G0d4ather

Thesis

First Trust Senior Floating Rate Income Fund II (NYSE:FCT) is a fixed income closed end fund. As per its literature:

The primary investment objective of the Fund is to seek a high level of current income. As a secondary objective, the Fund attempts to preserve capital. The Fund pursues its objectives by investing primarily in a portfolio of senior secured floating-rate corporate loans (“Senior Loans”). Under normal market conditions, at least 80% of the Fund’s Managed Assets are generally invested in a diversified portfolio of Senior Loans. “Managed Assets” means the total asset value of the Fund minus the sum of its liabilities, other than the principal amount of borrowings. There can be no assurance that the Fund will achieve its investment objectives. Investing in Senior Loans involves credit risk and, during periods of generally declining credit quality, it may be particularly difficult for the Fund to achieve its secondary investment objective

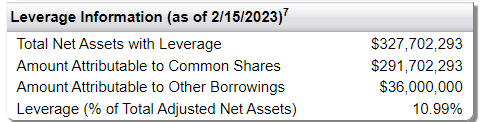

What makes this CEF stand-out for us is its very low leverage ratio:

Fund Leverage (Fund Website)

The fund’s leverage is currently at 11%, which is extremely small for the floating loan space which usually sees 30% leverage ratios for a standard build. The set-up is good for the current market, where we are expecting to see another leg down in this structural bear. However, unless the manager pumps up the leverage post the downturn, the CEF is going to underperform.

The floating rate loan asset class is the perfect asset for leverage, given its low standard deviation. That is why lev loan CEFs are so successful and stable, even at 30% to 35% leverage ratios.

The fund has an average build, with a couple of individual chunky names, but nothing unusual in its collateral. Longer term the fund underperforms the likes of Invesco Senior Income Trust (VVR) and Apollo Tactical Income Fund (AIF) which are golden standards in the space.

Given the current market cycle and low leverage, coupled with its discount, makes FCT attractive for now, although long term this is not an outperformer in the space.

Analytics

AUM: $0.26 billion.

Sharpe Ratio: 0.13 (3Y).

Std. Deviation: 11 (3Y).

Yield: 8.2%.

Premium/Discount to NAV: -10%.

Z-Stat: -0.8.

Leverage Ratio: 11%

Holdings

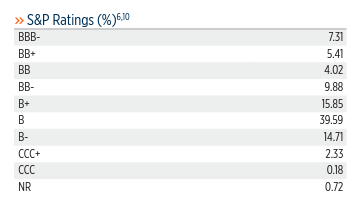

The fund does not have an aggressive asset composition when it comes to credit risk:

Ratings (Fund Website)

We can see from the credit rating parsing that the CCC bucket is fairly small, with the fund being overweight ‘B’ names. So we like the fact that the fund is not overcompensating the lack of leverage with an aggressive credit selection.

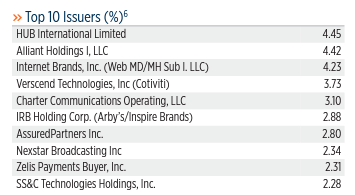

Its individual name composition is however a bit chunky:

Top Issuers (Fund Fact Sheet)

Usually we see individual names at a maximum of 2% of portfolios, especially for leveraged loan funds. This CEF takes some individual credit concentration in a couple of names which come in above a 4% weighting.

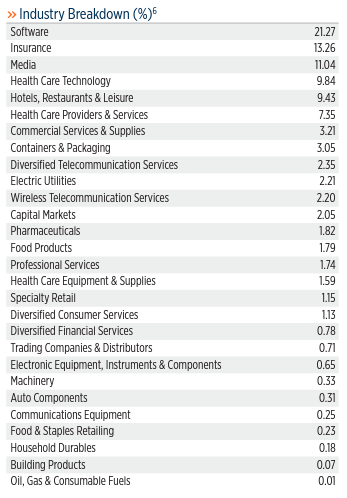

From an industry perspective the fund is concentrated in Software and Insurance:

Sectors (Fund Fact Sheet)

Performance

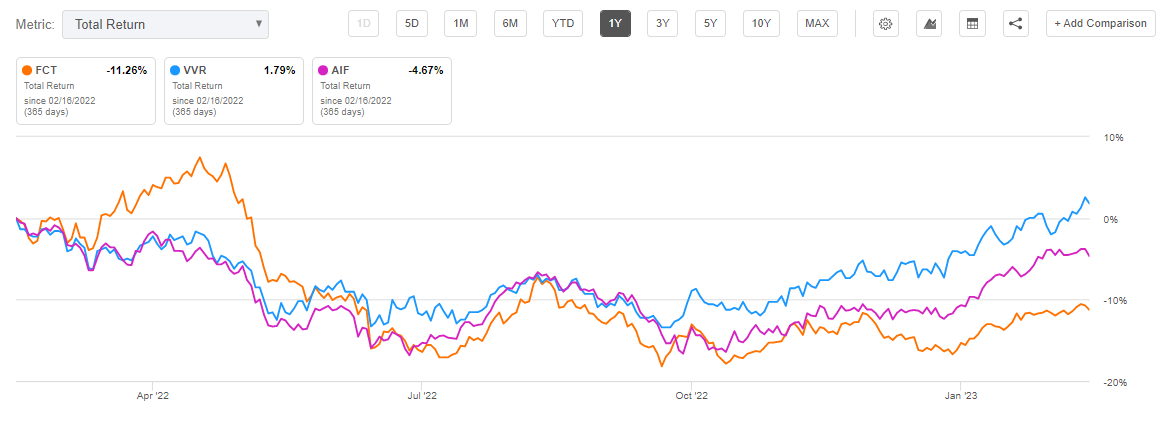

The CEF is down in the past year:

Total Return (Seeking Alpha)

Despite its low leverage (which is supposed to help in a down market), the fund is the worst performing one from the cohort analyzed. We are looking here at Invesco Senior Income Trust (VVR) and Apollo Tactical Income Fund (AIF) as comparison points.

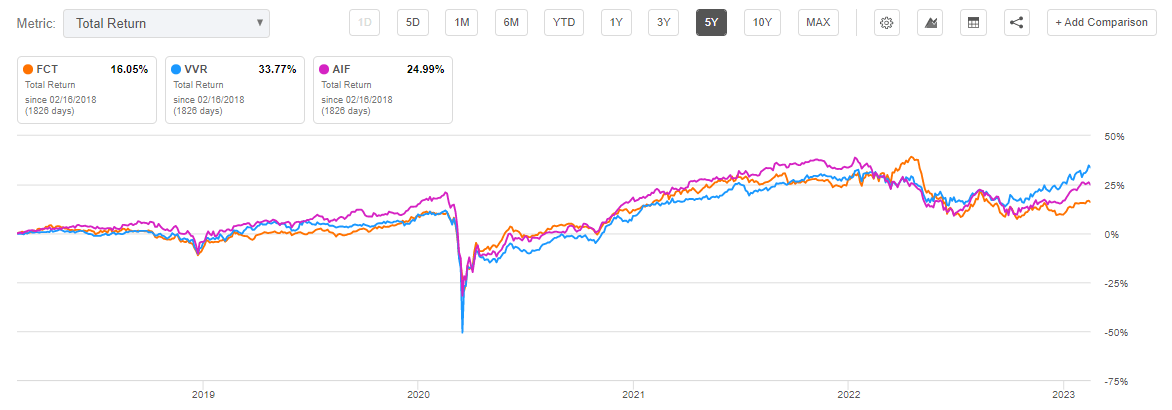

On a 5-year time-frame FCT continues to be the laggard in the cohort:

Total Return (Seeking Alpha)

Longer time-frames give us a better sense regarding management’s ability to pick good credits and generate alpha. FCT lags, although its risk metrics are not low.

Discount/Premium to NAV

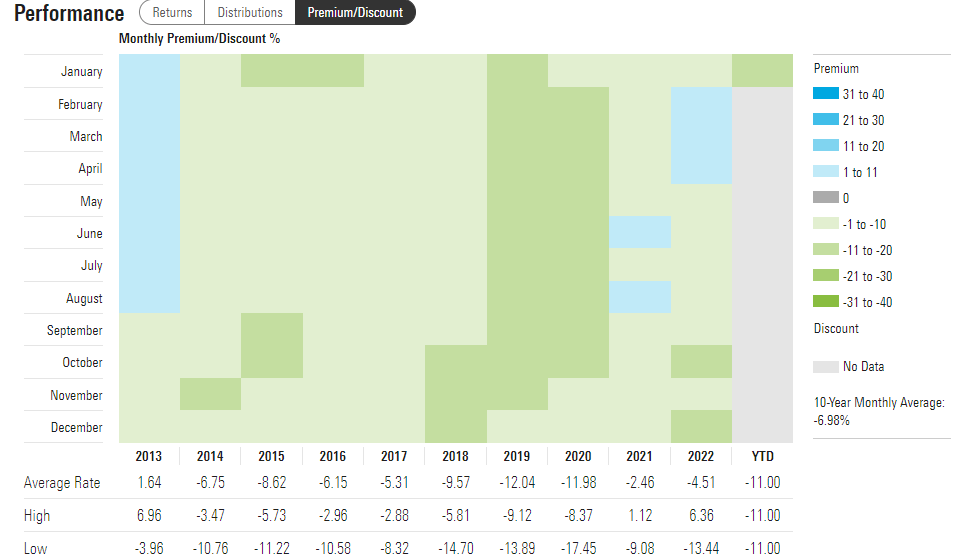

The fund usually trades at a discount to NAV:

Premium/Discount to NAV (Morningstar)

We can see from the above table, courtesy of Morningstar, that the CEF usually trades at a 10% discount to net asset value.

Conclusion

FCT is a leveraged loan CEF. The fund has a normalized build, without taking excessive risk via its holdings credit profile, although it does take some issuer concentration risk via its top holdings. What is particular about this CEF is its current low leverage ratio of only 11%, which is suitable for the current cyclical bear market. Long term however, the fund needs to bump that up to 30% to 35% in order to generate the same results as its competitors. With a -10% discount to NAV the fund represents an attractive choice for the current environment, although longer term the vehicle underperforms the golden standards in the space, namely VVR and AIF.

Be the first to comment