Jean-Luc Ichard/iStock Editorial via Getty Images

Last week, Euronext (OTCPK:EUXTF) reported its financial results to the investor community. Before analyzing the three-month accounts, we would like to report the CEO’s words: “this second quarter of 2022 was marked by the continuation of the volatile environment seen since the first quarter of the year. Euronext’s business model again demonstrated its resilience, and generated solid growth in revenue, adjusted EBITDA and adjusted net income”.

Mare Evidence Lab’s buy case recap was very in line with the CEO’s comment. Indeed, we were forecasting:

- Higher market volatility due to economic uncertainty and macro headwinds, adjusting our revenue model based on the market volatility index to forecast future volumes

- Higher synergies deriving from the Borsa Italiana acquisition

- An increasing number of IPOs (especially in the Italian market)

- In a follow-up note, we also include an upside thanks to the new Euronext Tech Leaders ecosystem and its pre-IPO ancillary services.

Q2 Results

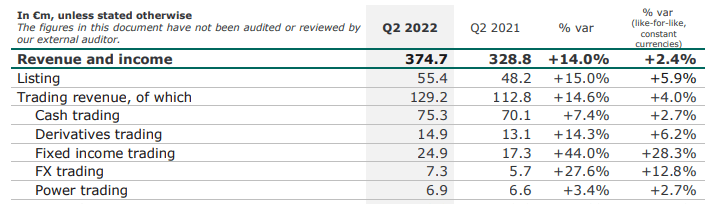

The company reached €374.7 million in turnover, up by 14% compared to the same period last year. The Italian stock exchange contributed more than a third to the performance delivering top-line sales of €129.2 million. Related to point 3) and despite a macroeconomic environment not very favorable for new IPOs, 19 new listings were completed in the quarter. Having looked at the Euronext sub-division, a strong performance was recorded in the trading both at fixed income and FX level that delivered higher revenue of 44% and 27.4% respectively (our point 1).

Euronext revenue

Source: Euronext Q2 press release

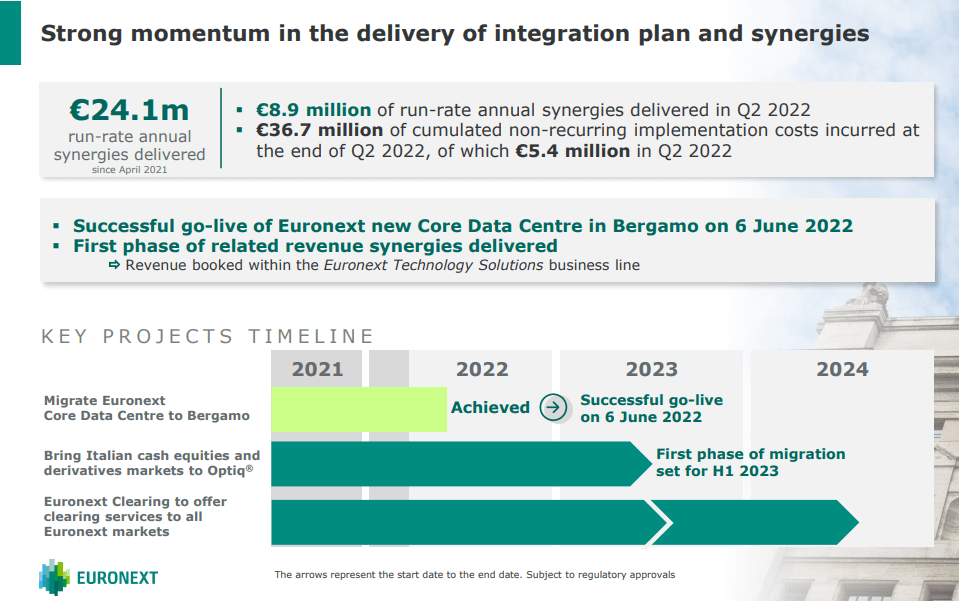

Going down to the P&L, adjusted EBITDA stood at €221.7 million marking a plus 12.3% versus the previous year’s end quarter. We should note that the EBITDA margin was 90 basis points lower mainly due to integration costs. However, adjusting the EBITDA and supported by our buy case recap point 2), synergies and integration plan are properly working and Euronext is delivering on its promises. Indeed, as expected, it has completed the state-of-the-art data center migration from the UK to Italy.

Euronext Synergies

Source: Euronext Q2 results

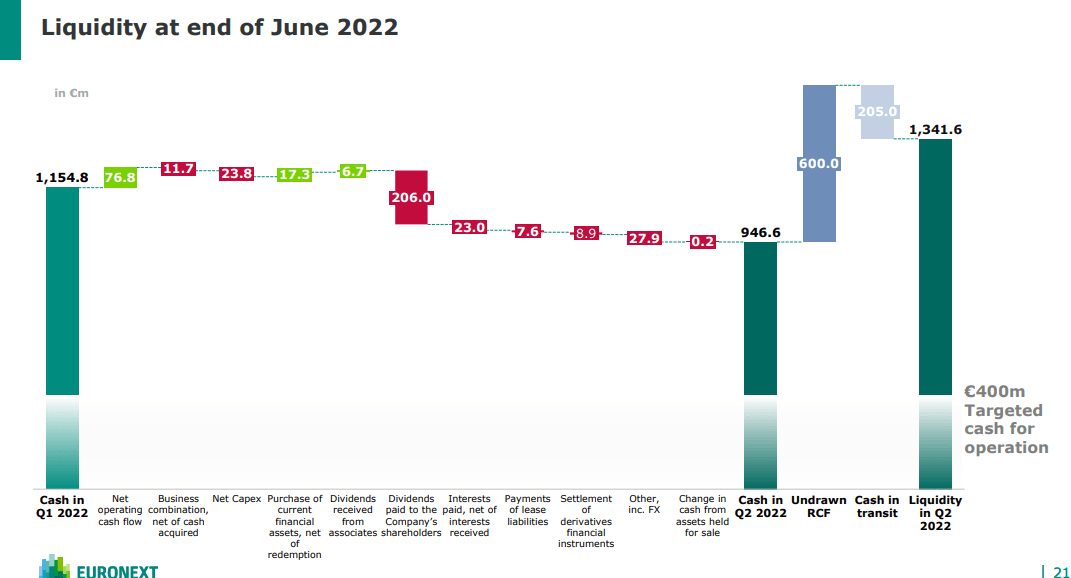

The net profit result was €118.9 million up 37.2% and +25.6% on a pro forma basis, with an adjusted net profit of €143.2 million again up by +6.4%. In Q2, we should also report that net debt increased, this was due to working capital requirements and also to the dividend payment (€206 million).

Dividend payment

Source: Euronext Q2 results

Conclusion and Valuation

Euronext delivered a solid set of numbers (after also strong Q1 performance). Synergies are starting to pay off and the company is very well managed. Concerning the valuation, we already adjusted our internal number in our previous publication arriving at a new stock price level from €98 to €100 per share. This was based on a forecast 2023 number with a 16x P/E and we decided to leave our number unchanged (we were already ahead of Wall Street analyst expectations). Since our strong buy rating, the anti-cyclical company is up by more than 6% and we continue to see a potential upside of more than 25% at the current price level.

Be the first to comment