951 tonnes per day processed at grades well below my estimates. The result was that the mine produced just ~72,400 ounces in FY2022 and merely ~140,000 ounces since being acquired but at all-in-sustaining costs [AISC] that have averaged approximately $2,000/oz. In previous updates, I noted that there was minimal value in judging this asset during its turnaround phase and that it suffered from a lack of proper investment under previous owners. Instead, a better judge of its potential would be the 2023 and 2024 results once First Majestic had spent adequately on sustaining capital and had time to optimize the asset.

Jerritt Canyon Mine – Production & All-in Sustaining Costs (Company Filings, Author’s Chart)

However, judging by the 2023 guidance of 119,000 to 133,000 ounces at a $1,780/oz AISC mid-point, this turnaround could take longer than I anticipated, and the company’s remarks at the time of the acquisition look wildly ambitious, at least in terms of the timeline provided. Let’s take a closer look:

Jerritt Canyon Disappoints

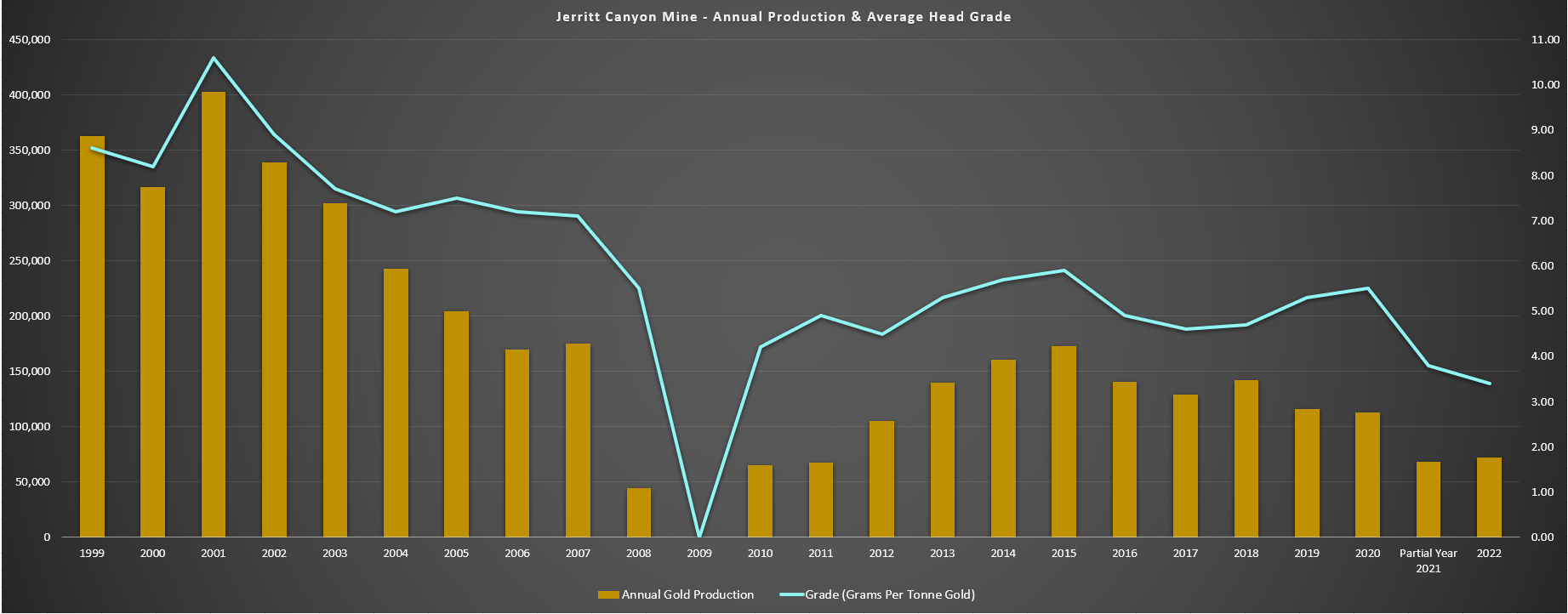

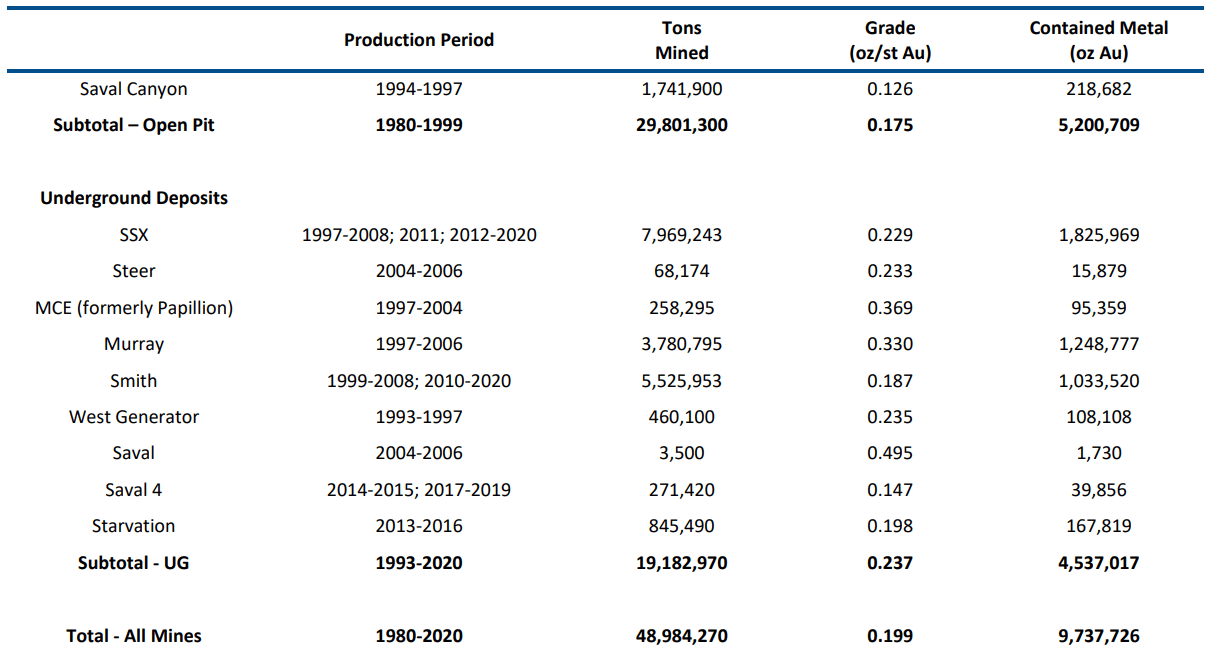

Looking at the chart below, Jerritt Canyon has seen a significant decline in annual production and grades since the turn of the century, going from a 300,000-ounce-per-annum operation to struggling to muster up a 150,000-ounce year over the past decade. Unfortunately, the past two years under First Majestic haven’t led to any change in this trend, with combined production from a partial year in 2021 and 2022 coming in below 150,000 ounces combined. As we can see, this dip in production has been grade-driven, with grades sliding to 3.80 grams per tonne of gold in 2021 and 3.4 grams per tonne of gold in 2022, down from 10.0+ grams per tonne of gold in 2001.

Jerritt Canyon Mine – Historical Production (Company Filings, Author’s Chart)

At the time of the acquisition, First Majestic’s management stated the following:

“This asset has not had a serious investment in developing our development or exploration for almost two decades or thereabouts. It used to be run by Freeport back in the 80s. It was a series of open pits. They got depleted at those metal prices. Today we think those pits can be reopened at the current metal prices, which we’re now evaluating, and we’re expecting to double the production here over the next couple of years. We’re actually expecting to have, in 2024, we’re expecting 200,000 ounces of gold – compared to 110,000 ounces this year (2021).”

– Gold Forum Americas, First Majestic Presentation

Clearly, the 2021 production goal did not meet expectations with a sub-100,000-ounce year for production, and betting against the outlook of 200,000 ounces in 2024 coming to fruition at this point is about as close to free money as one can get if a wager were available. This is because the only way this will occur is if the company processes at a rate of at least 4,000 tons per day and a 5.50 gram per tonne average grade, and it would still likely come up shy of this figure using 84% recoveries (~197,000 ounces vs. ~200,000 ounces). In fact, while the company appears proud to announce the ~70% increase in production year-over-year at the mid-point, this figure is miles below where this asset was guided to be from a cadence standpoint if it were to produce 200,000 ounces in 2024.

All that being said, there are some points to unpack, and while the 200,000-ounce goal by 2024 is far too ambitious, 2022 will likely be the low point for this asset.

Jerritt Canyon – Plant, Mines & Targets (Company Presentation)

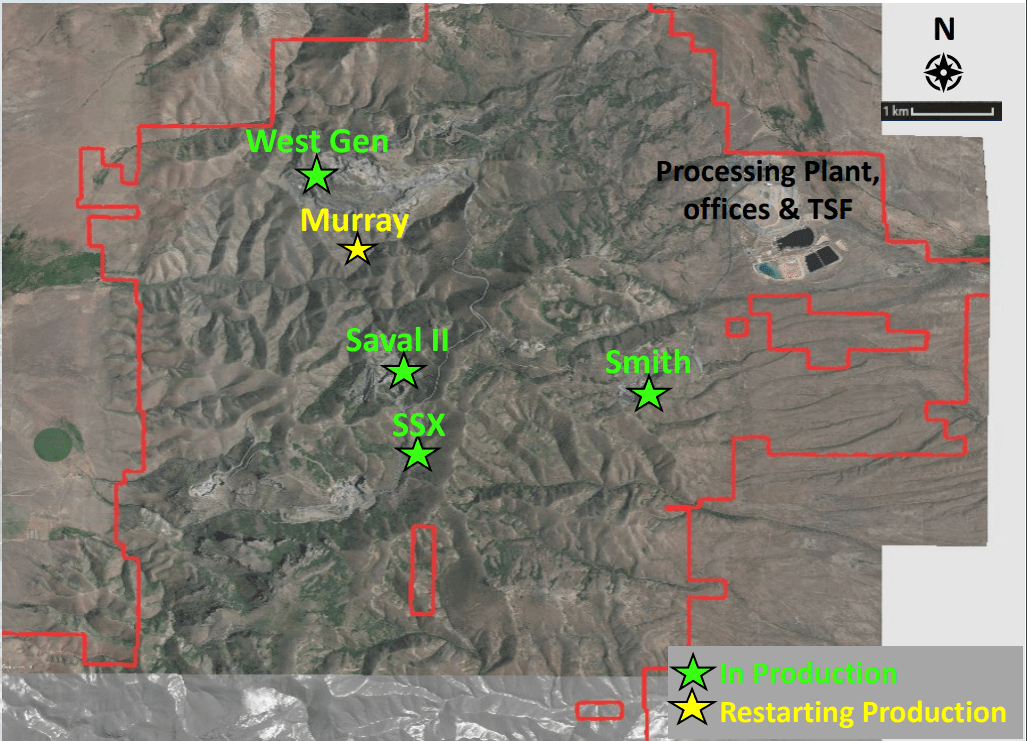

For starters, Q4 was a very tough quarter from a weather standpoint in Nevada, with multiple weeks of severe cold weather in Northern Nevada and double normal snowfall amounts that made ore haulage more challenging from its SSX and West Generator mines. The map above shows that these mines lie further from the plant than Smith. So, even if mined tonnes increased in Q4 to leverage fixed costs at the asset (considerable excess capacity of 4,000+ tons at the plant), it doesn’t help if those tonnes can’t efficiently make it to the plant to be treated to deliver the expected ore production. Some investors might note that this is just a convenient excuse, but I would disagree and think the company deserves a pass on the weak Q4 results.

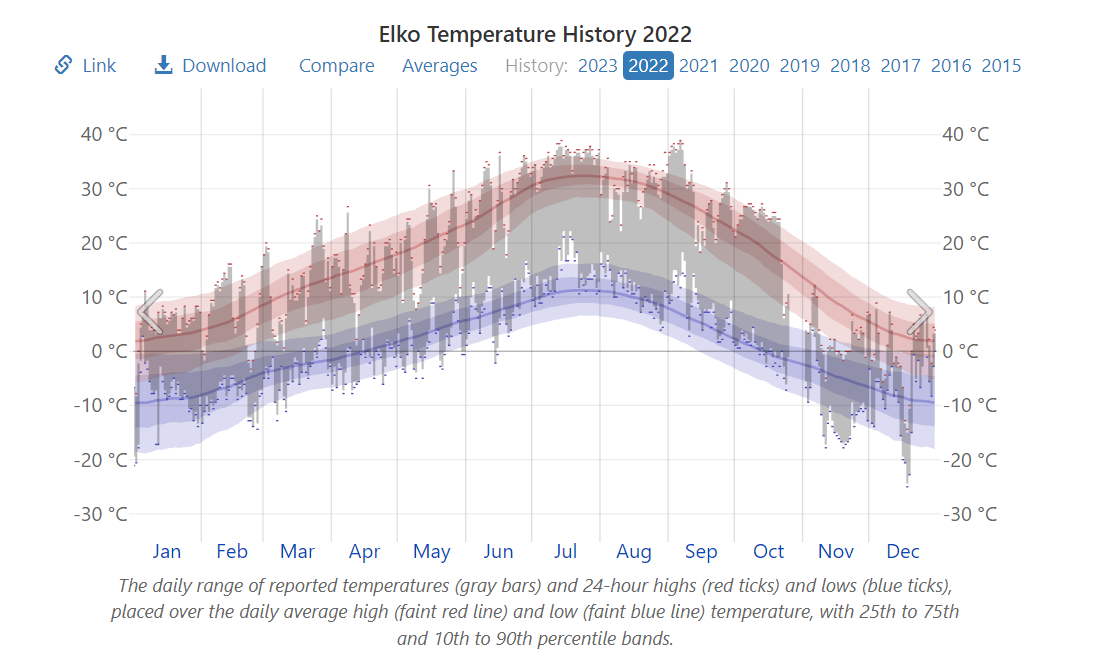

The weather in Elko, Nevada, is shown below, and it’s clear that November and December 2022 were much cooler than previous years, looking at the dataset, with temperatures consistently below 10 celsius and plunging below [-] 20 celsius on more than one occasion.

December 2022 Elko Temperature History vs. Averages (WeatherSpark.com)

Secondly, and in First Majestic’s defense, this is an asset running at barely 50% of its capacity (4,000+ tons per day), but the company is finally delivering on its goal of bringing new mining centers to take advantage of the significant capacity at the plant, similar to the mining complex model that Barrick (GOLD) employs in Nevada. This includes completing the secondary escape way in the West Gen Mine to increase ore production, ramping up the higher-grade Smith Zone 10, and it’s working on ramping up production from the previously shuttered Saval II Mine that sits just north of SSX. The result is that we should have four mines feeding the plant in 2023 vs. two in 2021, and the grades out of Smith should be better, with access to higher grades between the SSX and Smith Zones.

The result of this work is that we should see much higher grades in H1 2023 at Jerritt Canyon, and the goal is to have mined grades of ~5.4 grams per tonne of gold for FY2023, translating to a feed grade just shy of 5.0 grams per tonne of gold. Assuming an 83 – 84% recovery rate, this should translate to 120,000 plus ounces per annum and sub $1,800/oz AISC, a meaningful improvement from FY2022 levels ($2,000/oz plus AISC). Meanwhile, the company is looking to restart the high-grade Murray Underground Mine (1.24 million ounces produced historically at 10+ grams per ton of gold), providing additional incremental feed starting next year. Assuming a 6.0 gram per ton grade and a contribution of 700 tons per day, this could add another 35,000+ ounces to what looks to be a production profile of ~125,000 ounces per annum.

Jerritt Canyon – Historical Production (Technical Report 2021)

So, while this asset certainly doesn’t inspire any confidence based on its 2021 and 2022 production, First Majestic has made considerable progress that isn’t showing up in the Q4 or FY2022 results, and sustaining capital has been elevated in this period, with $55+ million spent since the project was acquired. Therefore, while the 2023 guidance was below my estimates from a production standpoint (~140,000 ounces) and well above my expectations of sub $1,700/oz AISC from a cost standpoint (actual guidance: $1,733/oz to $1,842/oz), 2024 has the potential to be a much better year.

To summarize, the worst results look to be in the rear-view mirror at Jerritt Canyon, and I remain cautiously optimistic about this asset. That said, I think a more conservative outlook is 140,000 to 155,000 ounces per annum (post-2024) at sub $1,700/oz AISC vs. the outlook provided at the time of the acquisition of ~200,000 ounces per annum at what would have been sub $1,500/oz AISC. In addition, I’d be remiss not to note from a negative standpoint, reserve replacement could be more challenging than expected due to inflationary pressures, with the possibility that the cut-off grade at the asset could increase towards 4.6 grams per ton of gold (previously: ~4.4 grams per ton of gold in the 2021 Technical Report), even if the company adjusts its gold price assumption to $1,550/oz or higher from $1,500/oz currently.

Putting It All Together

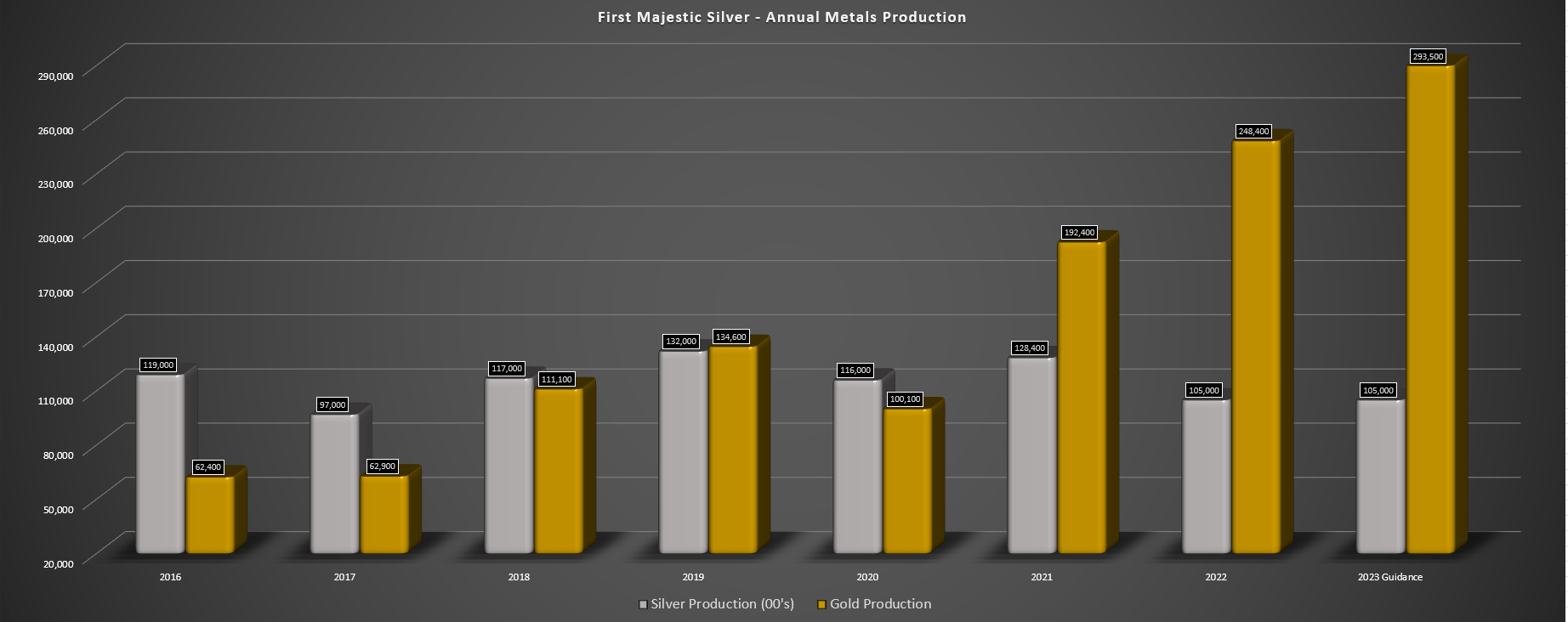

Given the softer year vs. what I expected at the company’s Jerritt Canyon Mine and lower silver production at Santa Elena, where mining will be solely focused on the higher-grade Ermitano ore, First Majestic expects to produce ~293,000 ounces of gold and ~10.6 million ounces of silver. This would translate to silver production remaining at multi-year lows (2021: ~12.8 million ounces), offset by a significant increase in gold production, which would increase 120% above 2019 levels (~135,000 ounces produced). However, although production is moving in the right direction, the trend in production per share has been less impressive, impacted by significant share dilution from the Jerritt Canyon acquisition.

Meanwhile, from a consolidated cost standpoint, First Majestic’s all-in-sustaining costs per silver-equivalent ounce [SEO] are expected to come in at $18.47/oz to $19.72/oz, providing little margin for error if we assume a more conservative silver price of $22.00/oz for the year. Worse, these costs are up substantially from FY2022 guidance (which the company will miss due to production shortfalls in Q4), which was set at $17.68/oz to $18.42/oz. So, while consolidated production may increase 10% year-over-year in 2023, the higher cost profile largely offsets this.

The result is that First Majestic Silver is really becoming First Majestic Gold (a negative development given that gold producers typically trade at lower multiples), and the company has razor-thin margins until Jerritt Canyon is optimized post-2023, or unless metals prices increase substantially. Hence, I don’t see any hope of this stock returning to the $13.00 per share level any time soon, let alone $17.00. This means that many silver apes that rushed into the stock to participate in the silver squeeze promises by some analysts are likely to create overhead resistance for the stock and lead to sharp rallies being sold as these become impatient after holding a losing investment, while other silver producers simultaneously outperform.

Valuation & Technical Picture

Based on ~286 million shares outstanding and a share price of US$8.10, First Majestic trades at a market cap of ~$2.32 billion. Even after the recent share-price decline, this still compares unfavorably with an estimated net asset value of $980 million. In fact, after dividing First Majestic’s market cap by its estimated net asset value, we can see that the stock has one of the highest multiples sector-wide, trading at nearly 2.30x P/NAV. This is despite ~70% of revenue coming from a Tier-2 jurisdiction (Mexico). Plus, the company now has a greater proportion of revenue from gold which should lower the premium multiple it commanded in 2016 due to being primarily a silver producer.

Following the acquisition of the Jerritt Canyon Mine and the higher gold grades at Ermitano vs. Santa Elena, First Majestic’s percentage of revenue coming from gold has increased substantially vs. 2016 levels (shown below).

First Majestic Silver – Annual Metals Production & 2023 Guidance (Company Filings, Author’s Chart)

Historically, I haven’t found any value in paying more than 1.25x P/NAV for a gold/silver miner. The only exceptions are when said company is a proverbial unicorn (industry-leading margins, high double-digit production growth, and all operations in Tier-1 jurisdictions), like Kirkland Lake Gold was from 2017-2019. This is certainly not the case with First Majestic, whose only Tier-1 jurisdiction asset has underperformed expectations; its consolidated AISC margins are below 20% at a more conservative $22.00/oz silver price, and it will be lucky to grow annual production by more than 10% this year. So, with First Majestic continuing to trade at one of the highest P/NAV multiples sector-wide, I continue to see zero margin of safety from a valuation standpoint.

The good news is that a rising tide will lift all boats, and while First Majestic had a rough year in 2022 with significant misses on guidance, it should see an improvement in margins if the gold and silver prices can continue their upward trajectory. However, even if this is the case, the goal should be to buy high-quality companies that consistently deliver on promises at a deep discount to fair value. Regarding turnarounds or companies that have struggled to meet promises, one should demand a more significant margin of safety to compensate for the negative sentiment that could weigh on the stock, the lower probability of flawless execution, and the higher risk. Given that First Majestic fits in the second category yet is one of the most expensive, I don’t see any way to justify being long here at US$8.10.

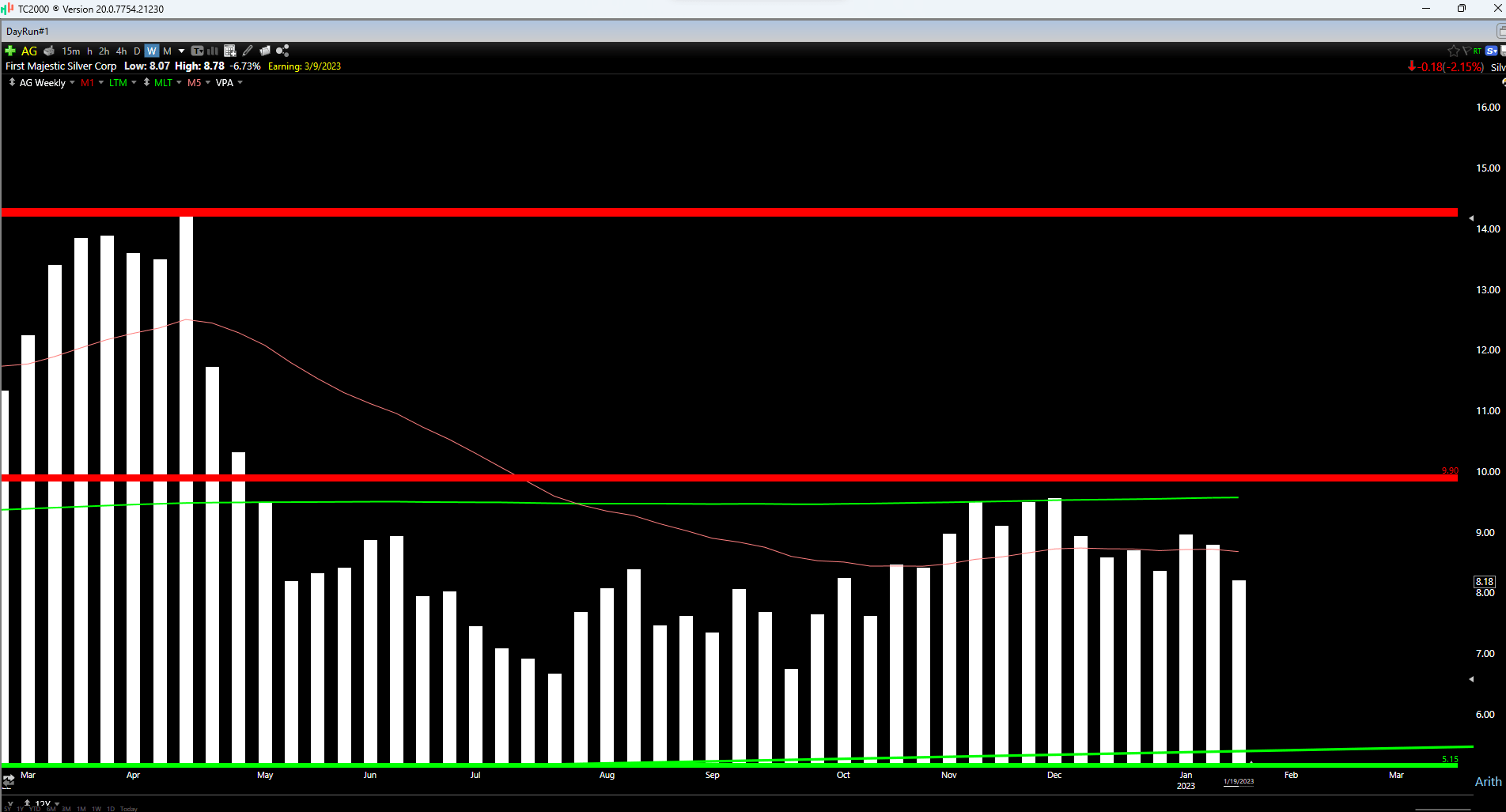

AG Weekly Chart (TC2000.com)

Finally, if we look at the technical picture, we can see that while AG has pulled back sharply from its recent highs, it’s still sitting in the upper portion of its expected support/resistance range. This is based on the stock having no strong support until the US$5.15 – US$5.35 region and strong resistance overhead at US$9.90 to US$10.10. If we measure from a current share price of US$8.10, this translates to $2.75 in potential downside to support and just $2.00 in potential upside to the upper edge of resistance, translating to a reward/risk ratio of 0.73 to 1.0. I prefer a minimum of a 5.0/1.0 reward/risk ratio to justify starting new positions in small/mid-cap names, meaning that AG is still not in a low-risk buy zone and would need to dip below US$6.00 to become more interesting.

Summary

While First Majestic has guided for a much better year ahead, the outlook was well below my previous estimates. In addition, while I was cautiously optimistic about Jerritt Canyon being a ~170,000-ounce producer at sub $1,450/oz AISC in 2024, I’m less confident in this outlook based on what’s been stickier inflation than expected. Plus, adding reserves could be tougher than previously anticipated, given that cut-off grades should increase vs. the 2021 report. So, while this asset could generate a decent amount of cash flow in a $2,000/oz+ gold price environment, even with a more conservative outlook of 145,000 ounces per annum annualized run rate starting in Q2 2024 at sub $1,650/oz AISC, the asset’s future is much less rosy in a weaker gold price environment (sub $1,800/oz).

To summarize, the one piece of this story that could lead to a re-rating (Jerritt Canyon in Nevada) hasn’t lived up to expectations, and I don’t expect reserve replacement to get much easier for silver producers in general (nor Jerritt Canyon), with inflationary pressures impacting cut-off grades at all operations. Meanwhile, although production is rising, costs are rising in line with costs, and after a rough year of missing estimates, the market may be less anxious to assign the premium multiple the stock has commanded in previous years. Hence, with First Majestic trading at a premium to other precious metals names, I continue to see limited relative value in the stock, suggesting the stock is best to Avoid unless we see much lower prices.

Be the first to comment