Stocks Juggle Strong Economic Recovery and Policy Uncertainty

The Dow Jones, S&P 500 and Nasdaq 100 enjoyed an encouraging start to the year before stumbling into the second quarter. Although domestic economic projections stand strong and the Federal Reserve reiterated its commitment to accommodative monetary policy at its March meeting, US equities entered the quarter on the backfoot. While the broader backdrop remains encouraging and stocks may continue to climb higher gradually in the months ahead, uncertainties remain and seasonality could stymie price action.

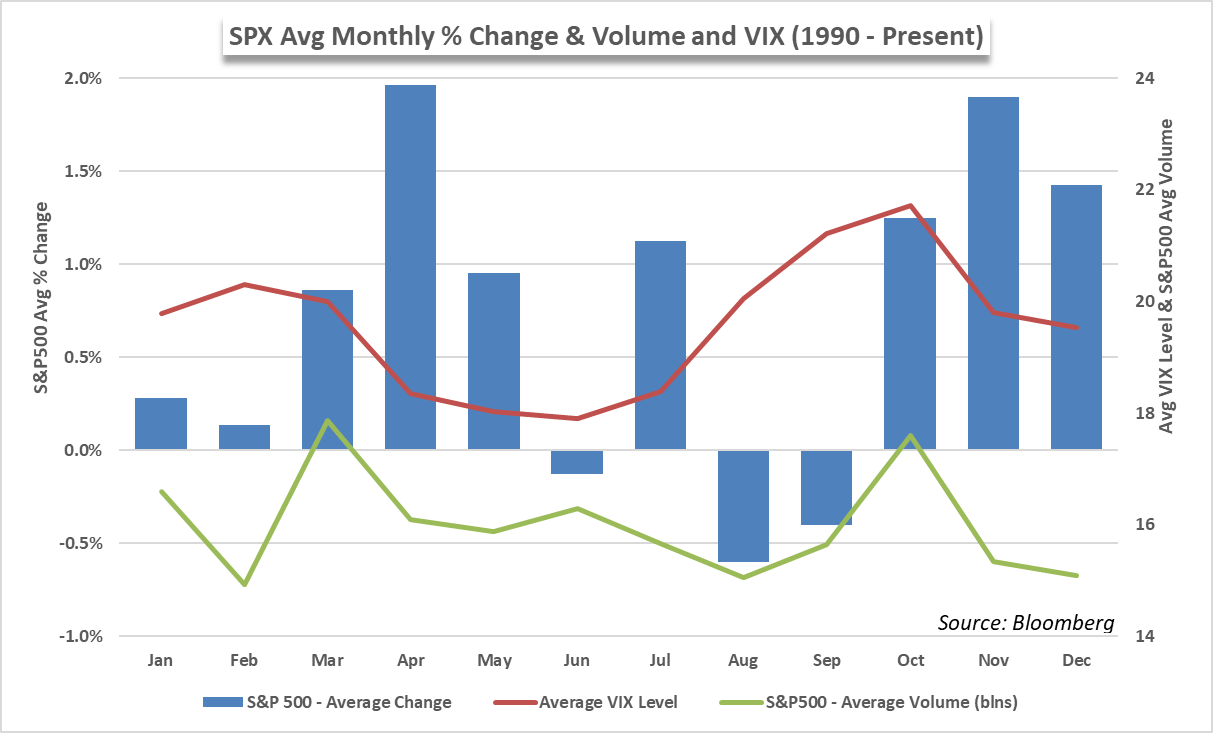

S&P 500 Average Monthly Returns & Average Monthly VIX

{kind=link}

Source: Bloomberg

The S&P 500 has seen a drawdown in volatility and volume from March to August over the last 30 years on average, suggesting the wild price swings experienced earlier in the year may become less frequent unless a novel catalyst presents itself. That said, the average monthly return during the period is generally bullish, although historical averages mean little to future performances. Regardless, the typical drawdown in market activity in the spring and summer months might make range-bound trading more common.

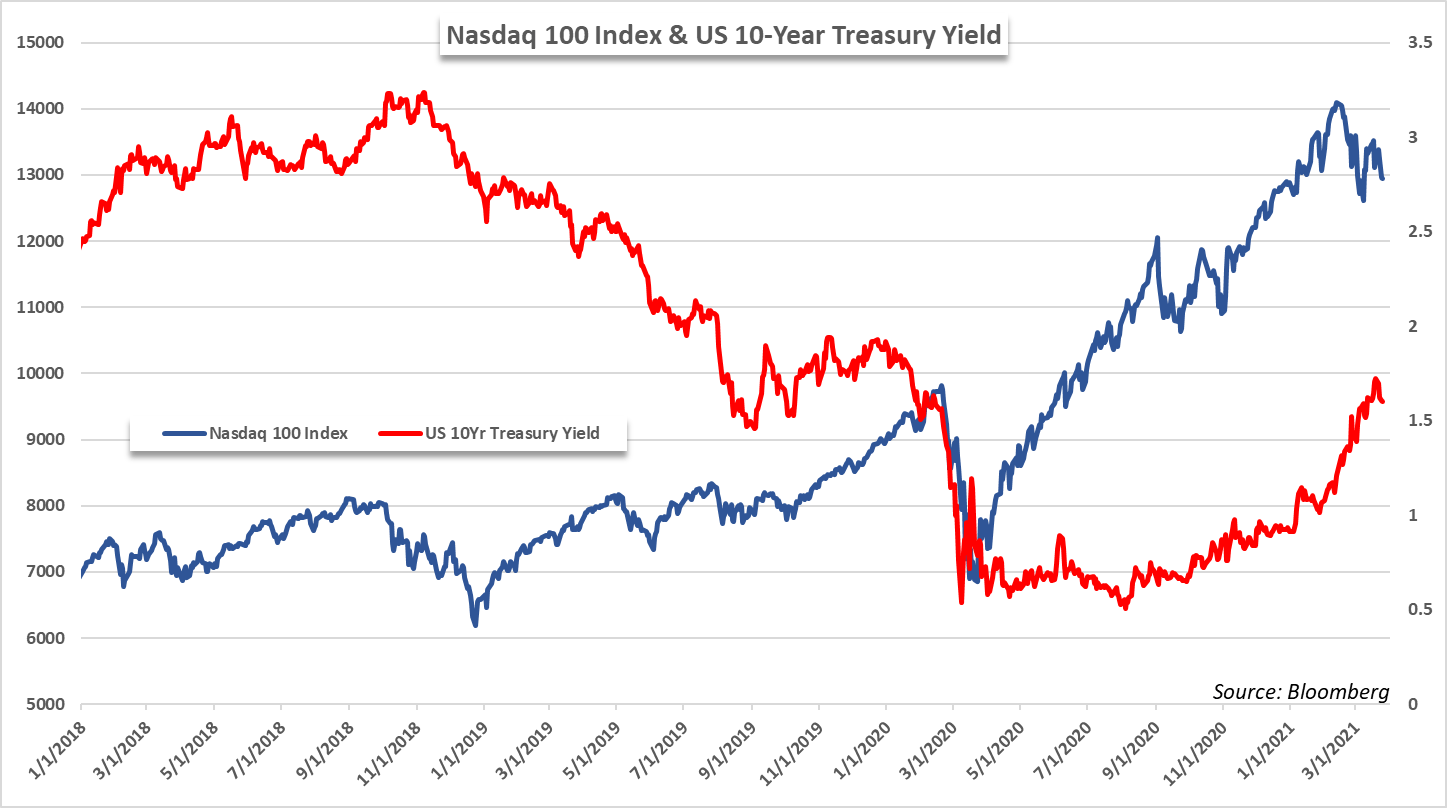

Nasdaq 100 Index & US 10-Year Treasury Yield

Source: Bloomberg

In the meantime, US indices will have to negotiate potential tax hikes, anti-trust action and infrastructure spending. Inflation expectations have cooled, but further gains in US Treasury yields may also remain a threat. While each theme presents different risks, it can be argued the technology sector, and therefore the Nasdaq 100 by extension, are the most vulnerable. With that in mind, broader equity weakness might see losses in the tech-heavy index outpace that of the S&P 500 and Dow Jones – the latter of which is well positioned for any eventual infrastructure spending.

DAX 30, CAC 40 & FTSE 100

European indices will also look to continue their post-covid recovery but may be hampered by weak vaccination rates and a resurgence in coronavirus cases relative to the United States and other developed nations. As a result, EU members may continue to impose lockdown measures or restrict cross-country travel, potentially constricting economic activity and slowing recovery efforts. Beholden to corporate earnings and broader economic trends, European indices like the DAX 30 and CAC 40 may suffer.

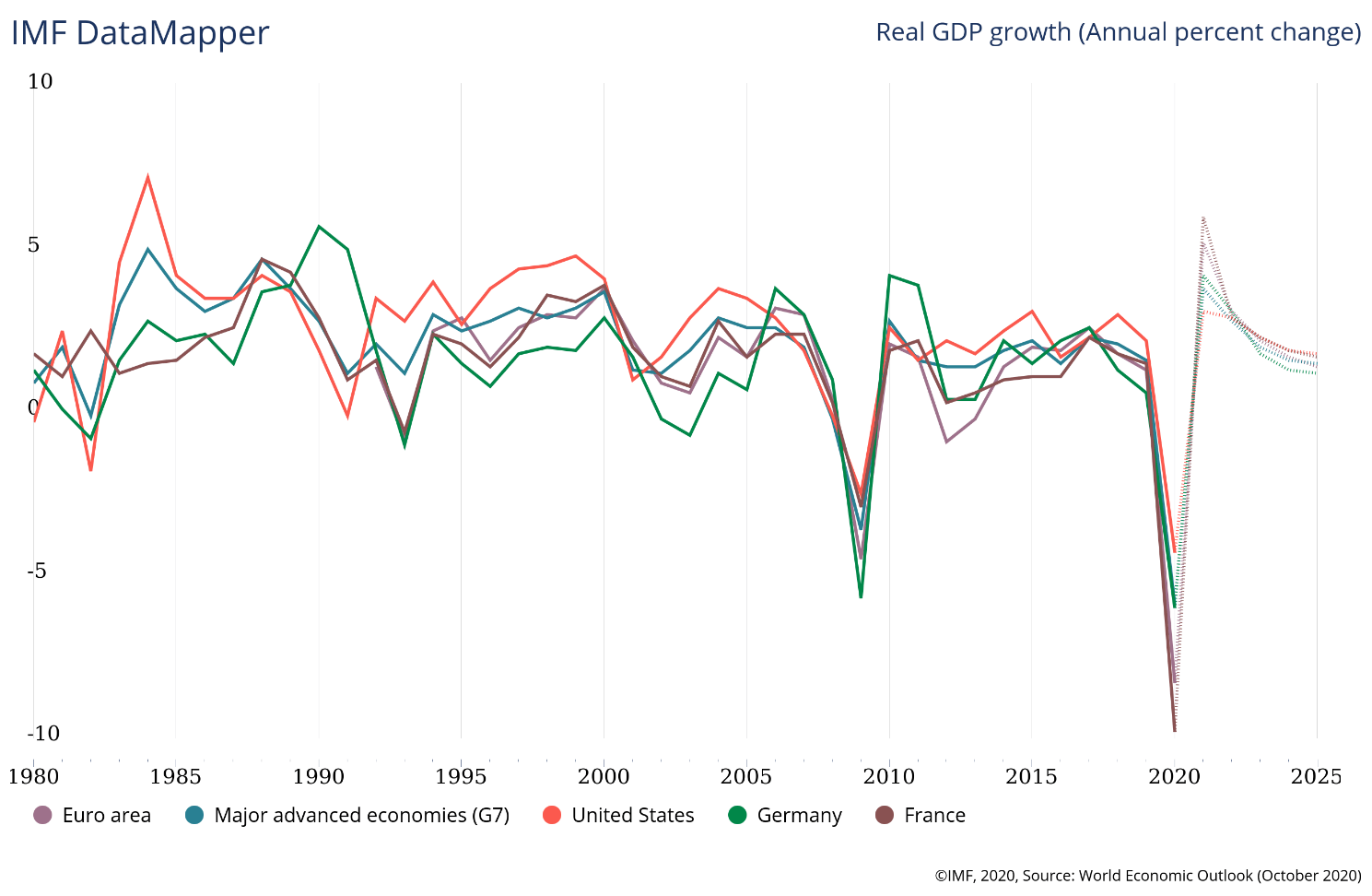

IMF World Economic Outlook GDP Projections

Source: IMF World Economic Outlook

That being said, inflation measures continue to underwhelm which may allow for prolonged support from the European Central Bank and local governments. Accommodative policy and projected economic growth create an encouraging backdrop for the major European indices but, as with many years in recent decades, any progress to the topside will likely lag that of the Dow Jones, Nasdaq 100 and S&P 500 as evidenced by their respective growth expectations.

Be the first to comment