omersukrugoksu/iStock via Getty Images

The margin’s high-rate sensitivity will boost the earnings of First Financial Bancorp. (NASDAQ:FFBC) through the end of 2023. Further, mid-single-digit loan growth will support the bottom line. On the other hand, the normalization of provisioning expenses for loan losses will limit earnings growth. Overall, I’m expecting First Financial Bancorp. to report earnings of $2.22 per share for 2022, up 4% year-over-year. For 2023, I’m expecting earnings to grow by 13% to $2.52 per share. The year-end target price suggests a small upside from the current market price. Based on the total expected return, I’m adopting a buy rating on First Financial Bancorp.

Loan Mix Well Positioned for the Rising Rate Environment

The average loan yield is quite rate-sensitive because the loan portfolio is heavy on commercial and industrial (“C&I”) and commercial real estate (“CRE”) loans, which make up around three-quarters of the loan portfolio. These loans are mostly based on variable or adjustable rates. On the contrary, residential real estate loans (10% of total loans) are mostly based on fixed rates, according to details given in the 10-Q filing.

On the other side of the balance sheet, the deposit book is also quite rate-sensitive. Interest-bearing demand and savings deposits made up a sizable 58% of total deposits at the end of June 2022. These deposits will reprice quickly after every rate hike, thereby holding back the margin.

The large balance of securities will also hold back the margin’s expansion as most securities are based on fixed rates. Available-for-sale and held-to-maturity securities made up 29% of total earning assets at the end of June 2022.

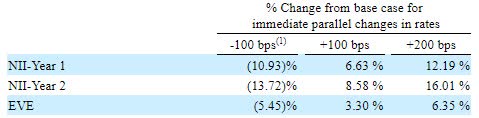

The results of the management’s interest-rate sensitivity analysis given in the 10-Q filing show that the margin is highly rate-sensitive, though part of the impact comes with a lag. According to the management’s analysis, a 200-basis points hike in interest rates can boost the net interest income by 12.19% over the first year and 16.01% over the second year of the rate hike.

2Q 2022 10-Q Filing

Considering these factors, I’m expecting the margin to increase by 40 basis points in the second half of 2022 and 20 basis points in 2023.

Loan Growth Likely to Revert to the Mid-Single-Digit Range

After declining for four consecutive quarters, the loan portfolio grew by 2.0% in the second quarter of 2022, or 8.1% annualized. The second quarter’s performance was remarkable as it was higher than in previous years. The loan book has grown in the mid-single-digit range in the past. I’m expecting the growth rate to return to the historical norm in the second half of this year mostly because of high interest rates that will curtail credit demand.

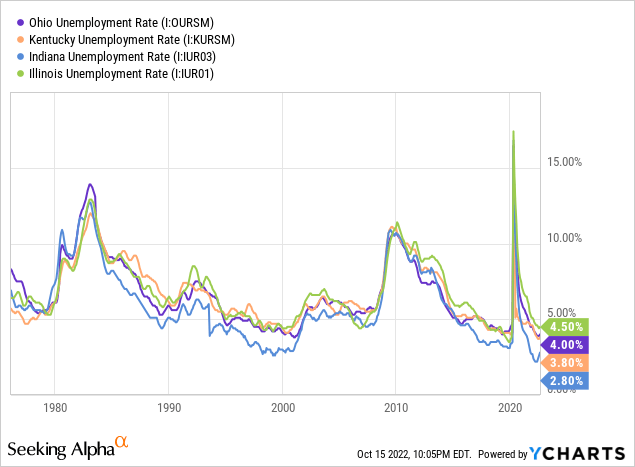

On the other hand, strong job markets will support loan growth. First Financial Bancorp. operates mostly in Ohio, Kentucky, Indiana, and Illinois. Out of these states, only Indiana has an unemployment rate that’s below the national average. Nevertheless, the job markets of all four states have improved remarkably in a historical context.

In January 2022, First Financial Bancorp. completed the acquisition of Summit Funding Group, an equipment financing platform. The acquisition has seen early success as equipment finance loans were up by 34% in the first half of this year, as compared to a decline of 7% in the corresponding period last year. I’m expecting this new platform to further support loan growth.

Considering these factors, I’m expecting the loan portfolio to grow by 1.25% every quarter till the end of 2023.

The Trend of Reserve Releases to Reverse Soon

First Financial Bancorp. released provisions for loan losses for the last five consecutive quarters. In my opinion, this trend will reverse in the second half of the year because of high inflation. Further, interest rates are now higher than before, which will worsen the portfolio’s credit quality. I’m not too worried though because the existing allowance level is quite high relative to the portfolio’s credit risk. According to details given in the 10-Q filing, the allowances-to-nonaccrual-loans ratio rose to 302.9% by the end of June 2022 from 272.8% at the end of December 2021.

Considering these factors, I’m expecting the net provision expense to revert to the historical norm in the second half of 2022. I’m expecting the net provision expense to make up 0.20% of total loans (annualized) every quarter till the end of 2023. In comparison, the net provision expense averaged 0.19% of total loans from 2017 to 2019.

Expecting Earnings to Grow by 4%

The anticipated loan growth and significant margin expansion will lift earnings through the end of 2023. On the other hand, provision normalization will curtail earnings growth. Overall, I’m expecting First Financial Bancorp. to report earnings of $2.22 per share for 2022, up 4% year-over-year. For 2023, I’m expecting earnings to grow by 13% to $2.52 per share.

First Financial Bancorp. is scheduled to announce its third-quarter results on October 20, 2022. I’m expecting the company to report earnings of $0.62 per share for the quarter, around 13% higher than the second quarter’s earnings of $0.55 per share.

The following table shows my annual income statement estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |||||

| Income Statement | ||||||||||

| Net interest income | 449 | 484 | 457 | 452 | 488 | 574 | ||||

| Provision for loan losses | 15 | 30 | 71 | (18) | 3 | 20 | ||||

| Non-interest income | 103 | 131 | 189 | 172 | 189 | 199 | ||||

| Non-interest expense | 324 | 342 | 391 | 401 | 416 | 462 | ||||

| Net income – Common Sh. | 173 | 198 | 156 | 205 | 210 | 238 | ||||

| EPS – Diluted ($) | 1.93 | 2.00 | 1.59 | 2.14 | 2.22 | 2.52 | ||||

|

Source: SEC Filings, Earnings Releases, Author’s Estimates (In USD million unless otherwise specified) |

||||||||||

Actual earnings may differ materially from estimates because of the risks and uncertainties related to inflation, and consequently the timing and magnitude of interest rate hikes. Further, a stronger or longer-than-anticipated recession can increase the provisioning for expected loan losses beyond my estimates.

Rising Interest Rates to Hurt Equity Book Value

First Financial Bancorp. has a large balance of available-for-sale securities on its books, which will hurt the stock’s valuation amid a rising rate environment. Available-for-sale securities made up 28% of total earning assets at the end of June 2022. As interest rates increase, the market value of fixed-rate available-for-sale securities will fall, leading to unrealized losses. These losses will directly reduce the equity book value without affecting the income statement.

First Financial Bancorp.’s equity has already dropped by 8% over the first half of the year due to unrealized mark-to-market losses. Further attrition is likely in the third quarter because the Federal Reserve has increased the fed funds rate by 150 basis points during the quarter. Moreover, the Fed projects another 125 to 150 basis points hike in rates by the end of 2023.

Considering these factors, I’m expecting unrealized losses to reduce the equity book value by 2% in the second half of 2022. On the other hand, retained earnings will lift the equity book value. The following table shows my balance sheet estimates.

| FY18 | FY19 | FY20 | FY21 | FY22E | FY23E | |

| Financial Position | ||||||

| Net Loans | 8,768 | 9,144 | 9,725 | 9,156 | 9,537 | 10,022 |

| Growth of Net Loans | 47.1% | 4.3% | 6.4% | (5.9)% | 4.2% | 5.1% |

| Other Earning Assets | 3,366 | 3,191 | 3,751 | 4,654 | 4,314 | 4,401 |

| Deposits | 10,140 | 10,210 | 12,232 | 12,872 | 12,524 | 13,032 |

| Borrowings and Sub-Debt | 1,611 | 1,731 | 943 | 706 | 1,273 | 1,312 |

| Common equity | 2,078 | 2,248 | 2,282 | 2,259 | 2,092 | 2,244 |

| Book Value Per Share ($) | 23.2 | 22.7 | 23.3 | 24.1 | 22.2 | 23.8 |

| Tangible BVPS ($) | 12.9 | 12.5 | 13.0 | 12.5 | 10.7 | 12.3 |

|

Source: SEC Filings, Author’s Estimates (In USD million unless otherwise specified) |

Adopting a Buy Rating Due to a Moderately-High Total Expected Return

First Financial Bancorp. is offering a dividend yield of 4.0% at the current quarterly dividend rate of $0.23 per share. The earnings and dividend estimates suggest a payout ratio of 36.5% for 2022, which is below the five-year average of 46%. Therefore, there is room for a dividend hike. Nevertheless, I’m not expecting any change in the dividend level because First Financial Bancorp. does not increase its dividend regularly.

I’m using the historical price-to-tangible book (“P/TB”) and price-to-earnings (“P/E”) multiples to value First Financial Bancorp. The stock has traded at an average P/TB ratio of 1.93 in the past, as shown below.

| FY17 | FY18 | FY19 | FY20 | FY21 | Average | |

| T. Book Value per Share ($) | 11.6 | 12.9 | 12.5 | 13.0 | 12.5 | |

| Average Market Price ($) | 26.8 | 29.2 | 24.6 | 16.1 | 23.5 | |

| Historical P/TB | 2.31x | 2.26x | 1.97x | 1.23x | 1.88x | 1.93x |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/TB multiple with the forecast tangible book value per share of $10.7 gives a target price of $20.7 for the end of 2022. This price target implies an 11.2% downside from the October 14 closing price. The following table shows the sensitivity of the target price to the P/TB ratio.

| P/TB Multiple | 1.73x | 1.83x | 1.93x | 2.03x | 2.13x |

| TBVPS – Dec 2022 ($) | 10.7 | 10.7 | 10.7 | 10.7 | 10.7 |

| Target Price ($) | 18.5 | 19.6 | 20.7 | 21.7 | 22.8 |

| Market Price ($) | 23.3 | 23.3 | 23.3 | 23.3 | 23.3 |

| Upside/(Downside) | (20.4)% | (15.8)% | (11.2)% | (6.6)% | (2.0)% |

| Source: Author’s Estimates |

The stock has traded at an average P/E ratio of around 13.2x in the past, as shown below.

| FY17 | FY18 | FY19 | FY20 | FY21 | Average | |

| Earnings per Share ($) | 1.56 | 1.93 | 2.00 | 1.59 | 2.14 | |

| Average Market Price ($) | 26.8 | 29.2 | 24.6 | 16.1 | 23.5 | |

| Historical P/E | 17.2x | 15.2x | 12.3x | 10.1x | 11.0x | 13.2x |

| Source: Company Financials, Yahoo Finance, Author’s Estimates | ||||||

Multiplying the average P/E multiple with the forecast earnings per share of $2.22 gives a target price of $29.3 for the end of 2022. This price target implies a 25.8% upside from the October 14 closing price. The following table shows the sensitivity of the target price to the P/E ratio.

| P/E Multiple | 11.2x | 12.2x | 13.2x | 14.2x | 15.2x |

| EPS 2022 ($) | 2.22 | 2.22 | 2.22 | 2.22 | 2.22 |

| Target Price ($) | 24.8 | 27.0 | 29.3 | 31.5 | 33.7 |

| Market Price ($) | 23.3 | 23.3 | 23.3 | 23.3 | 23.3 |

| Upside/(Downside) | 6.7% | 16.2% | 25.8% | 35.3% | 44.9% |

| Source: Author’s Estimates |

Equally weighting the target prices from the two valuation methods gives a combined target price of $25.0, which implies a 7.3% upside from the current market price. Adding the forward dividend yield gives a total expected return of 11.2%. Hence, I’m adopting a buy rating on First Financial Bancorp.

Be the first to comment