zhengzaishuru/iStock via Getty Images

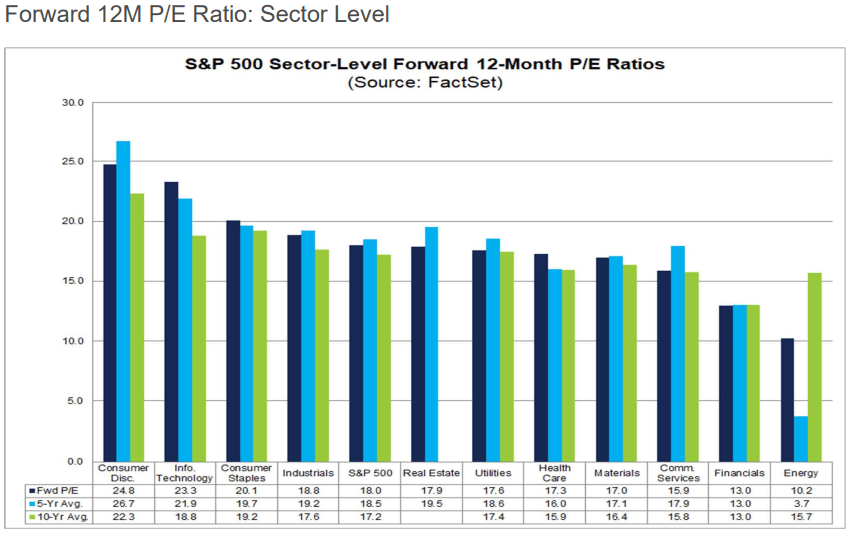

The Energy sector remains attractively priced. At just 10 times forward earnings, according to the latest John Butters Earnings Insight at FactSet, it’s the cheapest sector of the market and there has been improving price action among some of the group’s biggest stocks despite a rocky start to 2023.

One large-cap domestic name reports earnings later this month, and I spotted an anomaly that could portend positive results. But are shares of EOG a buy on valuation and technicals, too? Let’s weigh all the factors.

Energy Sector: Cheapest Area

FactSet

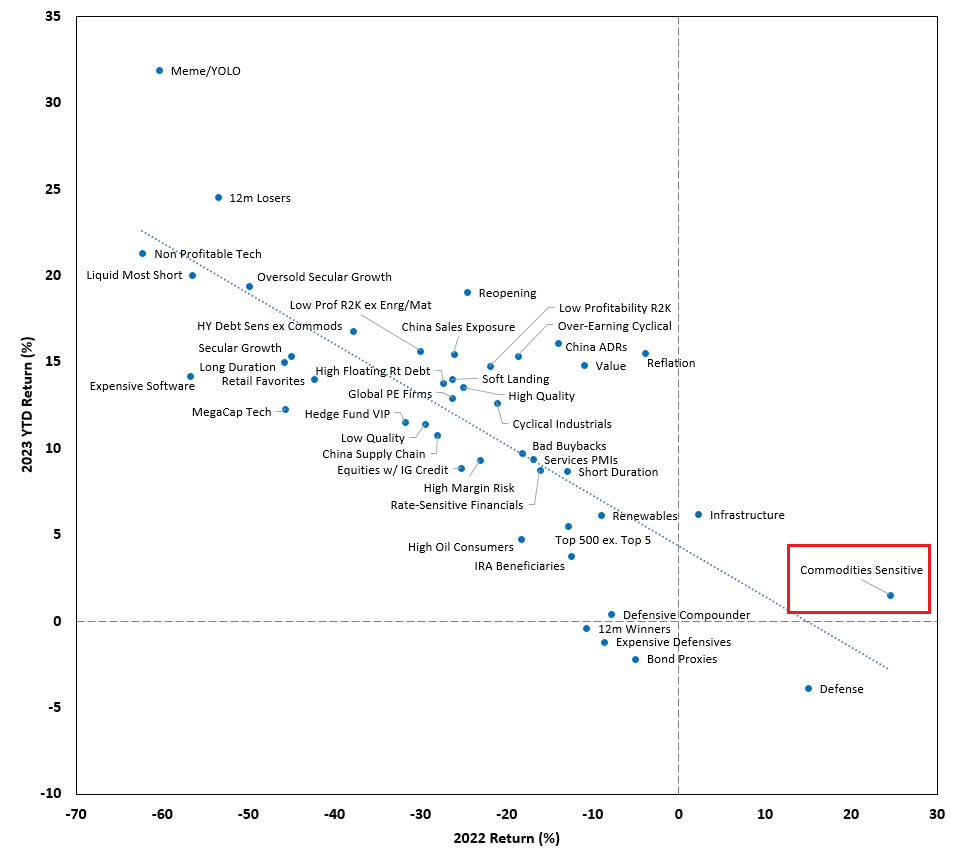

What Worked in 2022 Ain’t in 2023

Goldman Sachs

According to Bank of America Global Research, EOG Resources (NYSE:EOG) is one of the largest independent E&P companies operating in the United States. At year-end 2018, EOG had estimated proved reserves of 2.9bboe. Full-year 2018 production averaged 719mboepd comprising of 400mboepd of crude oil, 116mboeped of NGLs, and 1,219mmcfepd of natural gas.

The Houston-based $75 billion market cap Oil, Gas & Consumable Fuels industry company within the Energy sector trades at a low 10.5 trailing 12-month GAAP price-to-earnings ratio and pays an above-market rate dividend yield of 2.5%.

Ahead of earnings on the 23rd, the stock has a low 1% short interest. Key for EOG is growth in the Permian region, and the CEO recently said supply pressures are easing which should allow for more production in that shale spot.

On valuation, analysts at BofA see earnings having risen by a whopping 56% last year. That followed a major EPS jump in 2021. Per-share profits are seen as climbing another 20% in 2023 before they finally moderate to the $12 to $13 range next year. The Bloomberg consensus forecast is about in line with what BofA sees.

Dividends, meanwhile, are expected to continue to rise big – nearing $12 this year (an 8% forward yield) but then dropping back in 2024. Both EOG’s operating and GAAP P/Es are very attractive here around 10. At latest check, the non-GAAP earnings multiple is under 9, all while the free cash flow multiple is just 10. Finally, EOG’s EV/EBITDA ratio is about half that of the broad mark, under 5. With oil and gas prices way off the highs from 2022, there is some risk that lower commodity prices could result in a revision lower in free cash flow expectations, but EOG’s strong balance sheet should help buffer against oil price drops compared to other more leveraged plays.

EOG: Earnings, Valuation, Dividend Yield Forecasts

BofA Global Research

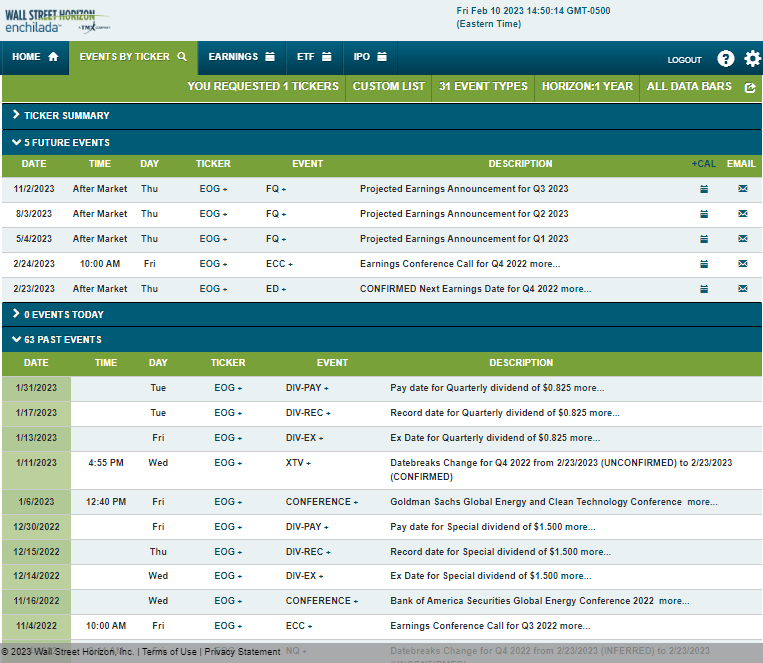

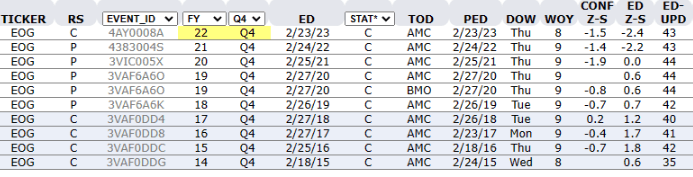

Looking ahead, corporate event data provided by Wall Street Horizon show a confirmed Q4 2022 earnings date of Thursday, February 23 AMC with a conference call the following morning. You can listen live here.

I dug into it, and it turns out that EOG confirmed its earnings date much earlier than usual. Why does that matter? There’s evidence to suggest that when firms confirm an earnings date materially early relative to history, abnormally positive returns are seen. Of course, that is in the aggregate, and for EOG, it’s just one piece of evidence ahead of earnings later this month.

Corporate Event Risk Calendar

Wall Street Horizon

EOG’s Q4 earnings date confirmation came 2.4 standard deviations to the early side of the historical trend.

EOG Earnings Date Confirmation History: Bullish Early Confirmation

Wall Street Horizon

The Technical Take

EOG continues to hold important support in the $117 to $121 range. Notice in the chart below that shares have a large amount of volume by price in the high $110s and low $120s which cushions declines. Also, that is where the rising 200-day moving average comes into play. While the 50-day moving average has turned down, EOG jumped on Friday to its best close of the month.

I see resistance near $138 with an ultimate test being at the all-time highs in the $148 to $151 range. Long here with a stop under $115 is a good play.

EOG: Holding the 200-day Moving Average Line

Stockcharts,com

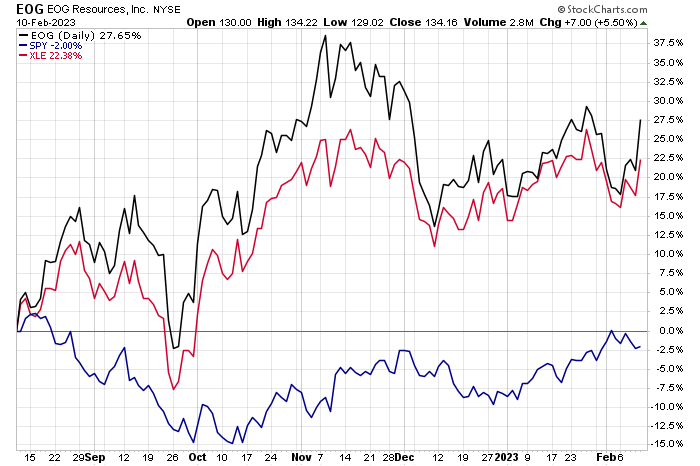

What I also like is EOG’s relative strength. Shares have outperformed both the sector ETF (XLE) and the broad market over the last six months.

EOG: Relative Strength

Stockcharts.com

The Bottom Line

With positive technicals, a compelling valuation, decent yield and free cash flow, and an abnormally positive early earnings confirmation date, I see more upside in the cards for EOG.

Be the first to comment