US Dollar Fundamental Talking Points:

- US Growth Is Still Leading the Developed World

- The Fed’s Timetable and the Market’s Patience

- Always the Possibility of a Crisis

The US Dollar had everything aligned to its favor through the first half of 2021 and yet the currency struggled to gain serious traction. Some may say that the benchmark currency was merely playing out the role of an unwanted safe haven as the capital markets continued their post-pandemic climb, but I don’t believe that to be necessarily the case. The same appetite for return in this speculative environment finds the Greenback in good position to draw capital to trend leaders like the S&P 500 pushing a record high or local yields bolstered by a rising 10-year Treasury as its baseline. The struggle arose from the Federal Reserve’s diligent effort to undermine surprise.

It seems to be a fairly clear path heading into the second half of the year that the US central bank will announce its plans to slowly pull back from its extraordinary munificence by first unveiling the plans for a taper. However, the timing for that announcement is up for debate and Chairman Powell is taking incredible pains to draw all of the surprise and impact from the official start – the exact spark that leads to meaningful market adjustment. So, even as the US enjoys competitive rates of growth and market yield forecasts, it may be a struggle for the Dollar to find serious traction…unless a severe risk downturn were to strike.

US Growth Is Still Leading the Developed World

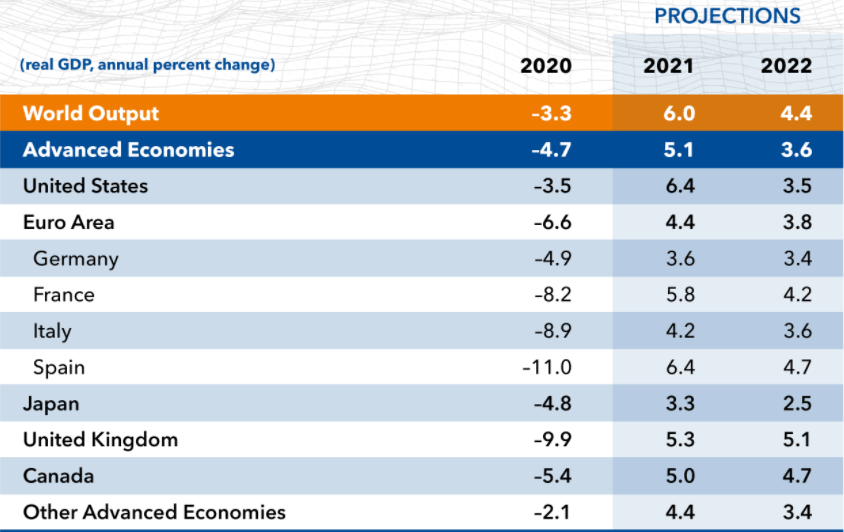

In a world where the ‘efficient market hypothesis’ held to its rudimentary interpretation, the Dollar should outperform its major counterparts on the sheer basis of its economic performance and outlook. Through the June Markit PMI figures (composite), the proxies for GDP showed that the US was sporting the fastest clip of expansion of all its major counterparts – including the Eurozone, UK and Japan. Looking further afield, the outlook for growth further favors the Greenback according to the IMF’s forecasts, which raised the tempo from a 5.1 percent projection in January to 6.4 percent in April. That is on the basis of large fiscal and monetary infusions and a drive to reopen the economy with vaccinations against the coronavirus. As promising as this looks, the general reopening of the global economy waters down the relative appeal the Dollar would otherwise enjoy. In a zero-rate environment, capital gains matter more than yield.

Chart 1: IMF Global Growth Projections From World Economic Outlook Report (April 2021)

{kind=link}

Source: Table from IMF April WEO

The Fed’s Timetable and the Market’s Patience

The critical consideration on my – and I’m sure many other market participants’ – radar for the third quarter is the timetable of the Fed’s plans to reverse its monetary policy largesse. The group’s favorite inflation indicator hit its fastest clip of year-over-year growth in three decades in with its May update. At the June monetary policy announcement, the central bank took pains to avoid any admission that it would soon begin its taper, but the rate forecasts component of its Summary of Economic Projections (SEP) moved the time table for hikes sharply forward. The steering committee now expects two rate hikes by the end of 2023, though there is debate over whether a move will occur in 2022.

On the other hand, the market seems to believe a hike will indeed come by the end of next year, referring to implied rates from Fed Funds futures. That may seem a long ways off, but the markets are forward-looking and there will be adjustments that will precede ‘lift off’. An FOMC survey showed people expect the timeline would be: taper begins; followed by an end to asset purchases three quarters later; followed then by the first rate hike three quarters after that. That would suggest the announcement of these plans will come in the first few months of the third quarter. There is a FOMC decision on July 28th and the Jackson Hole Symposium taking place from August 26th through 28th. I don’t believe the market has priced this shift in fully, but the uncertainty for this development to unfold could make for some difficult trading conditions before it is clear.

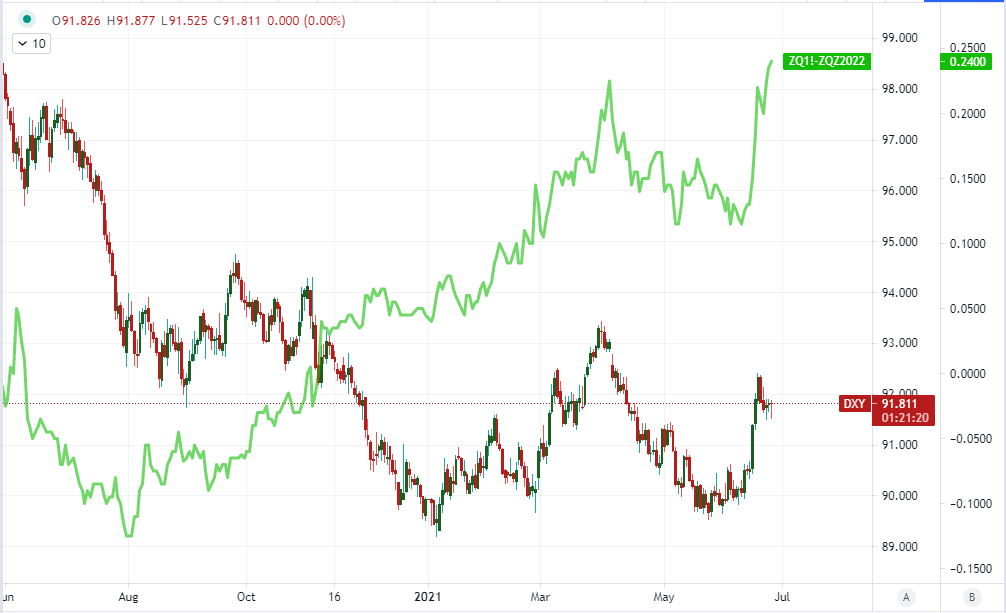

Chart 2: DXY Dollar Index and Implied Dec 2022 Fed Funds Change (Daily)

Source: TradingView; Prepared by John Kicklighter

Always the Possibility of a Crisis

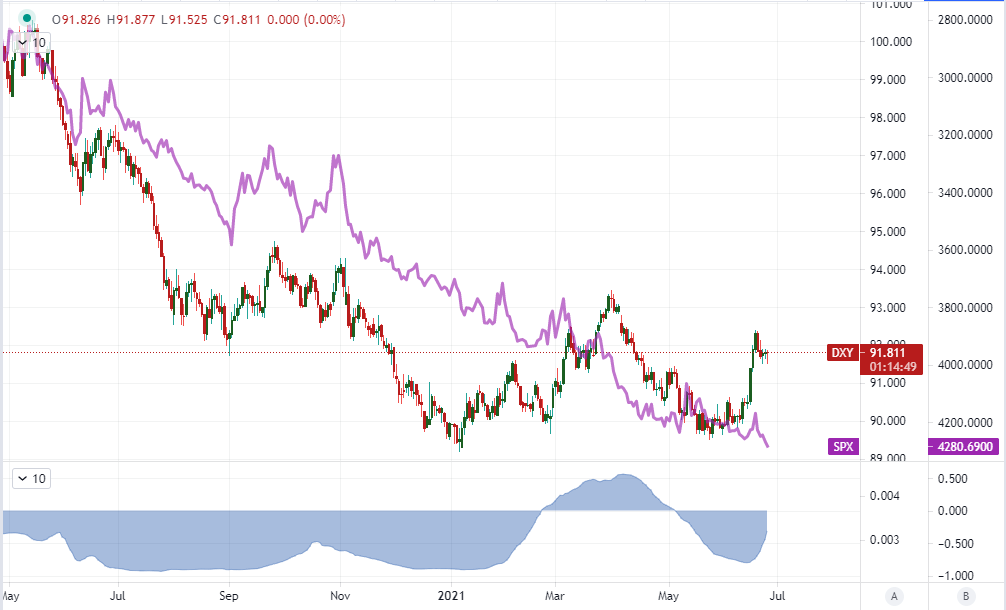

Finally, it is important to consider the Greenback’s connection to risk trends when moving forward. In extreme conditions of risk aversion, it quickly dons the robe of a safe haven of last resort. However, the threat of a full-scale financial collapse is a low probability even if there are worries of excessive leverage throughout the financial system. In more moderate periods of risk-on and risk-off, the sentiment influence tends to flag significantly. That may seem to contradict a chart that shows the Dollar relative to a sentiment torchbearer like the S&P 500, but correlation does not imply motivation. Should risk appetite continue to climb at a measured pace through the coming quarter, I don’t suspect it would lead the currency to an utter collapse. Nonetheless, the pursuit of yield for the excess funds that are being pumped into the US system would still favor targets like emerging markets or even larger counterparts that happen to have started their slow firming of monetary policy, like the Bank of Canada or Central Bank of Mexico.

Chart of DXY Dollar Index Overlaid with S&P 500 and 60-Day Correlation (Daily)

Source: TradingView; Prepared by John Kicklighter

To read the full US Dollar forecast including the technical outlook, download our new 3Q trading guide from the DailyFX Free Trading Guides!

.

Be the first to comment