Spencer Platt

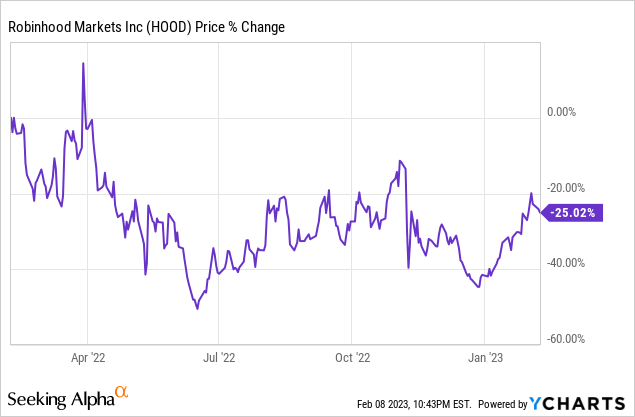

Animal spirits describe the emotions and instincts that influence financial decision-making in uncertain environments. For the stock market, the last few years since the pandemic has been defined by hyper volatility as the stock market quickly ebbed and flowed between boom and bust. Menlo Park, California-based Robinhood (NASDAQ:HOOD) has in many ways come to represent the full zeitgeist of the last few years since the pandemic. The commission-free stock broker, which also offers crypto investing, is now up nearly 30% year-to-date as the market finally sees the end of the current Fed rate hike cycle. Perhaps there will be two further 25 basis point hikes, but the dovish pivot looks to be here and inflation is now pulling more towards the Fed’s 2% target.

Hence, assets from tech stocks to Bitcoin to the ape-powered meme stocks have seen trading get reinvigorated. The last few weeks have seen bullish animal spirits, locked away in a more than year-long decline, return triumphantly. Bitcoin is up 35% since the start of January, the tech-heavy Nasdaq 100 is up 15% and the S&P 500 is up nearly 8%. This has created the early backdrop for Robinhood’s operational performance in 2023 as positive market volatility drives trading activity and the overall momentum of its platform. It also comes on the back of its fiscal 2022 fourth quarter results.

Robinhood’s Fiscal 2022 Fourth Quarter Earnings Depict 2022 Headwinds

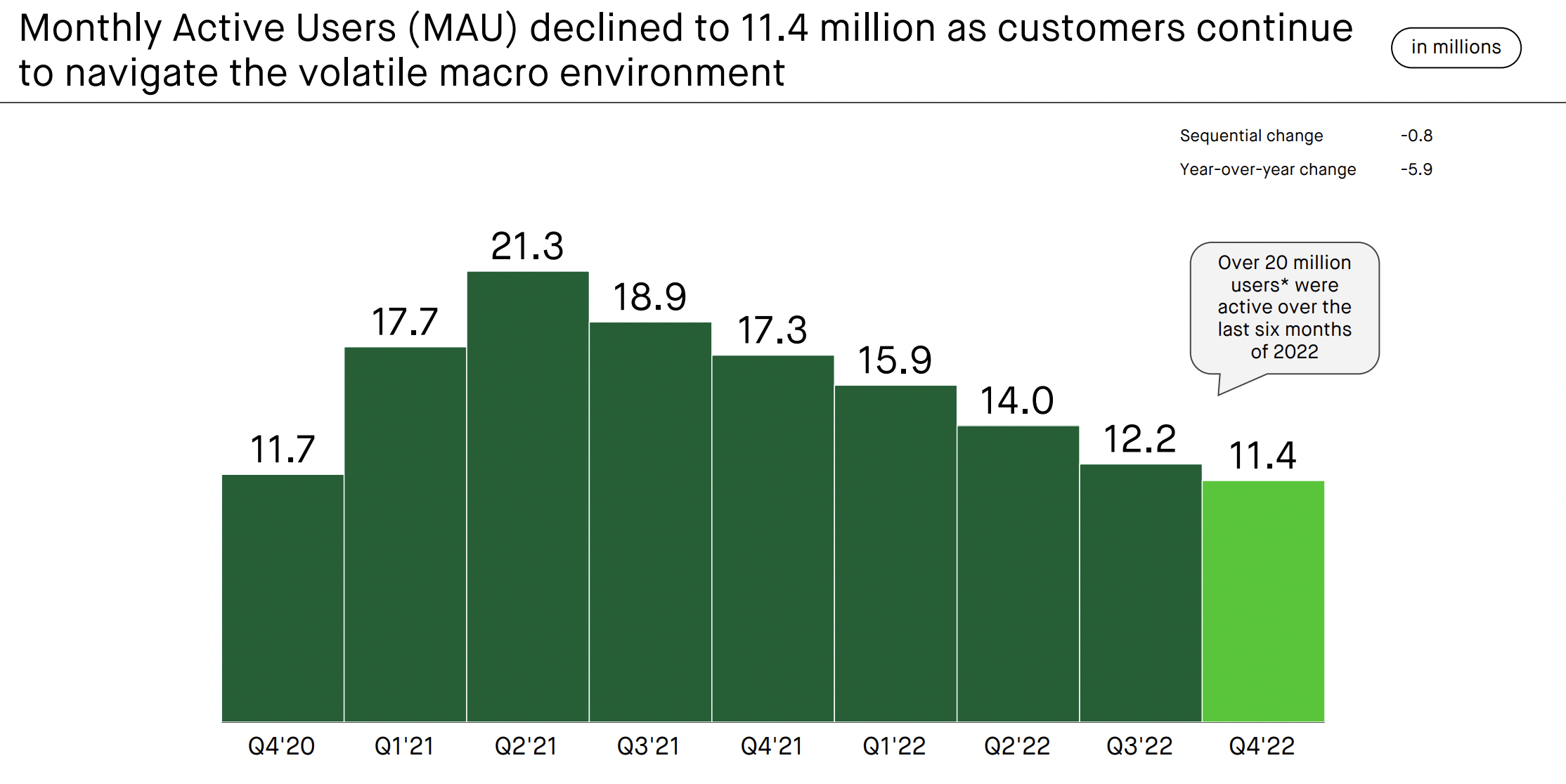

Robinhood recently reported earnings for its fiscal 2022 fourth quarter. The company reported revenue of $380 million, a growth of 5% over the year-ago quarter but a miss of $15.16 million on consensus estimates. Robinhood faced a number of blocks to growth. Firstly, monthly active users fell to 11.4 million, a sequential decline of around 800,000 users. This came as assets under custody fell sequentially by 4% to $62 billion with the market valuation for crypto and growth-oriented stocks facing pressure during the fourth quarter.

Both these metrics highlight the importance of animal spirits to Robinhood’s underlying momentum. An uptrend not only helps boost MAU it also drives AUC to strengthen whilst increasing the overall health of the platform. Critically, this forms the base for alpha. Robinhood is really a play on the gyrations of the stock market and an investment in its commons cannot be made without assessing the general direction of the factors driving the near-term direction of the stock market.

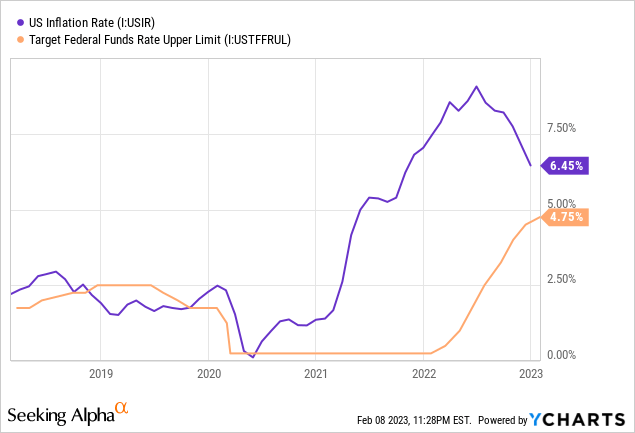

Inflation, rising Fed fund rates and the specter of a recession have all worked to form the three horsemen of the market. However, inflation has been on a marked decline from its peak of 9.1% in the summer of 2022. This is with revised 2023 economic forecasts for the US now placing the economy on track for 1.4% GDP growth. Hence, a soft landing now appears fully in view with interest rates unlikely to rise significantly from their current level.

Robinhood

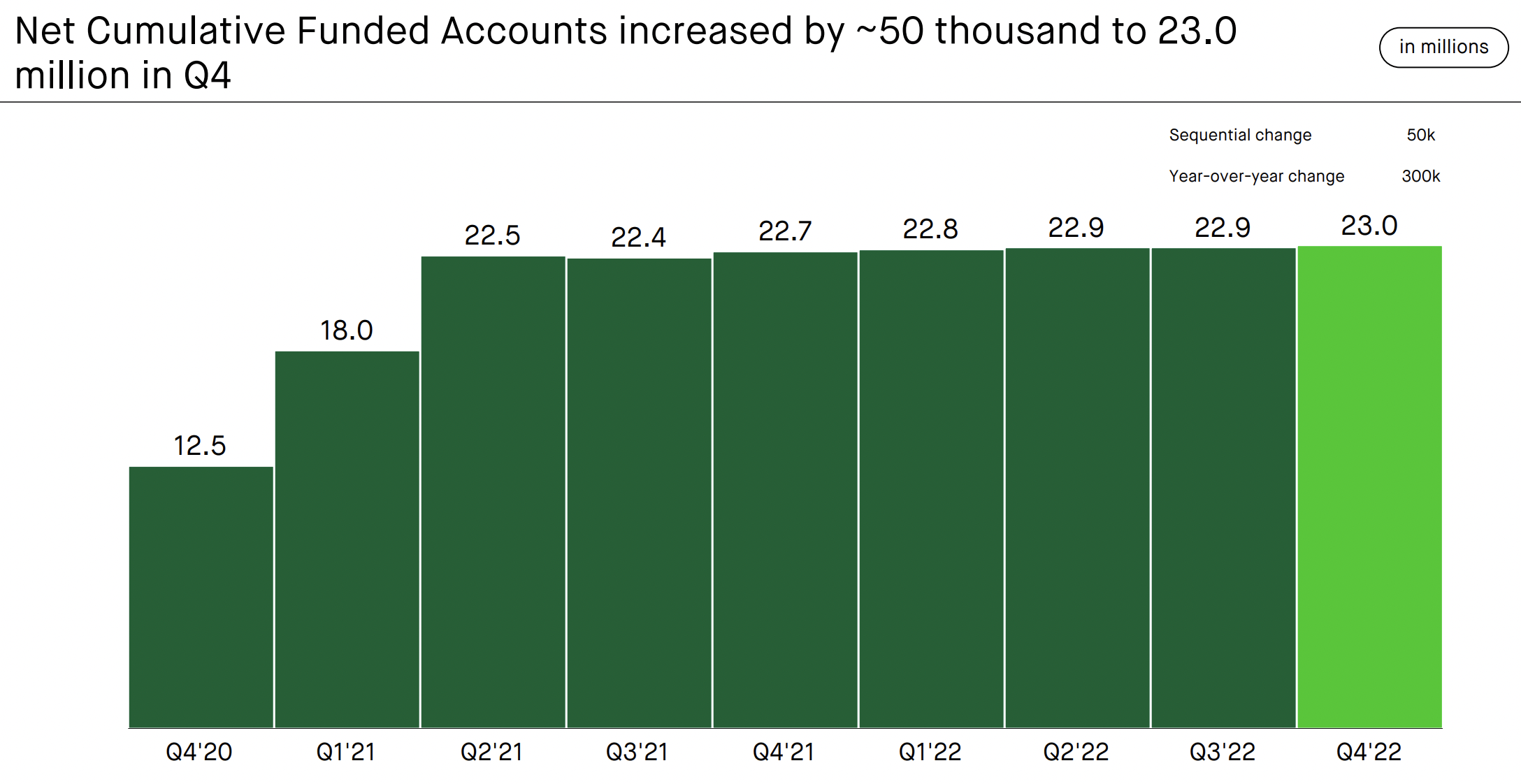

Robinhood’s net cumulative funded accounts saw marginal growth of around 50,000 to 23 million with net deposits also growing to reach $4.8 billion. This was a growth of around 30% relative to the third quarter AUC as 2022 net deposits grew by 19% over 2021. Average revenue per user came in at $66, a $3 increase from the third quarter.

Inflation, Rising Interest Rates And Recession Fears

Robinhood recorded a net loss of $166 million, an improvement from a net loss of $423 million in the year-ago quarter and from a net loss of $175 million in the prior third quarter. This meant an EPS of around -$0.19, underperforming consensus estimates by around 7 cents. Management added more detail around this during their earnings call.

The company had to record a $57 million loss during the quarter from a single error processing shares in Cosmos Health (COSM), a micro-cap healthcare company. Essentially, Robinhood accidentally sold the stock short and was forced to buy it back when its commons surged higher. Whilst the mistake was corrected quickly, Robinhood lost more than the market cap of Cosmos which worked out to be $0.07 per share to drive the miss.

Overall, transactional revenues fell to $186 million, an 11% sequential decline on the back of cryptocurrency revenue that fell markedly by around 24% to $39 million and options trading that flatlined at $124 million.

Robinhood

However, the clear structural decline of monthly active users is the core takeaway from the earnings report. Indeed, Robinhood has built its image of the democratization of finance. Its inherent core corporate value is finance that is built for everyone, yet its retail base has been nearly cut in half from its 2021 peak and shows no sign of stopping its fall. The return of animal spirits holds the potential to reverse this decline if it stays. In my opinion, this forms the foundation for considering a long position. I remain neutral on the stock.

Be the first to comment