David Commins

Nauticus Robotics, Inc. (NASDAQ:KITT) will likely benefit from the incoming demand for rare earth materials and the development of new forms of extraction and generation of energy. I believe that the company’s AI-based perception applied to its robots could bring significant free cash flow generation. I obviously see risks from lack of diversification and perhaps failed commercial strategy; however, the stock appears a bit undervalued.

Nauticus Robotics

Nauticus Robotics focuses on the development of technologies for operations that are carried out in the marine environment.

Source: Company’s Website

It is evident that the forms of extraction and generation of energy are changing radically, and this transformation tends to deepen rather than appear to slow down in the future. For example, the situation has sharply worsened during the year 2022 with regard to the conditions related to the provision of gas supplies due to the complications and sanctions arising from diplomatic relations due to the war between Russia and Ukraine, which logically has deeper interests. In this sense, in my view, companies like Nauticus Robotics are presented as an emerging option in terms of the standardization and adaptation of technologies towards the future in the fields, in which innovation in robotics and marine technology can collaborate.

Nauticus Robotics’ business model is not divided into segments, but operations are concentrated in the same business branch, through which it offers its products, which include robotics elements that serve for underwater exploration and research as well as maneuvering in coastal operations.

The company also offers a cargo transportation service with a zero carbon emission, perfectly adapting to the requirements and trends in terms of environmental regulation. Let’s also mention that Nauticus Robotics’ products are guided by software also developed by the company, permanently trained through machine learning and with an operation based on artificial intelligence.

Although the company does not have more information about its active operations or its employee base, management does clarify that the majority of its employees are engineers with a past at NASA. Of course, the conditions of this type of employees, even though they are great scientists and developers, does not guarantee, under any point of view, success in future commercial operations or the strategy to determine the destination of its investments for development of products.

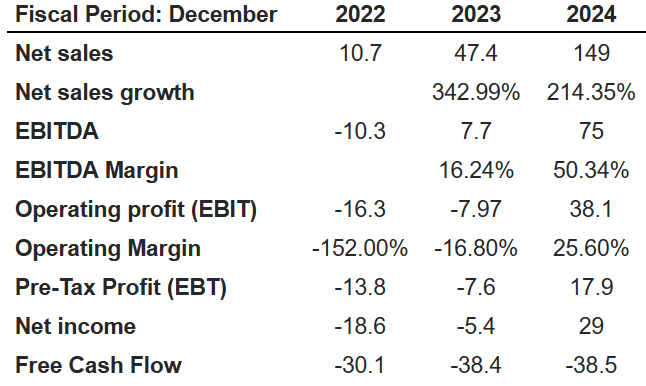

Analysts Expect Triple-Digit Sales Growth In 2023 And 2024

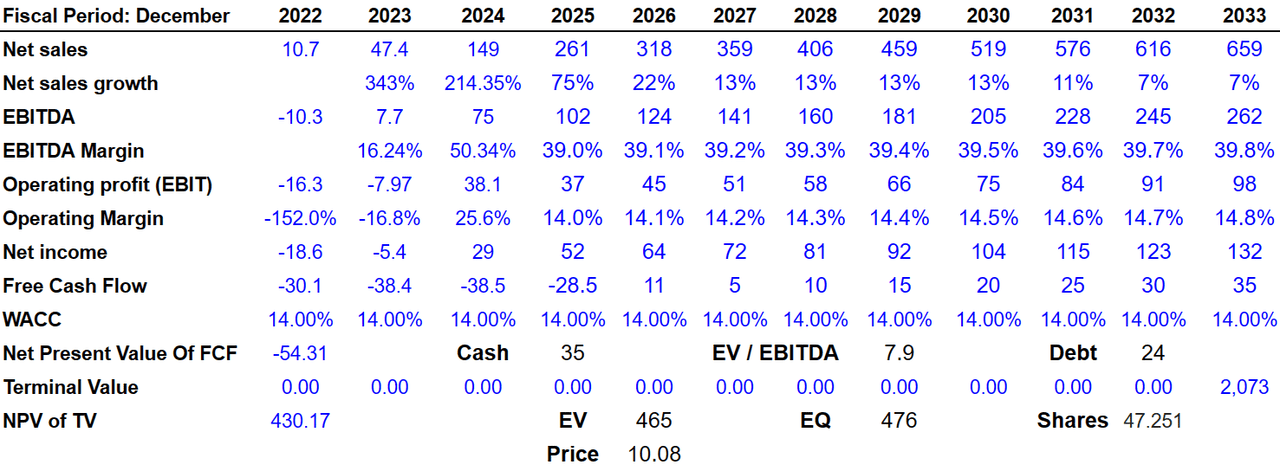

Analysts are expecting impressive sales growth from Nauticus Robotics. They are expecting 2024 net sales of $149 million with net sales growth of 214.35%. 2023 sales growth is expected to be close to 342%. In addition to 2024 EBITDA of $75 million and 2024 EBITDA margin of 50.34%, the operating profit would be $38.1 million with an operating margin of 25.60%. Besides, analysts are also anticipating a pre-tax profit of $17.9 million and 2024 free cash flow of -$38.5 million. I used some figures from the expectations of other analysts.

Source: marketscreener.com

Balance Sheet

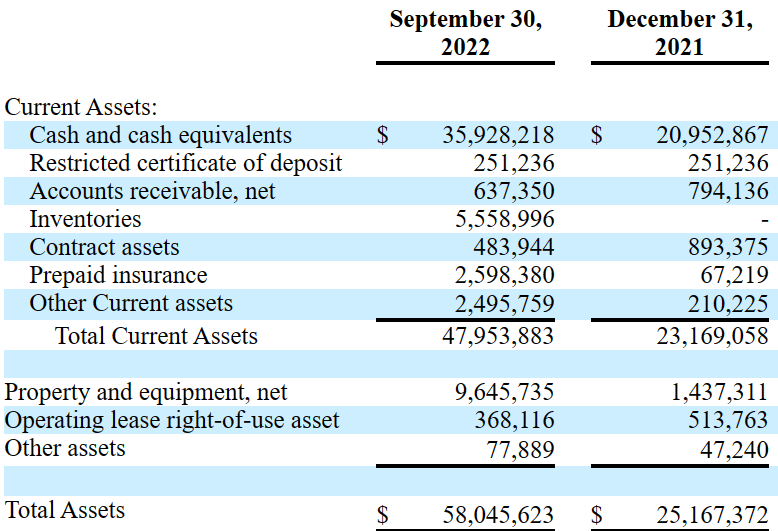

As of September 30, 2022, the financials included cash worth $35 million, inventories of $5 million, and prepaid insurance of $2.5 million. With other current assets of $2.4 million, total current assets stand at close to $47 million, more than 10x the total amount of current assets. I believe that Nauticus Robotics will likely not have liquidity issues.

Besides, with property and equipment of $9.6 million, total assets stand at close to $58 million, implying an asset/liability ratio close to 2x. In sum, I believe that the balance sheet is in good shape.

Source: 10-Q

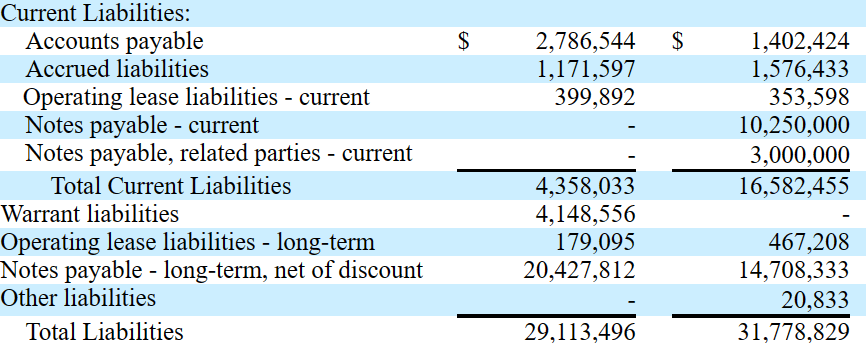

Regarding the liabilities, the company disclosed accounts payable worth $2.7 million, accompanied by accrued liabilities of $1.1 million and total current liabilities of $4.3 million. Besides, warrant liabilities stand at $4 million, with notes payable worth $20 million and total liabilities worth $29 million.

Source: 10-Q

A Large Target Market And AI-based Perception And Control Software Would Imply A Valuation Of $10.08 Per Share

Among the most relevant data coming from Nauticus Robotics, I would highlight that the ocean economy appears to be worth around $2.5 trillion. With this in mind, in my view, Nauticus Robotics appears in a good position to report million-dollar revenue. Under this case scenario, I assumed that the size of the market will likely enhance the future free cash flow generation.

We can also highlight that the demand for rare earth materials, by the year 2030, may increase to around 350k tons. Considering that minerals are the product of marine research and extraction, Nauticus Robotics could also benefit significantly from the growing extraction of these types of material from the ocean. Under this case, I assumed that demand for rare materials will likely serve as a catalyst for revenue generation.

Source: Company’s Website

I also believe that the company’s AI-based perception and control software along with high-definition sensors will likely reduce costs, which may bring the FCF margin north. In this regard, let’s mention the explanation given by management in a recent quarterly report.

Our key technologies are autonomous platforms, acoustic communications networks, electric manipulators, AI-based perception and control software, and high-definition workspace sensors. Implementation of these technologies enables operations to reduced costs over conventional methods. Source: 10-Q

Finally, I would expect continued revenue acceleration thanks to new contracts signed by Nauticus Robotics. In this regard, I believe that the agreement signed with Triumph Subsea Construction Limited to sell Aquanaut systems will likely be a catalyst for revenue growth in 2023 and 2024.

On August 29, 2022, we amended an existing sales contract with Triumph Subsea Construction Limited, which provides for the sale of four Aquanaut systems for a total of $54.2 million. The amended terms shifted the customer’s milestone payments into late 2022 and through 2024, while also shifting the delivery of the initial two Aquanaut systems to late 2023, with the subsequent units being delivered in late 2024. Source: 10-Q

Under the previous conditions, I assumed that Nauticus Robotics would deliver 2033 net sales of $659 million with a net sales growth of 7%. In addition to 2033 EBITDA of $262 million and an EBITDA margin of 39.8%, I expect an operating profit of $98 million and an operating margin of 14.8%. Besides, we will have a net income of $132 million and 2033 free cash flow of $35 million.

Source: Bersit Research

If we assume a WACC of 14%, the net present value of future free cash flow would stand at around -$54.31 million. If I assume an EV/EBITDA multiple of 7.9x, the terminal value would be $2.073 billion, and the NPV of TV would be $430.17 million. Finally, the enterprise value would be $465 million, the equity valuation would stand at $476 million, and the fair price would be around $10.08 per share.

Lack Of Diversification Or Failed Commercial Activity Could Bring The Stock Price Down To $2.5 Per Share

Nauticus Robotics does not carry out any operations. It is also not involved in the business realities of corporations that actually have active operations in the ocean and coasts. Therefore, management may lack practical knowledge in this regard. In the same way, the products of the company are particular and highly developed, but the company lacks diversification if one thinks about the number of offers available. In my view, lack of diversification could contribute to higher revenue volatility.

In the same way, an inability to propose new strategies as well as an inability to provide support channels and customer service for its contractors can be an adverse blow to the company’s operations, since being modern products they need a process of training and accompaniment for the technical employees. Clearly, the company may lack sufficient expertise to grow.

Finally, if we talk about the risks to which Nauticus is exposed, we can ultimately point out the direct dependence on the migration of the market to technological implementations and the automation of different phases of the production process. Basically, the predictions for 2030 and 2050 are based on real factors and are highly promising for Nauticus. The fact that commercial and financial success depends directly on the fulfillment of these predictions is obviously a condition of long-term risk.

Any drastic change or insertion of lower cost technologies as well as a negative development or recession in the marine industry in general, added to the possibility of regional regulations in relation to the exploration of marine resources, would cause a large-scale alteration in the company projections, and without a strategy that contemplates this possibility, Nauticus would effectively be left without room for action or adaptation to correct the course of its operations.

The development of technologies for the extraction of marine materials as well as research and construction of off-shore infrastructure, whether for the installation of wind mills or other types of industrial establishments, is not a novelty either nationally or internationally. If clients believe that the products offered by Nauticus Robotics are not necessary, revenue growth would be lower than expected.

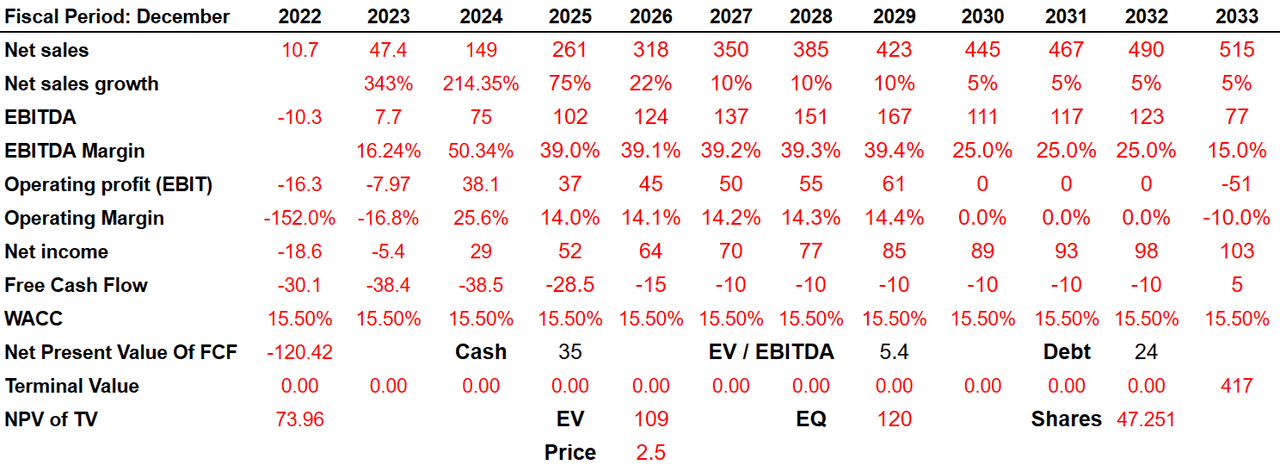

Under my bearish case scenario, I included 2033 net sales of $515 million together with a net sales growth of 5%. In addition to an EBITDA close to $77 million accompanied by an EBITDA margin of 15%, the operating profit would be close to -$51 million with an operating margin of -10%. Finally, I also assumed a net income of $103 million with a free cash flow of $5 million.

Source: Bersit Research

If we include a WACC of 15.50% and an EV/EBITDA multiple of 5x, the terminal value would stand at $417 million with a NPV of TV of $73.96 million. Finally, the enterprise value would be $109 million, with an equity valuation of $120 million and a fair price of $2.5 per share.

Conclusion

Nauticus Robotics expects to benefit from the probable incoming demand for rare earth materials. Besides, management has already signed agreements like that with Triumph Subsea Construction Limited, which may accelerate revenue growth in 2023 and 2024. In my view, if the AI-based perception and control software successfully accelerates free cash flow generation, Nauticus Robotics could be worth close to $10.08. I obviously see risks from lack of diversification and potential failed commercial activity. With that, the company’s stock price appears undervalued.

Be the first to comment