olindana/iStock via Getty Images

Etsy (NASDAQ:ETSY) has been struggling for a while now, partially due to a high base from the pandemic, but, in my opinion, also due to poor decisions made by the management in recent times. During the pandemic, Etsy like many growth stocks witnessed a significant improvement in revenue, as the lockdowns pushed people towards Etsy’s products, it also witnessed significant gains from merchants, many of whom used the website to make income. The high levels of merchant growth resulted in high levels of revenue growth, but ever since the pandemic slowly came to a closure, things have not looked as rosy, as gross merchant sale, has essentially come to a halt, with growth being largely flat.

Management’s Decision Making Remains Imperfect At Best

Furthermore, in their investment presentations, management seems to be consistently focused on 2019 as a point of reference, rather than accepting that Etsy has not lived up to the post-pandemic expectations. The reality is the vast majority of Etsy’s merchants were small-scale operations, offering some personal talent in return for basic monetary compensation. Knowing your demographics in business is generally really important, and Etsy has largely done a poor job of this. The company historically focussed on small-scale merchants, rather than higher value, higher margin goods, which is what it is focusing on now, and the strategy may backfire, as it previously relied on small merchants to drive merchandise volume.

While Etsy boasts of margin improvement in its presentation, it’s missing the key to its business, which is its merchants. Merchants and an increase in merchants/offerings is the biggest factor that in my opinion, will drive revenue. Clearly, management has a different take, and it may well be right in the long term.

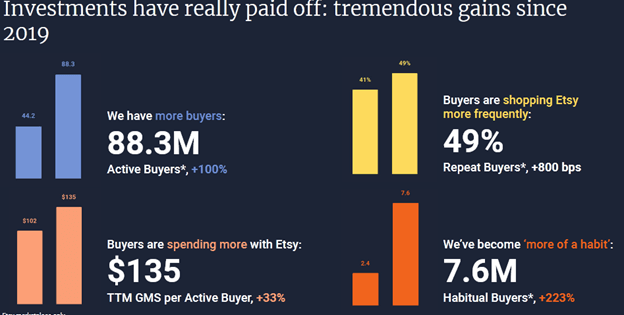

Etsy Statistics (Investor Presentation)

What’s interesting to note is that while in 2021, there was a particularly high base, on which ETSY was working, and that could have contributed to the current reduction in GMW (gross merchant value), the reality is that a lot of merchants have simply chosen to move on from ETSY citing excessive fees.

Etsy’s Fee Structure And Business Outlook

The Etsy marketplace’s third quarter GMS and key buyer cohort metrics reflect further stabilization in year-over-three-year growth trends and our continued success engaging and retaining buyers,” said Rachel Glaser, Etsy, Inc. Chief Financial Officer. “Increased revenue generated from our higher transaction fee is being reinvested in product and marketing initiatives, keeping Etsy handmade and safe, improving customer support, and our new Etsy Purchase Protection program, aimed at building customer loyalty. We love our business model, which enabled us to make these and other important investments in future growth, while simultaneously delivering a very strong consolidated Adjusted EBITDA margin of 28%.”

Spending capital on products is usually a good sign, but questions remain whether moving away from its traditional base will bode well for the company as it moves towards a slightly different business model.

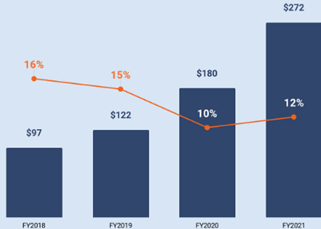

Expanding Product Investment (Investor presentation)

Since the increase in fees, Etsy has not been very open about the total number of merchants on its platform. Clearly, the strategy seems to be turning Etsy into a marketplace where a smaller number of higher margins goods can sustain themselves, and management, in my opinion, does not wish to raise the alarm bells that it might have turned its back on small-scale merchants. While revenue has continued to grow, questions remain about whether the strategy will work in the long term and if the pivot toward higher-valued goods is a reasonable one.

The reality is Etsy is seen as a place where people who had artistic talent but could not monetize their goods traditionally i.e. online or offline sales, turned to Etsy to provide them with a point of sale, many of these sellers were marginalized and had thin margins, which allowed them to make some extra cash. These people may now be on the chopping block, which could backfire.

Taking A Closer Look At The Business Model

While Etsy has done a good job of improving its overall service and platform, offering various new features, including ‘Etsy, made for you’, ‘Reverb’, and ‘elo7’, and Depop, the fashion reseller, the company is still facing headwinds. Etsy is increasingly trying to create a parallel marketplace and expand its product base. But this increasingly puts it in competition with the likes of eBay, albeit, the marketplaces that Etsy offers are a lot more niche, and the overall feel is different. The fashion resell market again brings about mixed emotions, on one hand, there are expectations that it will increase to $77 billion by 2025, as an entire industry pops up, on the other hand, it increasingly provides the feeling that there might be another bubble. We know that sneakers are potentially in a bubble, and a lot of other forms of fashion resell items might be in a similar situation.

Currently, Etsy’s management is sending mixed signals, in terms of quoting multiple addressable market numbers, but has mostly projected an addressable market of $100 billion for what it refers to as its ‘niche’ goods, this seems to be a general theme for the company which is looking to consolidate its merchants. What is important to note is currently, women are the biggest demographics in terms of sellers, and many use Etsy as a key source of income. And as it expands globally, this will be a much more common theme. Small handicrafts are made mostly by women, many of whom may not have the educational background or privileges that allow them to seek a source of income elsewhere. So while the platform can be highly useful for the average seller, it also heading in a direction where international expansion may not integrate well with where its business model is headed.

While it’s true, Etsy may still be cheaper than setting up an entire store, it remains to be seen in terms of absolute cost rather than relative cost, whether or not, merchants will come back onto the platform, and once again drive revenue.

Financial and Technical Outlook

Currently, the revenue growth is primarily being driven by substitution and higher valued goods replacing, lower valued goods, and that means that margins and transaction values are improving, which is translating into a higher EBITDA. Currently, low double-digit growth should be expected in 2023, as global headwinds continue to affect the GMS value. Therefore, with a forward P/E of 38, there is a chance we could see a further correction.

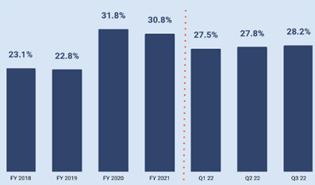

Margins Expansion (Etsy Presentation)

Technicals are currently pointing to similar sentiment from the market with the put-to-call ratio currently standing at 0.91, which is mostly even, as investors wait and watch how the pivot performs. The stock currently trades at slightly lofty valuations and a forward P/E of 38, which could lead to a correction, especially moving away to safer stocks, dividend paying, and discount rates keep rising.

Etsy remains at a key juncture and if it fails to execute its current strategy, it may have to cut fees, as it looks to expand globally. On the other hand, if the company executes well and is able to make the pivot that it intends, the stock could be back to its old ways. Investors would be advised to hold and wait it out for now.

Be the first to comment