ionutanisca/iStock via Getty Images

There could be a lot of wild trading in San Juan Basin Royalty Trust (NYSE:SJT) over the next few weeks as monthly dividends are announced based on extremely high natural gas prices late last year and early this year, but there are recent estimates of much lower natural gas prices in the future that could have a negative impact on SJT units. Too many traders are also just looking at the Henry Hub spot prices and are ignoring the fact that SJT is mostly impacted by west coast natural gas supply/demand – not Louisiana nor the east coast. This article is an update to my prior SJT articles.

Monthly Dividend and Yield Confusion

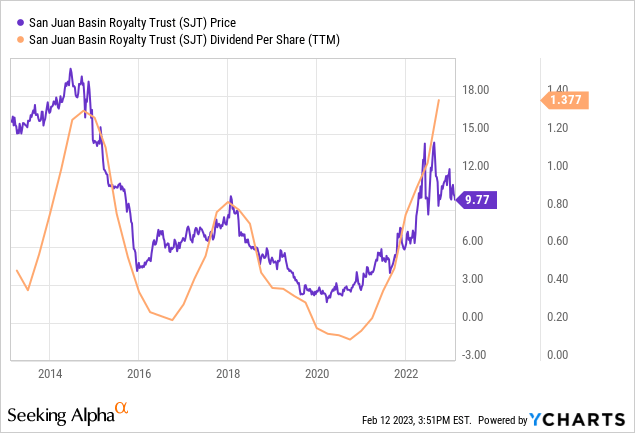

I expect that some investors see the SJT yield of 17.13% on Seeking Alpha’s webpage and think the royalty trust is a great buy. One of the problems is that that yield figure is based on the trailing last twelve months and not on the expected future monthly dividend payments for later this year. A monthly dividend of $0.0963 is being paid on February 14, which was declared on January 20 based on November’s natural gas price/production numbers.

This monthly payment yield misunderstanding is about to get much worse after the February distribution announcement and especially after the March announcement. Given that the Inside FERC’s EPNG San Juan Basin price for January was $32.97 because very cold weather had depleted storage in the West, it is possible that the monthly dividend announced in mid-March could be well over $0.65 per unit. I can see some retail trader multiplying $0.65 by 12 to incorrectly estimate a $7.80 total annual dividend and assert that SJT is “yielding almost 80%”. The trailing twelve-month dividend total could, in my opinion, be at least $2.37 after the March dividend is included, which would imply a 24% yield based the latest SJT price.

SJT Price and Trailing 12 Month Dividends

Natural Gas Prices and SJT Unit Prices

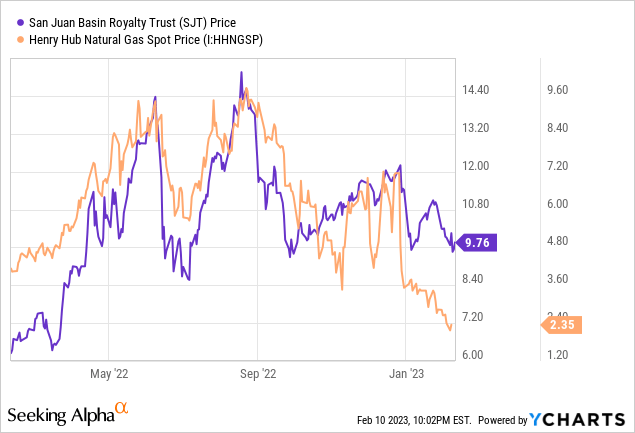

Historically there has been some correlation between Henry Hub natural gas prices and SJT unit price. The chart below compares the Henry Hub spot price and SJT unit price. Using the Henry Hub price, however, may not always really be indicative of what price SJT is actually being paid because their natural gas is not sold/priced based on that hub. It is based on the San Juan Basin price. The chart is still useful in that it does show some general connection between the two, which is expected because SJT is purely a royalty trust and does not have any actual operations that could influence the price.

SJT Price and Henry Hub Natural Gas Price

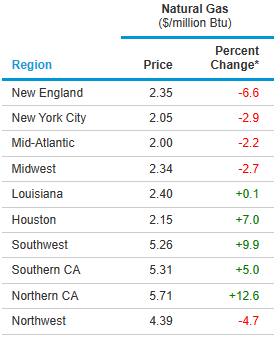

If you looked just at the above chart, one could assert SJT is currently greatly over-priced. Investors, however, are looking at the natural gas prices in markets served by SJT. Look at the table below to see the very high variance in current spot natural gas prices for the various markets and compared to the Henry Hub $2.35 price.

Spot Price for Delivery 2/10/23

www.eia.gov/todayinenergy/prices.php

California High Natural Gas Prices

Gov. Newsom on February 6 sent a letter to the chairman of FERC (text of the letter) requesting an inquiry into high natural gas prices in California. He asked “that FERC immediately focus its investigatory resources on assessing whether market manipulation, anticompetitive behavior, or other anomalous activities are driving these ongoing elevated prices in the western gas markets”. While he may want to force the prices down with some threat of an investigation, his actual actions are keeping natural gas prices higher. The state is paying consumers $90-$120 California Climate Credits on their natural gas and electric bills. So instead of higher natural gas prices reducing demand, the state is helping consumers pay these higher natural gas prices, which helps to keep demand higher.

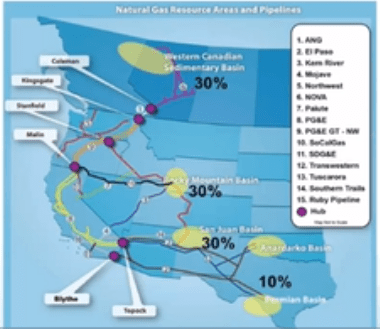

The California Public Utilities Commission – CPUC- held an en banc hearing on the natural gas price issues in the state on February 7 (recording of the 4-hour hearing). Besides blaming the cold weather, many blamed pipeline issues, such as unexpected pipeline maintenance and repairs caused by prior pipeline explosions that disrupted the flow of natural gas into California. It seems that many of the pipeline problems are finally being resolved, which should increase the flow of natural gas to California and other areas of the West. This is expected to greatly reduce prices in the area. It does not appear that any of these pipeline problems directly impacted the flow of natural gas from the San Juan Basin area. California currently gets about 30% of their natural gas from the San Juan Basin. SJT investors need to follow any new developments in California.

Percent of Natural Gas Gets From Various Areas

www.adminmonitor.com/ca/cpuc/en_banc/20230207/

Natural Gas Price Forecast

Last week the U.S. Energy Information Administration announced a new 2023 average Henry Hub natural gas spot price forecast of $3.40 MMBtu, which is down 30.5% from their $4.90 forecast in January. This compares to an average of $6.42 in 2022. They also sharply lowered their 2024 forecast to $4.04 from $4.80. These numbers were lowered because unusually warm weather in certain parts of the country resulted in much less natural gas usage.

While these forecast numbers are only for the Henry Hub, the direction of various hub prices are often fairly much the same. With pipelines serving western markets becoming fully operational and warmer weather in California, the prices received by SJT could be significantly lower over the next few months. This means that monthly dividends should drop sharply from the March amount by mid-year.

Issues With HilCorp

One of the problems an investor has owning a royalty trust is that you are at the mercy of the actual operator. Hilcorp bought the San Juan Basin assets in 2017 and there have been a few problems over the years with some of their calculations/figures. Audits should pick up any problems, but many investors still worry that “things may not always be right”. All drilling and other decisions regarding selling contracts are all done by Hilcorp. STJ unitholders have no say, except if 75% vote in favor of selling the royalty trust itself.

Hilcorp is a huge organization that is privately owned. After reading many local newspaper articles about Hilcorp it seems there are other problems such as they run everything out of their headquarters in Houston and don’t seem directly involved in the communities where they have their operations. Often energy companies at least try some PR outreach programs to reduce the public’s negative opinions of “big oil”, but not Hilcorp. With no real positive image PR campaign, Hilcorp may run into problems with environmentalists who want to close fossil fuel operations. An area that Hilcorp and SJT are vulnerable, in my opinion, is that 17% of their reserves are coal seam natural gas according to the SJT 10-K. Some assert that production of coal seam natural gas is a major cause of methane pollution.

Tax Issues Readers Have Asked About

A number of readers have asked about buying/owning SJT units in an IRA. Investors should consult with their tax professional on this issue, but the trust does have extensive tax information on their website. As stated in their latest tax information booklet, “In most cases, payments from Units held in an IRA are tax-deferred, and no tax reporting is required. However, Unit holders should consult their tax advisers regarding their particular circumstances.” Owning SJT in an IRA makes filing your taxes much easier, in my opinion. Investors often worry about unrelated taxable business income – UTBI – in an IRA, but according to their tax booklet, “income of the Trust should not be unrelated business taxable income to such organizations, so long as the Trust Units are not “debt-financed property” within the meaning of IRC Section 514(b).”

Remember the dividends from this grantor trust are not considered qualified dividends. They are considered “ordinary income, taxed at your marginal rate”. You should get a 1099-MISC and 1099-INT. Another issue is the confusion over the time period used for filing tax returns. As stated in their tax booklet, “the income to be reported for 2022 is associated with amounts distributed in February 2022 through January 2023.”

Usually, S.A. editors prefer that writers avoid income tax issues, but it seems many of the comments by readers on SJT articles are questions about taxes. (Disclosure: I am not giving tax advice and Seeking Alpha is not a tax advisory website. Readers should consult their own tax professional regarding their specific tax issues. The above statements are mostly quotes directly from the SJT website, but there is no assurance the statements are accurate or comply with the U.S. Tax Code and I.R.S regulations.)

Conclusion

Since I first wrote about San Juan Basin Royalty Trust in April 2016, SJT investors received a 179% total return. I bought some SJT units last week because I think there could be some irrational trading as a result of the March dividend announcement, which I plan to sell into.

I think natural gas prices in the West will eventually become more aligned to the Henry Hub prices when the prior pipeline issues are completely resolved. After some very high SJT monthly dividends, they should decline sharply by mid-year. Overall, I rate SJT units neutral/hold.

Be the first to comment