jetcityimage

As the out-and-out leader in EV charging with more than 70% share of Level 2 chargers in the US, ChargePoint (NYSE:CHPT) stands to benefit even if EV growth slows, with revenue growth projected in the low-60% range. Improving operating leverage and gross margins are also a positive, but under the surface, expenses are still way too high to drive a meaningful shift to profitability through 2023.

EV Market Growth In Question In 2023

With one month down so far, it’s hard to predict exactly where the EV industry will end the year — other OEMs such as Ford (F) have followed Tesla’s (TSLA) price cuts in efforts to spur demand, which look to be paying off — Tesla recorded over 900% growth in Germany and 18% growth in China following the cuts took effect.

S&P Global believes that EV growth momentum “is at risk in 2023 due to several factors: the end of China’s subsidies, Europe’s energy crisis and the consequent inflation, and recession fears in the US.” S&P sees that the majority of the benefits to EVs from the Inflation Reduction act won’t be realized until 2024, thus creating a potential headwind to EV sales in the US through 2023.

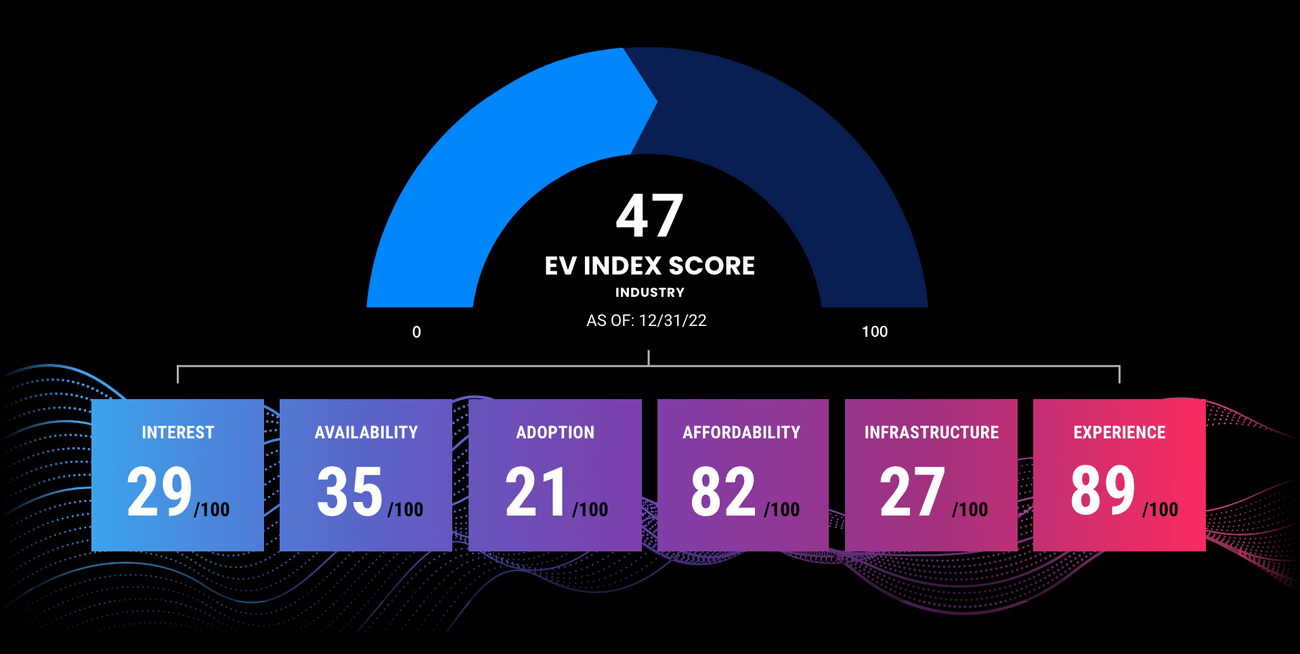

However, forecasts for growth differ — J.D. Power “says overall BEV retail market share will jump to 12% in 2023 and 21% by 2025, a forecast it calls its middle-of-the-road projection, meaning growth could come even faster.” This forecast is based on availability and adoption — how many EV options are available, and how many consumers who have viable EV options purchase one. McKinsey “predicts legacy automakers and EV startups will produce up to 400 new models by 2023″ — this would handle availability and pave the way for broader adoption.

J.D. Power EV Index

Regardless of the pace of growth in 2023 for the EV market — whether it’s 20% y/y or 35% y/y, ChargePoint still stands to benefit — infrastructure is still lacking, especially from the viewpoint of the Class 8/heavy duty sector. Freightliner Cascadia manufacturer Daimler Truck North America CEO John O’Leary sees that the “infrastructure is slowing us down in terms of EV deployment.”

It’s no doubt EV charging infrastructure is still a headwind for EV adoption — a lack of widespread, readily accessible charging stirring range anxiety fears has pervaded the industry for years. S&P Global Mobility believes EV charging infrastructure “needs to be quadrupled by 2025, and to grow more than eight times by 2030,” in order to meet growing EV demand. For 2023 through 2025, government grants allocated via the Inflation Reduction Act will help spur larger investments nationwide in EV charging, benefiting operators such as ChargePoint, Blink (BLNK), EVgo (EVGO), and others.

Strong Revenue Growth Ahead

ChargePoint’s recent Q3 results saw the EV charging operator record ~90% y/y revenue growth, with a small boost to full year revenue guidance, now seeing revenues between $475 million to $485 million. At the high end of that guided range, ChargePoint would be on track to record ~100% y/y growth.

For fiscal 2024, ChargePoint could record 60% or higher revenue growth, to $780 million, regardless of the overall pace of growth in the EV market. Even with 20% growth in EV sales during calendar 2023 (fiscal 2024), the broader increase in EVs on the roads, combined with an increase in charger deployments set the stage for revenue to continue to accelerate.

Subscription growth still lags behind charging systems revenue growth — for Q3, charging systems revenue more than doubled, from $47.5 million to $97.6 million, while subscriptions only grew 61.7% to $21.7 million. As a percentage of revenue, subscriptions dropped to 17.3% of revenues from 20.6%; for the 9-month period, subscriptions dropped to 18.9% from over 22%.

For fiscal 2024, a similar trend is expected to pan out — charger installations, boosted by states working to improve charging infrastructure via the IRA, are expected to lead revenue growth, while subscriptions will continue at a modest pace. For example, continuous creation of partnerships such as the recent tie-up with Mercedes-Benz to deploy a network of 2,500 chargers is a core driver of this 60% revenue growth projection.

Margin Improvement, But OpEx In Focus

With strong revenue growth ahead, the main focal point of ChargePoint’s fiscal 2024 comes down to margins — gross margins have dipped through FY23 relative to FY22, but are showing signs of sequential improvement. For FY24, the question remains if ChargePoint can regain a 25% gross margin and improve operating leverage to put it on a fast track to profitability.

ChargePoint

And at the moment, operating expenses still look too high to drive a meaningful shift to profitability throughout FY24.

From Q1 ’23 to Q3 ’23, ChargePoint has seen a fairly meaningful decline in operating expenses as a % of revenues, down from 103% to start the fiscal year to 63% as of Q3; on a dollar basis, quarterly operating expenses declined $5 million.

However, the issues start to stem from the recent gross margin declines — operating expenses for Q3 are approximately 4.7x gross profit, and about 6x gross profit for the 9 month period. It’s not much an improvement from the comparable nine-month period in FY22, when operating expenses totaled just under 6.2x gross profit.

In essence, even with revenues up nearly 96% y/y for nine month period ending in Q3, operating losses widened over 41%.

We see a worrisome trend for the nine-month period:

- subscription gross margin has decreased 450 bp to 37.3%, even with Q3 contributing 36% of the nine-month’s total revenue at a ~62% margin

- networked charging systems gross margin has decline 470 bp to 10.3%

Margins have shown some improvement sequentially from the beginning of FY23, but overall, margins are not strong enough to offset increasing levels of operating expenses. FQ4 ’23’s operating expenses are expected to reverse the slow decline seen so far in fiscal ’23, rising to $86-89 million on a non-GAAP basis (about $102-106 million GAAP).

Where does this take ChargePoint for FY24?

For FY24, operating expenses are estimated to grow about 35% from FY23’s expected ~$420 million, given current spending trends, ending the fiscal year at around $570 million. At estimated revenues of $770 million, based on EV market growth and increased deployments, gross profits would come in around $185 million at a 24% gross margin.

Given those two figures, net loss for FY24 is projected at ~$385 million GAAP; assuming similar growth in SBC expense to ~$120 million, non-GAAP net loss is projected at ~$265 million, or a loss of about ($0.76) per share assuming around 2-3% dilution.

With operating expenses still totaling far above 4x gross profit, it’s hard to see a rapid inflection in operating profitability, even as margins are showing signs of improvement and as revenues scale higher. Net loss for FY24 is not expected to show any improvement in loss per share, if at all. The expected uptick in FQ4 ’23 operating expenses — and only decreasing operating expenses on a non-GAAP basis by ~$1 million — is not the trend needed to unlock profitability until at least FY25, potentially FY26. Given the dim outlook on profitability, ChargePoint’s shares may struggle to find meaningful upside in 2023, similar to the range-bound trading from 2022.

Be the first to comment