tumsasedgars/iStock via Getty Images

Thesis

Eaton Vance Tax-Managed Buy-Write Strategy Fund (EXD) is an equity buy-write fund. The vehicle was due for a vote last week for its proposed merger with Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV):

The proposed merger is subject to approval by Acquired Fund shareholders at a Special Meeting of Shareholders scheduled for Thursday, February 2, 2023. A proxy statement/prospectus containing information about the meeting and the proposed merger will be mailed to the Acquired Fund’s shareholders of record as of November 21, 2022. No action is needed by shareholders of the Acquiring Fund. Each Fund is a diversified closed-end management investment company sponsored and managed by Eaton Vance Management. Each Fund is listed on the New York Stock Exchange.

We had expected the meeting and the vote to go through, and have some sort of result on the proposed merger. Unfortunately, it was not that way:

BOSTON–Eaton Vance Tax-Managed Buy-Write Strategy Fund (NYSE: EXD) (the “Fund”) held a special meeting of shareholders earlier today (the “Special Meeting”). At the Special Meeting, Fund shareholders were asked to approve an Agreement and Plan of Reorganization pursuant to which the Fund will be reorganized with and into Eaton Vance Tax-Managed Buy-Write Opportunities Fund (NYSE: ETV), as approved by the Fund’s Board of Trustees. The Special Meeting was adjourned to March 16, 2023 at 1:00 p.m. Eastern time to allow more time for shareholders to vote. The November 21, 2022 record date for shareholders entitled to vote at the adjourned Special Meeting remains unchanged. Information about the adjourned Special Meeting appears below.

Source: Business Wire

It seems that the trustees could not get a simple majority needed given lack of participation, hence the vote was postponed. This is a bit of a surprise given that both funds come from Eaton Vance, and the fund management should have a good understanding of the shareholders in the fund and prospective appetite for what had been put forward. Looks like Eaton dropped the ball a bit on this one.

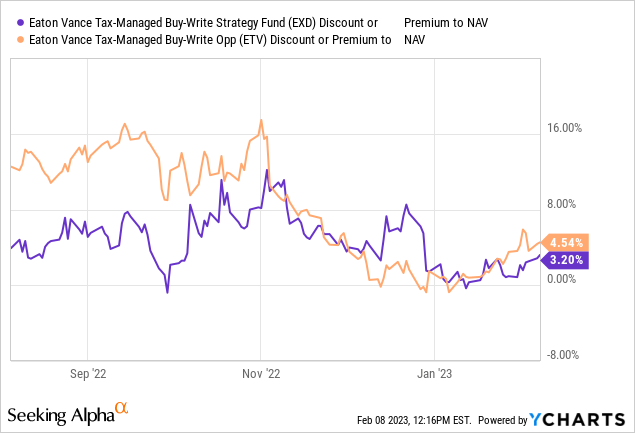

Since the initial merger news came out, EXD and ETV have started to trade at very similar premiums to NAV, which currently stand at 3.2% and 4.5% respectively. The market is basically telling us the merger will eventually go through. EXD holders have seen a nice pick-up in pricing as the market firmed up the premium post the merger announcement, and we even saw a shocking development in late December where the premium to net asset value for EXD exceeded the one for ETV by almost 8%! That is unprecedented, and EXD should have been sold vs ETV at that point.

We feel Eaton dropped the ball a bit on this merger proposal by not careening enough support from shareholders prior to the vote day, but they will eventually manage to push it through. Until the final approval, substantial divergences in premiums to NAVs for the two CEFs should be actively traded, betting on a mean reversion and approval of the merger.

Premium / Discount to NAV

We can see a nice correlation between the premiums to NAV for the two CEFs since the merger announcement:

After the proposed merger was announced, we saw a substantial jump in the premium to NAV for EXD. Currently, the two funds are trading at very similar premiums, which tells us the market thinks the merger will eventually go through.

Conclusion

EXD is set to be merged into ETV. Unfortunately, Eaton dropped the ball on the scheduled meeting and securing the necessary votes, with the special meeting now postponed to March. We feel the merger will eventually go through, and the market is telling us a similar story, with the two CEFs having very similar premiums to NAV. However, given the volatility present in the wider markets, arbitrage opportunities can arise in these two names. Back in December, we saw EXD move to an unprecedented 8% premium over ETV, an event which should have been sold into (i.e., an investor should have sold EXD and bought ETV). We believe the merger will eventually go through, and any volatility driven dislocation in the premium differential here can be traded by an active retail investor. This relationship should be closely watched and monitored for arbitrage opportunities.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Be the first to comment