Hammad Khan

Emerging market stocks often bottom out amid wide-scale public discontent and protests, as the market already prices in a further escalation, allowing stocks to rally even if the economic and political situation remains dire but does not deteriorate. In the case of Brazil, the January 8 capital riots highlighted the extent of the discontent among swathes of the Brazilian population, and the failure of the market to move lower suggests the bad news had all been priced in. In fact, a number of positives can be taken from the response to the protests, which could be seen as a sign of strength of Brazil’s institutions.

While President Lula’s economic policies will act as a headwind to corporate profitability, markets are already anticipating a collapse in earnings and dividends and remain cheap on a forward basis. I remain long the iShares MSCI Brazil Capped ETF (NYSEARCA:EWZ), a position I have held since February 2021. Over this period, the high dividend yield has allowed the EWZ to eke out a 1% total return gain, outperform the emerging market benchmark by more than 20%. This outperformance may have only just begun.

The EWZ ETF

The EWZ tracks the performance of the MSCI Brazil index and charges an expense fee of 0.57%. The ETF holds 50 companies at present and is heavily weighted towards commodities. The Materials sector accounts for 22% of the index, thanks to iron ore giant Vale, which has a 20% share. The Oil & Gas sector accounts for an additional 15% due to oil major Petrobras. The ETF’s performance is also driven by the performance of the currency, which is itself in part a function of commodity export prices. High commodity prices have seen earnings surge over recent years, leaving the EWZ trading at extremely undervalued levels, while offering a dividend yield of 11.9%. Shares outstanding in the ETF peaked in early 2020 and remain 28% down from this peak, while total assets under management have fallen by over a half over this period to USD5.0bn.

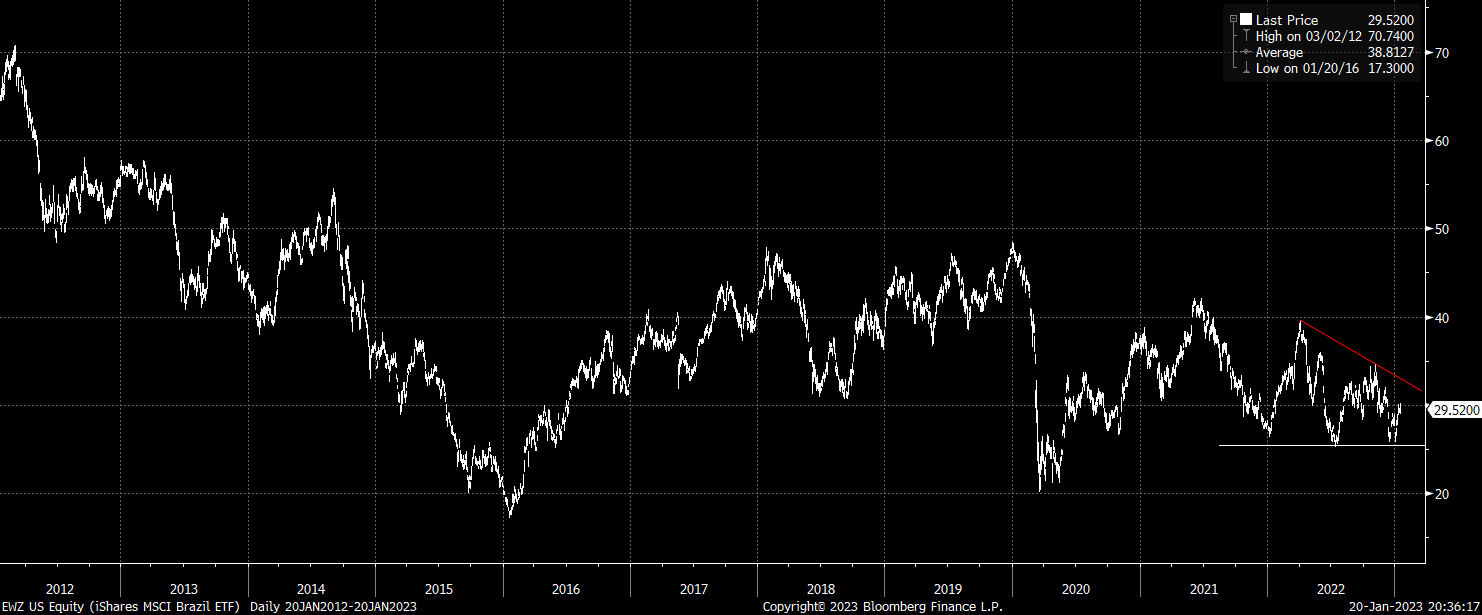

The Lows Have Held

Weakness seen in the EWZ in early January found strong support at the December lows, setting up a potential double bottom formation. The muted reaction to the Capitol riots highlights the extent to which sentiment towards the market is already at rock bottom. We would need to see a break above down trendline resistance, which comes in at around USD33 in order to confirm an upside reversal. However, the strong support just above the USD25 area is a positive sign, particularly as holders of this ETF do not need capital gains to generate strong returns given the high dividend yield.

EWZ Share Price (Bloomberg)

Protest Response Highlights Brazil’s Institutional Strength

While some had feared that the military may not defend Brazil’s democracy, the response from the security forces was congratulated both domestically and internationally. The swift response has reduced the risk of protests spreading to other areas of the country, as has muted condemnation from former president Bolsonaro. The risk is that a more emboldened Lula could mean a stronger push for a more leftist economic agenda, which has been a major drag on market sentiment. However, the narrow margin of Lula’s election victory and the scale of the protests highlights the still-strong resistance to increased socialism in the country.

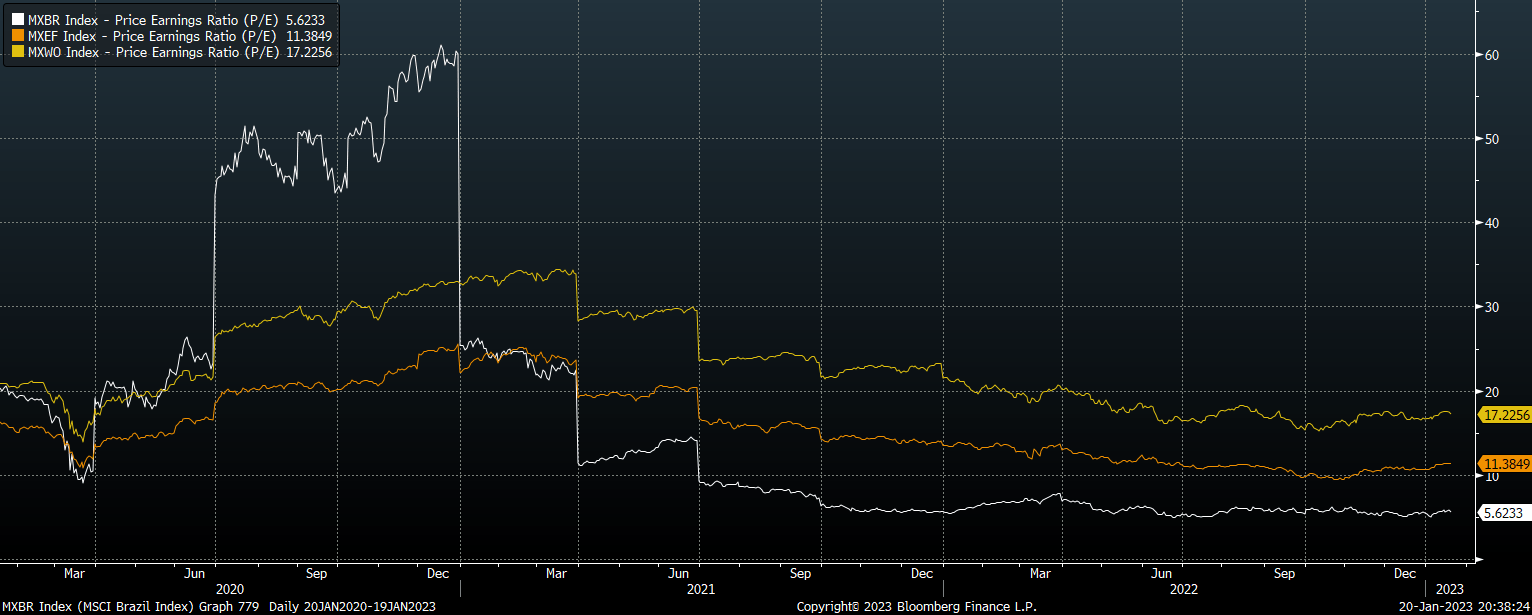

The Market Continues To Trade At Crisis Valuations

Even if Lula’s policies undermine wealth creation and corporate profitability in the country as investors clearly expect, the equity market is already anticipating a collapse in earnings and dividends. The trailing P/E ratio on the MSCI Brazil sits at just 5.6x, on par with the major market lows seen in 2001 and 2008. The P/E ratio is also less than half of that of the MSCI Emerging Markets index, and less than a third of the MSCI World. The dividend yield paints an even stronger picture of Brazil’s undervaluation, sitting at 9.7%, more than 3x the MSCI Emerging Markets index and more than 4x the MSCI World.

P/E Ratios For MSCI Brazil, MSCI EM, And MSCI World (Bloomberg)

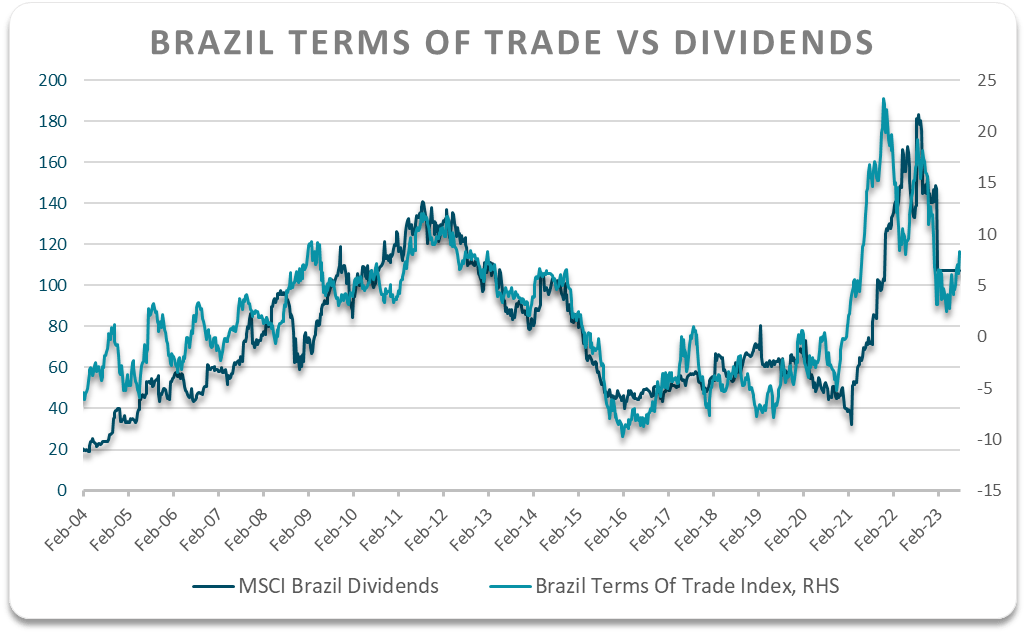

In order for Brazilian stocks to underperform over the coming years amid these valuations, we would need to see a collapse in earnings and dividend payments. Analysts are anticipating a sharp drop in both over the next 12 months, which puts the forward P/E ratio at 6.5x and the forward dividend yield at 7.1%. This would mark a 27% decline in dividend payouts, which is the scale of decline one would expect based on the country’s terms of trade index, as shown below. While this means that the yield on the EWZ will fall sharply from its current level of 11.7%, this is still attractive in a global context and relative to the EWZ’s own history.

Bloomberg, Citi, Author’s calculations

Summary

The bad news facing the Brazilian market appears to be priced in, with the Capitol protests failing to dent the recovery rally in the EWZ off the January lows. Even with earnings and dividend payments set to fall sharply over the next 12 months, the EWZ still trades at a deep discount, and offers a dividend yield far in excess of its peers.

Be the first to comment