Leestat

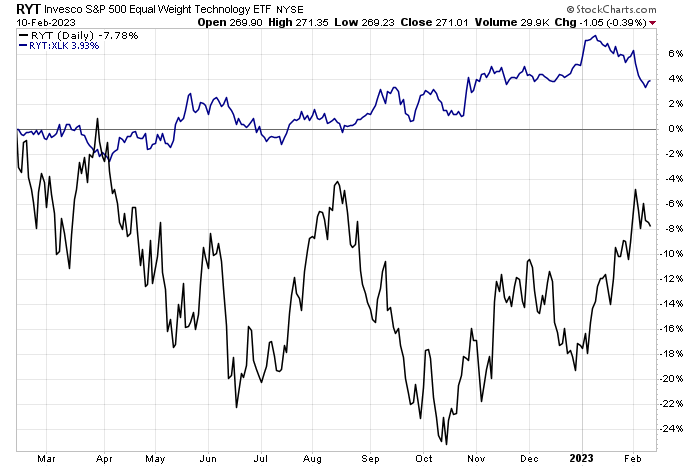

Large-cap tech has staged a 2023 recovery. As a market technician, I like to investigate trends in how small vs. large stocks are doing. One method is to compare an equal-weight sector ETF to its traditional cap-weighted peer. In this case, the equal-weight tech ETF (RYT) has yielded some of its 2022 gains on XLK since early January. The broader trend remains in favor of RYT, though.

Let’s dive into one mid to large size IT firm with earnings later this week.

Equal-Weight Tech Gives Back Some Relative Gains to XLK

Stockcharts.com

According to Bank of America Global Research, EPAM Systems (NYSE:EPAM) provides complex software development and engineering, as well as high-end digital IT services to clients located primarily in North America and Europe, employing specialized engineers primarily from lower-cost Central/Eastern European countries. EPAM maintains a bench of high-quality software engineering talent, and the company’s clients primarily consist of Forbes Global 2000 corporations. In F21, EPAM generated revenues of $3.76B.

The Pennsylvania-based $21 billion market cap IT Services industry company, ranked 3 out of 30 by Seeking Alpha, within the Information Technology sector trades at a high 51.9 trailing 12-month GAAP price-to-earnings ratio and does not pay a dividend, according to The Wall Street Journal.

Back in November, EPAM reported an operating earnings beat of $0.57 with total per-share profits of $3.10 on revenue of $1.23 billion, also better than the consensus estimate. Guidance was a tad soft, however. Despite headwinds from Russia’s invasion of Ukraine a year ago (the firm has 40% of its employees are from that region), the company has been resilient. Still, there are risks including further volatility in the Russa/Ukraine/Belarus area that could impact EPAM’s biggest clients along with broader competition for workers in the IT space.

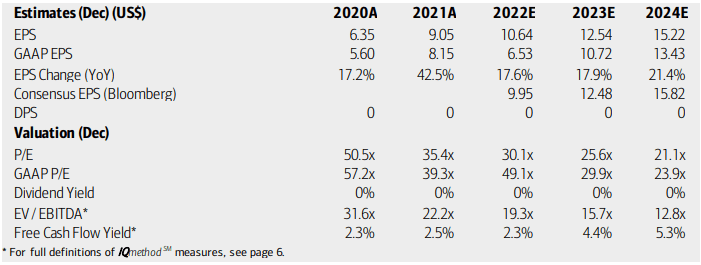

On valuation, analysts at BofA see earnings having climbed a strong 18% in 2022 and similar EPS growth trends are seen through next year in the face of instability abroad. The Bloomberg consensus forecast is about on par with what BofA sees. EPAM has modest free cash flow, and dividends are not expected to be initiated any time soon. With an operating and GAAP P/E north of 20 using 2023 figures, shares are not cheap.

But it’s important to consider the growth trajectory in the valuation. I like to use the forward non-GAAP PEG ratio in cases like these. Right now, Seeking Alpha shows a reasonable 1.64 PEG – about in line with the sector median and a more than 20% discount to EPAM’s 5-year historical average PEG. Overall, the valuation seems fair to me given the growth outlook. Call it a GARP play.

EPAM Systems: Earnings, Valuation, Free Cash Flow Forecasts

BofA Global Research

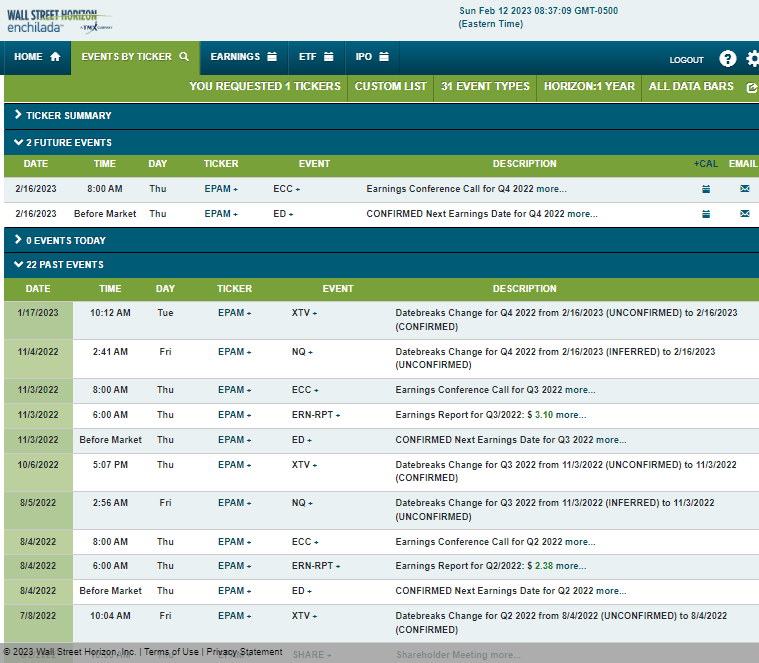

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Thursday, February 16 BMO with a conference call immediately after results cross the wires. You can listen live here. The calendar is light on volatility catalysts aside from the reporting date this week.

Corporate Event Risk Calendar

Wall Street Horizon

The Technical Take

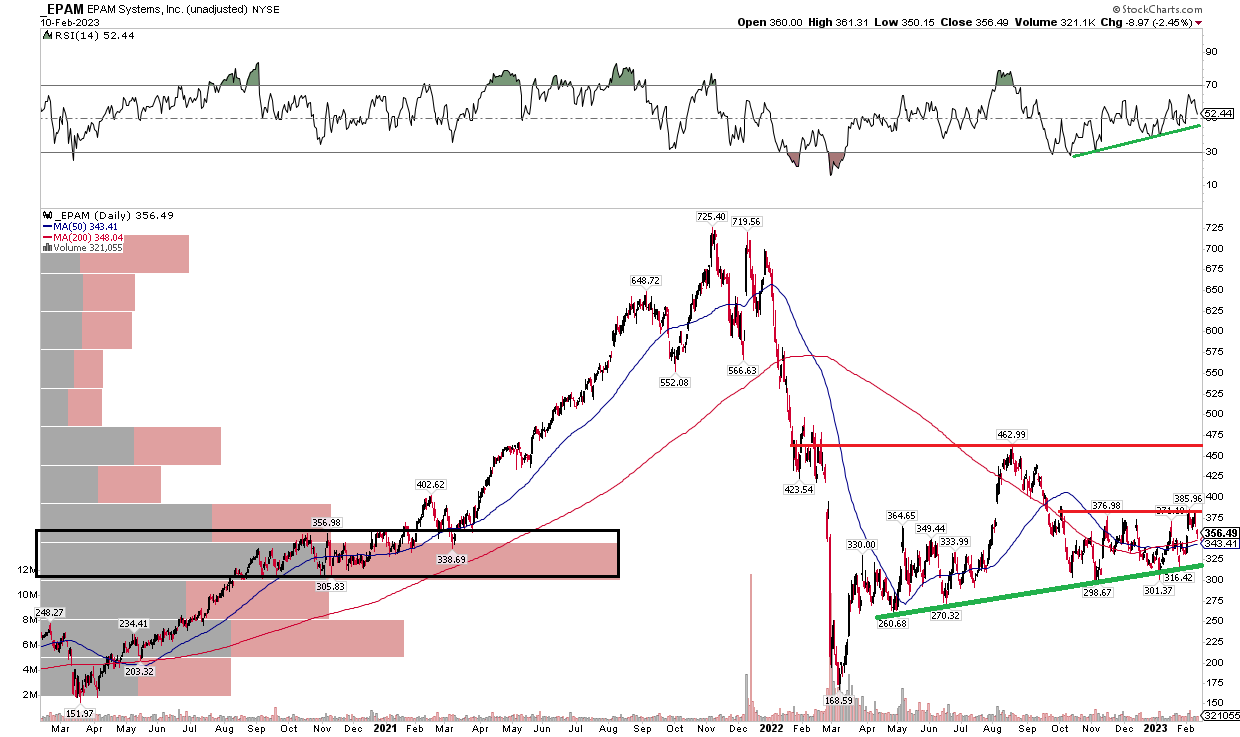

With a fair to slightly favorable valuation, how does the chart look? Notice in the graph below that EPAM is consolidating with an uptrend support line and horizontal resistance line. I see the $370 to $386 area has a defense zone by the bears – a breakout above that area would support the case for a push higher to the September 2022 peak above $460. Should $300 break, though, a very bearish measured move to under $200 would be triggered, but the March 2020 low of $170 could attract buyers.

That is a dramatic possible scenario, but I am more encouraged by rising RSI momentum that could portend an eventual bullish breakout in price. I would wait and see what happens with the noted support and resistance levels before jumping in. High volume by price from $300 to $360 may also cushion further downside moves.

EPAM: Consolidating with Improving Momentum

Stockcharts.com

The Bottom Line

EPAM trades at a premium P/E for good reason, but it’s not super cheap here. The chart is also just in consolidation mode. I am a hold for now, but this week’s earnings report could provide new pieces of evidence.

Be the first to comment