Oselote

Dear readers/followers,

Artificial Intelligence (AI) has been the hottest topic for several months now and understandably investors have been asking themselves how to position themselves in order to benefit from this growing trend. I have been asking myself the same question and believe that there are basically two ways to do this. Either you invest in the companies that will develop AI and benefit from integrating it into their businesses or you invest into the companies that will provide the necessary infrastructure that will allow AI to operate.

Option #1 – invest in tech giants directly

Ideally we could invest directly into companies that are developing AI. The issue is that the companies that are on the forefront of innovation in the industry (such as Open AI with their ChatGPT) are often privately held entities that investors are not very familiar with and frankly cannot invest into unless they have connections in the VC community in Silicon Valley. That leaves us with the option of buying the already established tech giants, mainly Microsoft (MSFT) and Google (GOOGL), both of which have declared their respective visions incorporating AI into their products, are actively working on it and likely have the financial means to make it happen.

Microsoft seems better positioned in the race as it already has a partnership with Open AI which dates back to 2019 (when they first invested $1 Billion and became the exclusive cloud computing services provider to Open AI). They have recently announced that they will double-down on the investment.

Google seems to be one step behind, forcing them to declare an internal “code-red” to speed up development of AI and related services. Things however don’t seem be going that well, as during a recent presentation the Google’s AI-powered chatbot Bard made a mistake, causing the stock price to plummet by almost 10%.

Investing into these companies is a perfectly valid way to get exposure to AI. The drawback is that AI still only accounts for a small percentage of the overall revenue of these companies so you’re also getting exposure to Google’s advertising business, Microsoft’s personal computing etc. Moreover, although the price of tech has decreased significantly in 2022, these companies have still not reached dirt-cheap levels (especially not Microsoft) and with a potential slowdown/recession still not out of the picture big tech could still be risky. So that brings us to option number two.

Option #2 – invest in the infrastructure

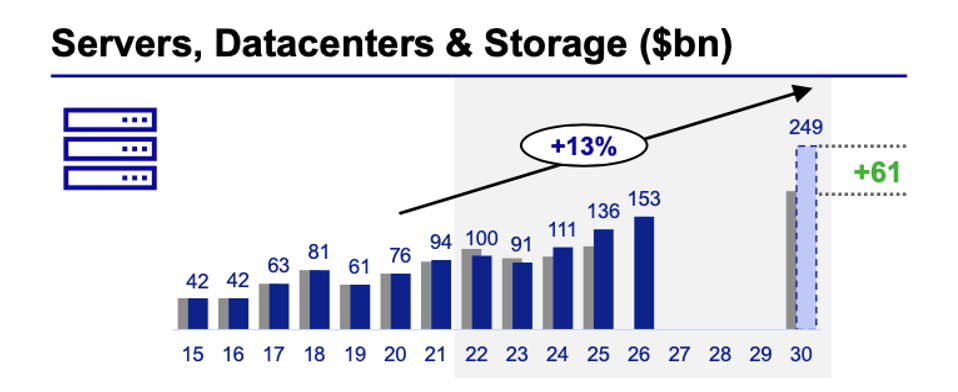

The best way to get rich during the gold rush was to sell shovels. And that’s exactly what I mean be investing in the infrastructure. In order for AI to be used in our day-to-day lives, enormous amounts of computing power will be needed. This means a ton of chips and a ton of data-centers – an industry that is expected to grow by 13% annually over the next decade, according to ASML’s Investor Presentation.

ASML Investor Presentation

This is impressive growth, but for this option #2 to be better than simply buying big tech, we need a company that will benefit from the growth of AI but can also be bought a good price today giving us a bigger margin of safety compared to big tech and a high enough expected total return. In this article I want to focus on a major data center REIT and determine whether it makes a good investment based on the criteria above.

Equinix

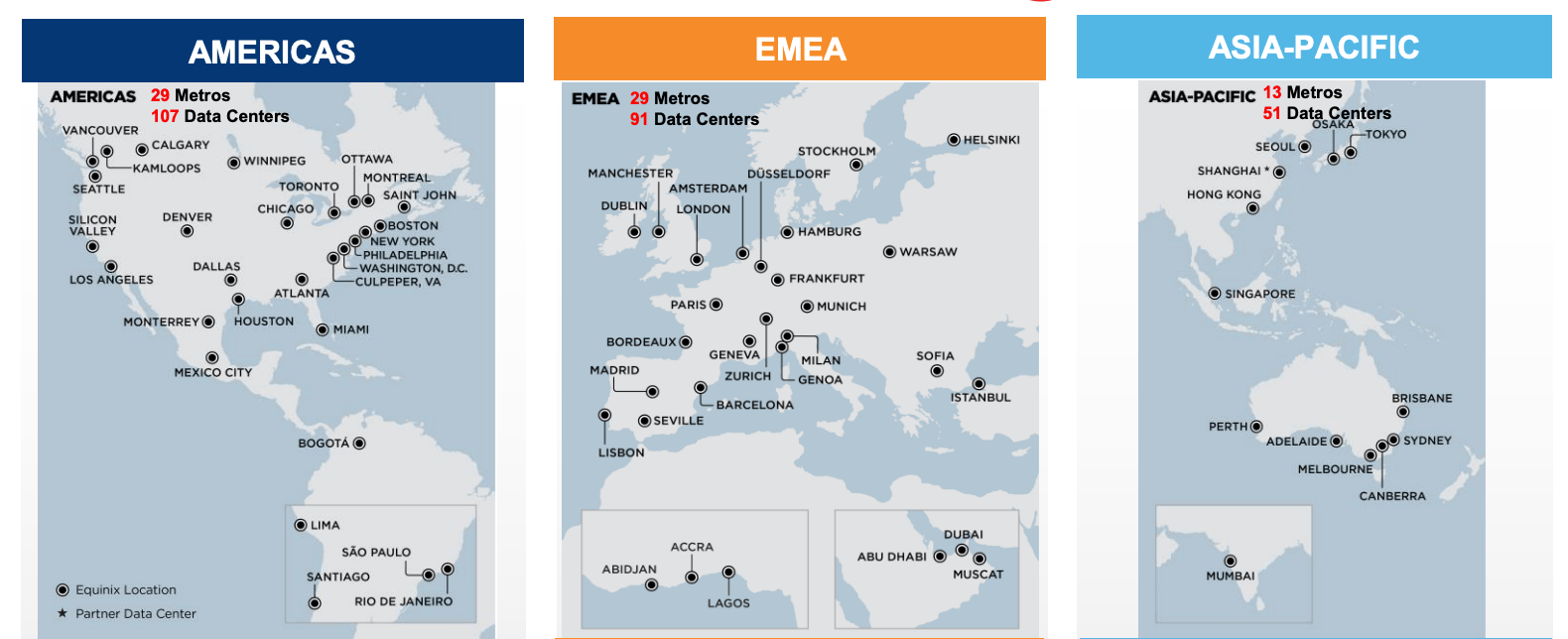

Equinix (NASDAQ:EQIX) is a globally diversified REIT which operates 249 data centers located in 71 metropolitan areas in the North and South America, EMEA and Asia-Pacific. Of these, the company owns 135 locations and leases the rest with the majority of leases (70%) being very long-term, expiring after 2037. The REIT is committed to growing, with 14 new locations announced in 2022, as they aim to capture first-mover advantage in future global hubs.

Equinix Q3 2022 Report

The revenues are relatively well diversified across tenants, region and industry segments with no single tenants accounting for more than 2.5%. The majority of tenants operate in the IT & Cloud sector and yes a lot of these tenants are big tech names (more on the risks of this later).

Operations

Q4 Earnings are coming out next week and the company has guided to an FFO of around $29.2 per share. If they can achieve this, it would represent a solid 10% increase YoY, even against FX headwinds. The growth has been driven by their aggressive expansion and also very solid same-store revenue which has increased by 7% YoY (with a 69% cash gross margin) as reported in their Q3 2022 results. Q4 2022 will also be the company’s 80 quarters of sequential revenues growth which speaks to the quality of the company and its leadership.

Equinix Q3 2022 report

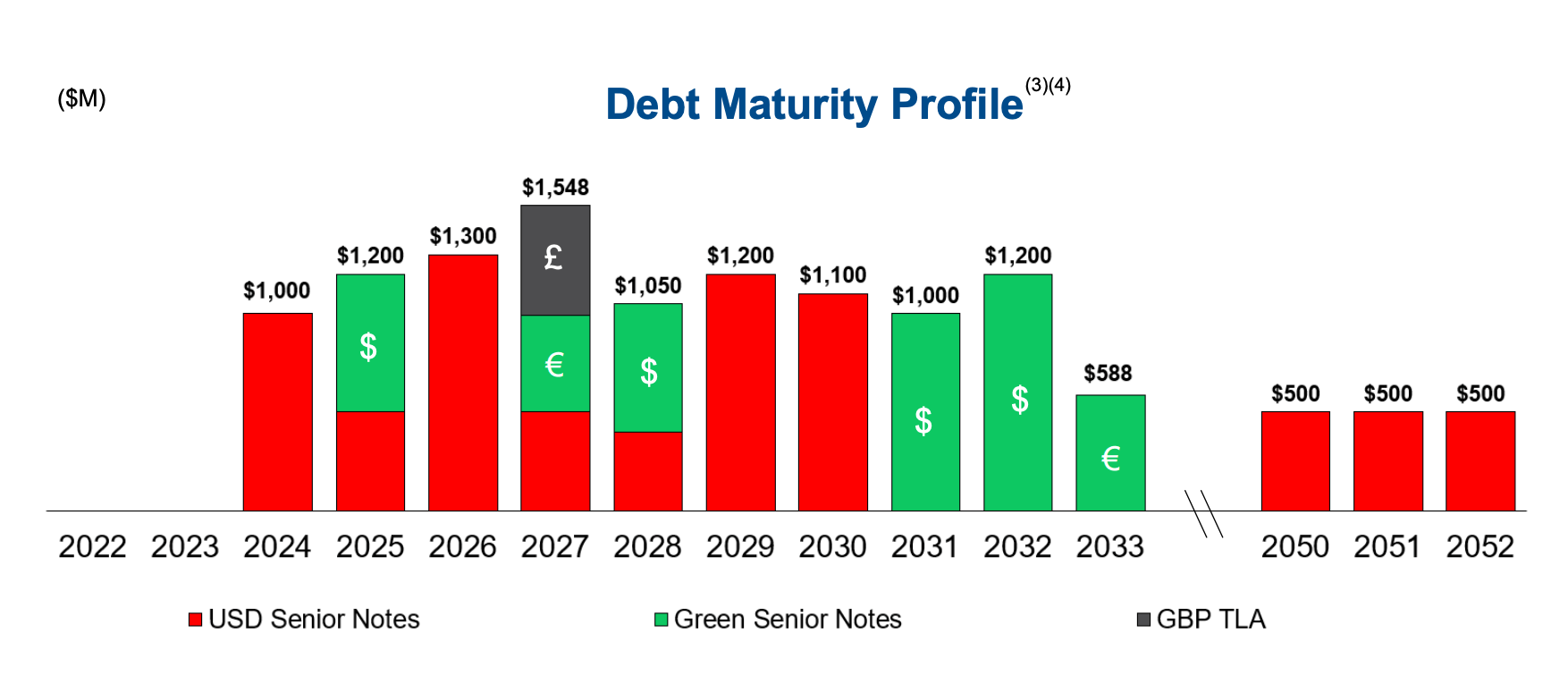

The company has $12.7 Billion of debt, 96% of which is fixed and with a blended rate of only 1.96% (this is great compared to fed funds rate at 4.5%). The debt maturities are spread over time, with no repayments in 2023 and $1 Billion due in 2024. However, with total available liquidity of $6.4 Billion ($2.5 Billion of which is cash with the rest being a revolving credit facility) the company is in a very good financial position and could easily repay the debt due in 2024 if for some reason it is not able to refinance. With regards to their balance sheet, I would consider Equinix as very healthy (especially when compared to other REITs). This is reiterated by a BBB rating.

Equinix Q3 2022 Report

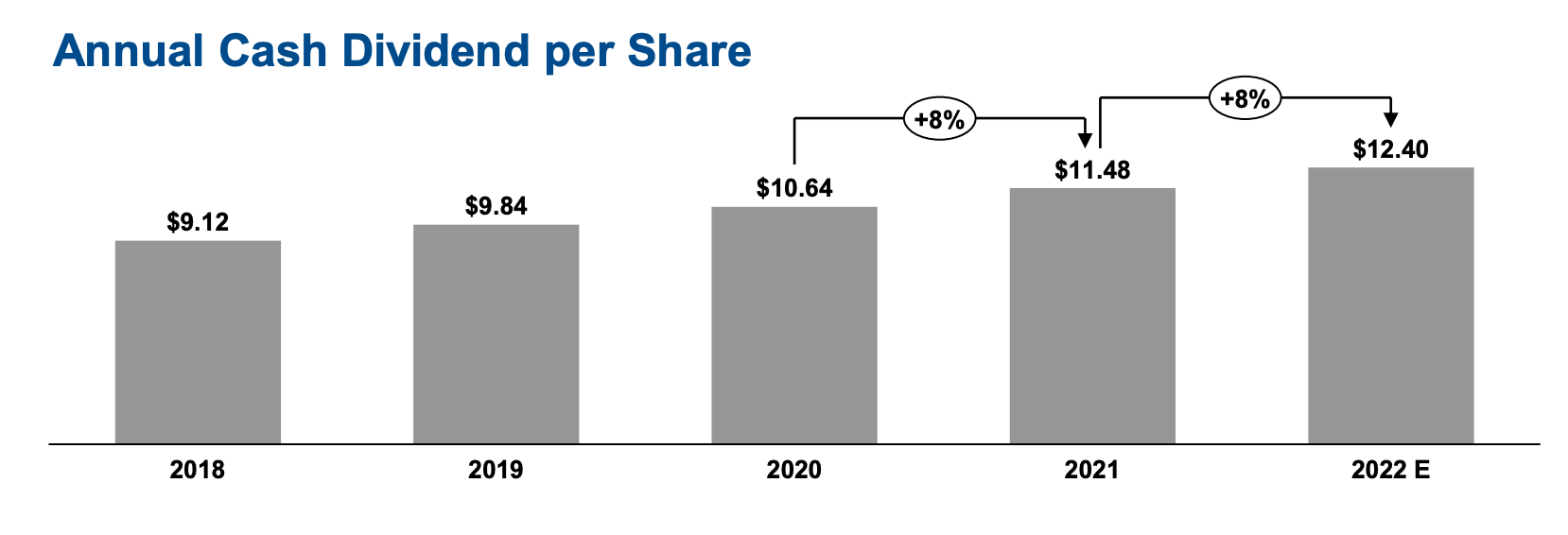

The company has grown its dividend for 7 consecutive years with a 5-year CAGR of 9.2%, but the yield is still low for a REIT at only 1.7%. On the flip-side, the company has a lot of room to increase the dividend going forward as the payout ratio is currently 43% and earnings are expected to grow rapidly. As such I wouldn’t be surprised if the company continued to increase its dividend by 8-10% a year going forward.

Equinix Q3 2022 Report

Valuation

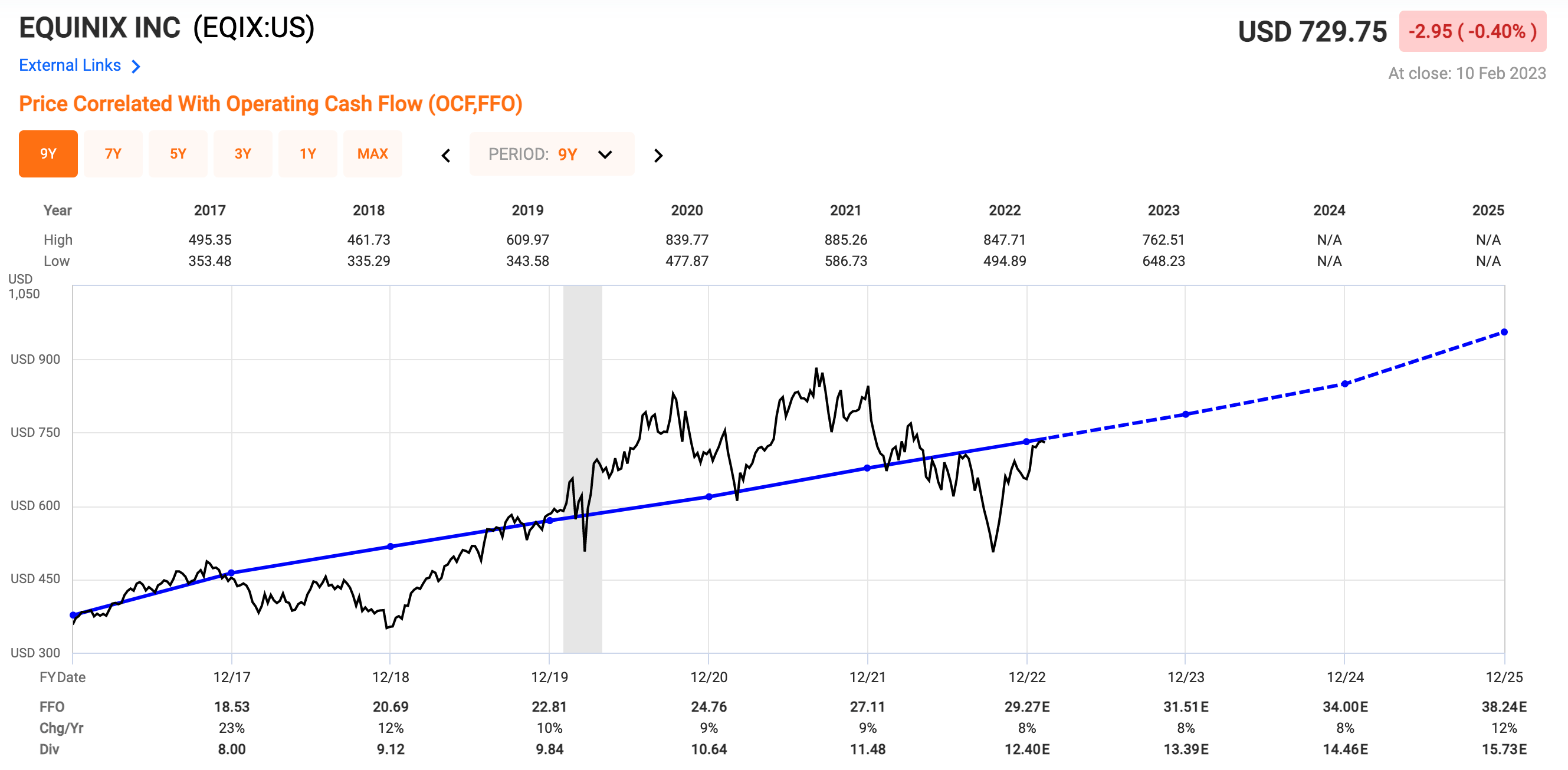

From a relative valuation perspective, the REIT currently trades at 24.7x FFO. This is in-line with the historical average multiple (between 2016-2022) of 25x FFO. Of course one could argue for a higher multiple (vs say in 2016) due to the abnormally high expected growth driven by AI, but at the same time we have entered an environment with higher interest rates which would justify a lower multiple. Overall I think these two effects will balance out and the fair value multiple will lie close to its historical average.

According to data on SA, analysts are expecting FFO to grow by almost 10% per year for the next three years. This would mean that FFO could reach $38.00 per share by 2025. At a 25x multiple the price would be $950 per share (30% up from $730 today). This would translate into a 10% annual price appreciation + 1.7% yield = 11.7% total return. Not bad and certainly above the market.

Fast graphs

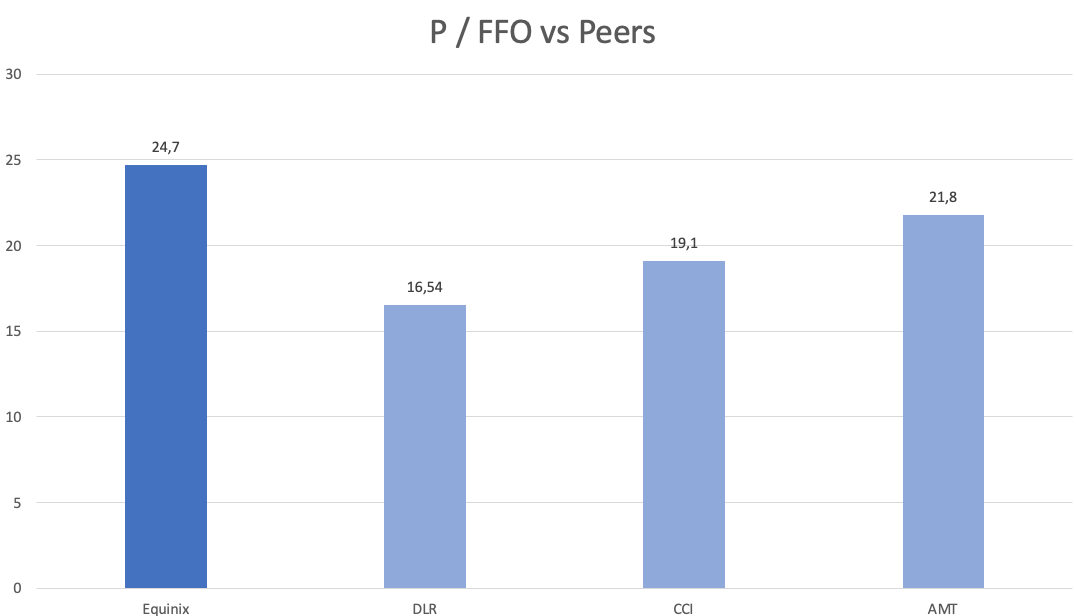

Relative to other digital infrastructure REITs, Equinix trades at a significant premium in terms of P/FFO (see chart below). This is because although EQIX trades like a REIT, it is also a tech stock, which operates a unique one of a kind Telecom infrastructure business. Because of this the peers we can look at aren’t in exactly the same business and therefore we can’t really make one-to-one comparisons. Still the comparison gives an indication that we are probably not getting the company at a massive discount here nor are we overpaying significantly (if we assume that EQIX should have a premium compared to the peers). This reiterates that the stock seems more or less fairly valued here.

Created by Author based on data from Fast graphs

Risks

Of course no investment comes without risk. The biggest one here is the competition that data centers will face from some of their biggest tenants from big tech. Large companies that are leaders in the cloud computing space (including Amazon, Google, Microsoft and others) are amongst the largest tenants of Equinix and all of them are adding to their own data centers. It is not hard to imagine that these large companies will make the decision to house all of their servers in-house which would hurt Equinix’s performance significantly. This has been the motivation why some funds decided to short data center REITs in 2022 (e.g. Chanos & Company) and frankly is what has stopped me from investing in the sector so far as I am not able to determine whether or not big tech will make the move and therefore I demand a discount in order to consider the investment.

Investor Takeaway

AI has been a hot topic and I think most investors should try to get some exposure to this growing trend. There’s the traditional way to bet on big tech and then the alternative way to “sell shovels during a gold rush”. Today we focused on the latter and in-particular on a data center REIT Equinix which could provide the desired exposure to the growing sector.

The REIT’s operational performance has been superb. It has increased its revenue for 80 consecutive quarter, with a 10% increase over the past year and it has a great BBB-rated balance sheet with 96% of debt fixed at sub 2% interest rate. Moreover, it has enough cash to repay any debt due over the next two years. The only drawback for income investors is the dividend yield, which only stands at 1.7%. Still with FFO and earnings expected to grow by around 10% a year for the next 3 years, the stock could be expected to generate a total return of almost 12%.

Overall this can make a pretty good investment as the company has been doing very well. Personally though, I view the potential risk of big tech leaving and moving their operations in-house as significant and would need a discount in order to invest (trading at fair value doesn’t give me enough of a margin of safety to balance out this risk, though this is subjective). Frankly, we already got the discount last fall (with the stock trading at just 18.5x FFO in October) and if you bought at $500-$600, congratulations. I didn’t, so Equinix is a “HOLD” for me here at $730 for the aforementioned reasons, but I would like to start a position if we get a pullback below $650 or so.

Be the first to comment