oonal/iStock via Getty Images

We have previously covered Enphase Energy (NASDAQ:ENPH) here as a post-FQ3’22-earnings article in November 2022. Its market opportunities in the US and the EU were discussed extensively, providing massive tailwinds to its booking growth through Q1’23, despite the rising inflationary pressures. However, its overly rich premium was discussed then, suggesting massive volatility in the short term, attributed to the uncertain macroeconomic outlook.

For this article, we will be focusing on ENPH’s significant stock declines, due to the declining oil/gas prices and supply glut contributing to plunging polysilicon prices. We reckon that the moderation is not over yet, since the Fed’s battle for a 2% target rate will likely continue through 2024, suggesting prolonged interest rate pain in the short term. While the Inflation Reduction Act (IRA) may offer solar subsidies, tightened discretionary spending may impact the company’s top line over the next few quarters.

The Renewable Investment Thesis Is Less Convincing In The Face Of Recession

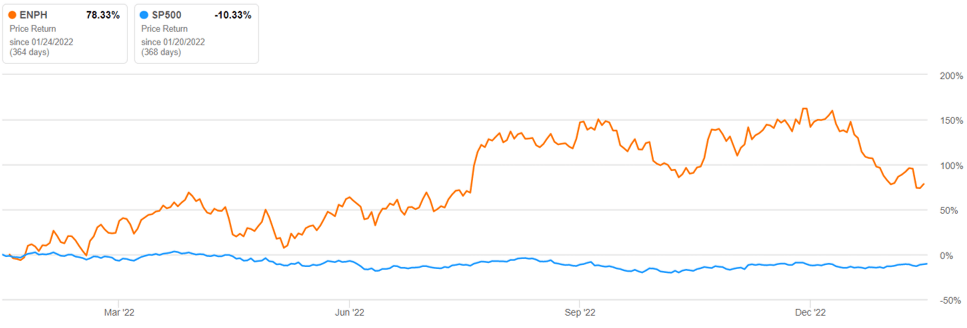

ENPH 1Y Stock Price

Seeking Alpha

ENPH has unfortunately tumbled hard by -38.12% since hitting the peak of $339.92 in December 2022, a situation reminiscent of high-growth tech stocks in November 2021. At that time, even the king of FAANG stocks, Apple (AAPL) plunged by -24.5% in the months after, suggesting Mr. Market’s efforts for moderation after the hyper-inflated pandemic highs.

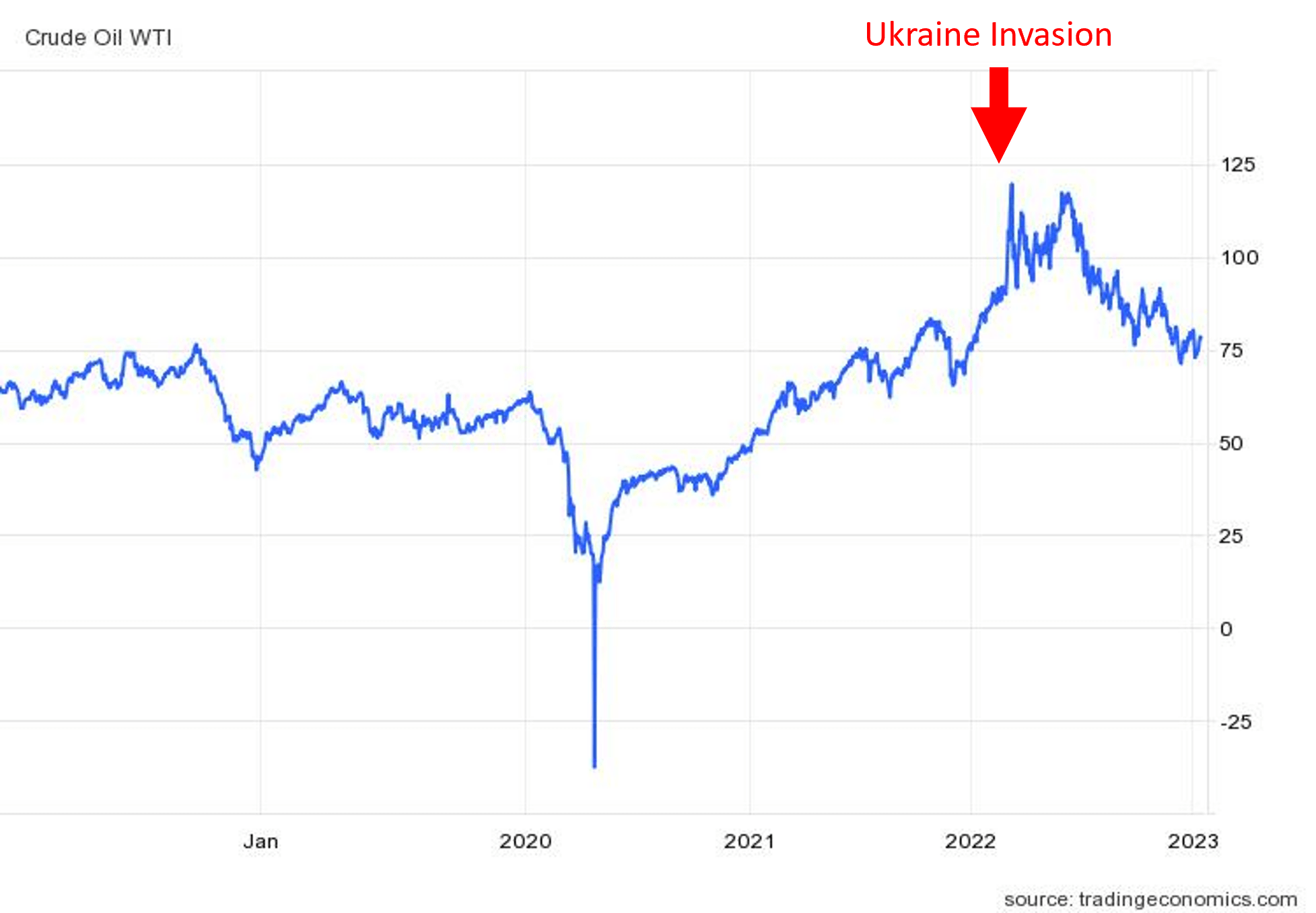

Declining Crude Oil WTI Spot Prices

Trading Economics

Does this mean that ENPH may further decline in the coming months? Maybe, maybe not. No one knows for sure. One thing is for sure, crude oil WTI prices have moderated drastically by -31.5% to $80.36 at the time of writing, nearer to their pre-pandemic levels of $65.

These numbers matter, since the demand for renewable products also rose drastically, with the Ukraine invasion triggering a massive rally in oil/gas prices in February 2022. With Russian oil accounting for up to 10% of global oil production, it is no wonder that many countries had to scramble for alternative oil sources/renewable energy then.

The situation was especially worsened after the G7 moved to cap Russian oil prices at $60, triggering a Russian production cut from 2023, potentially putting a floor on the declining prices. It remains to be seen how crude oil prices will evolve over the next few months, since we expect more support tests ahead, with the G7 also looking to cap Russian oil product prices from February 2023 onwards.

It makes sense that market optimism towards renewable stocks, like ENPH, has moderated as oil/gas prices normalize closer to pre-pandemic levels. While the EU may have temporarily turned to coal for energy security, we reckon that governments may eventually return to oil/gas, due to the latter’s improved availability and moderated prices from 2024 onwards.

Therefore, it is not surprising that the race towards carbon neutrality may also decelerate in the short term, attributed to rising inflation, growing recessionary fears, and improved energy sentiments.

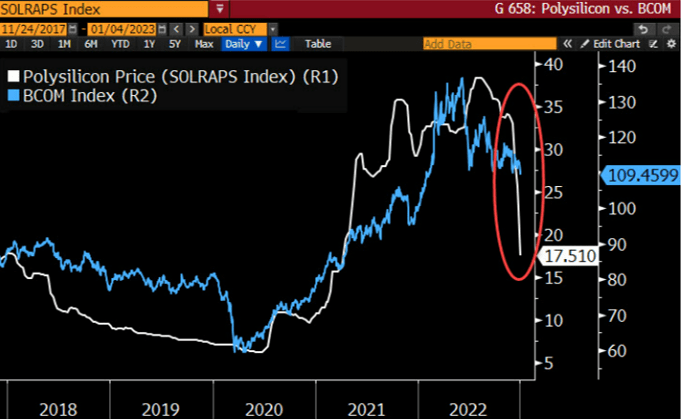

Declining Polysilicon Spot Prices

PV Magazine & BloombergNEF

Unfortunately, polysilicon prices have similarly plunged by -54.3% from $38.32/kg in August 2022 to $17.51/kg by 04 January 2023, against the pre-pandemic prices of $15/kg. Demand had soared by early 2021, leading to the rally in polysilicon prices then. However, many manufacturers also committed to an immense expansion in production output, potentially leading to a supply glut by 2024.

Multiple Chinese producers, such as Tongwei, GCL Technology (OTCPK:GCPEF), and Daqo New Energy (DQ) guided the total output of 970 MT by 2023, growing tremendously by 339.1% from the 286 MT produced in 2021. Combined with other global producers, market analysts already project over 3.8M MT of polysilicon supply by the end of 2024, compared to the 1.2M MT produced in 2022.

With massive supply flooding the market then, it is natural that we would see polysilicon prices moderate from their previous peak. DQ similarly projected a further decline in polysilicon spot prices to $10/kg by 2024, with the company guiding production costs of $4.5/kg then.

This sentiment similarly impacted ENPH’s valuations, due to the latter’s massive exposure to the photovoltaic supply chain. California’s decision in reducing the solar rebate to homeowners with solar panels has also impacted market sentiments, due to the potential slowdown in future home installations. In the short term, photovoltaic production in the US remains gated by the designed manufacturing output as well.

While the IRA has also boosted the Capex investments toward capacity expansions, the construction may only commence in 2023, with production beginning by 2025. In the long term, we may see a constructive return for renewable stocks, since the US is set to pour an eye-popping $385B into the domestic renewable sector over the next ten years, with planned expansions of approximately 550 GW for combined solar, wind, and energy storage capacities by 2030. Thereby, ambitiously expanding the renewables share from 23.2% to 50% by 2030, nearer to Biden’s highly ambitious plan of 80%.

The EU proved highly aggressive towards this trend as well, with 1 TW of solar installations planned by the end of the decade, with renewables share growing to 40% by 2030 against 22.2% in 2021. We think these massive tailwinds may trigger ENPH’s sustainable rally through the end of the decade, once the macroeconomic environment improves and market sentiments lift. The robust demand in the US and EU may also support its premium valuations, since 71.1% of its revenues remain concentrated in the US, with demand in the EU growing tremendously by 70% QoQ/136% YoY in the latest quarter.

So, Is ENPH Stock A Buy, Sell, Or Hold?

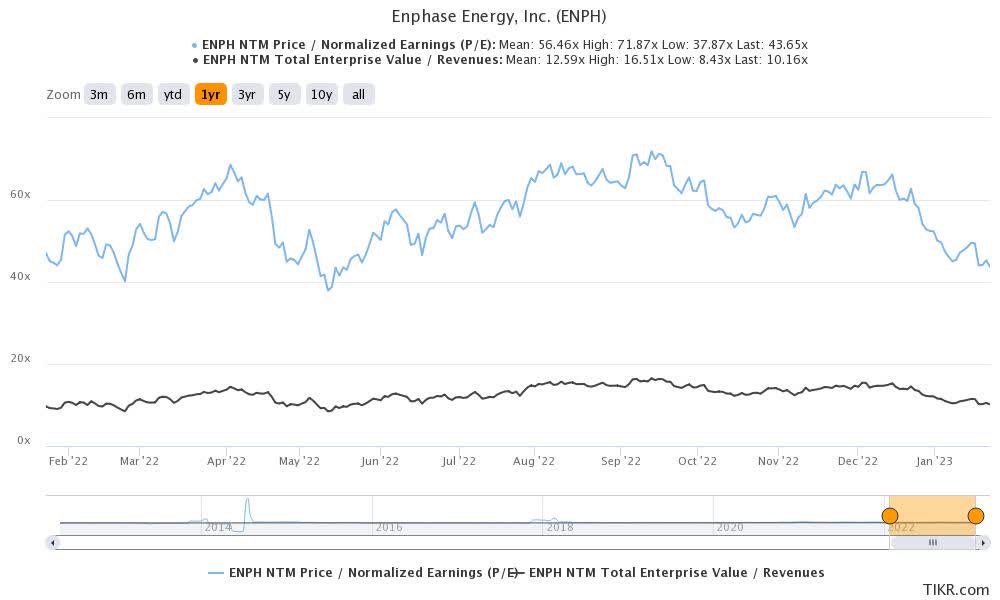

ENPH 1Y EV/Revenue and P/E Valuations

S&P Capital IQ

ENPH is currently trading at an NTM P/E of 43.65x, higher than its pre-pandemic mean of 26.66x, though lower than its 1Y mean of 56.46x. Mr. Market appears keen on moderating the stock’s premium, seeing that it has been inflated over the past few years by the hyper-pandemic hype, record high oil/gas prices, and massive renewable movement.

While it is unknown how things will develop moving forward, we remain convinced that ENPH’s forward execution will remain stellar and, therefore, justify a certain premium. Market analysts expect the company to record an excellent revenue CAGR of 36.8% and an EPS CAGR of 36.2% through FY2025. Its EBIT/net income/Free Cash Flow margins may also expand by 7.3/4.9/3.6 percentage points to 23.8%/24.8%/23.5% by FY2025, suggesting its potentially improved balance sheet and book value then.

Naturally, the question arises, how much should the premium be? There is no clear answer indeed, though we reckon that the 30x multiple may present an improved margin of safety, similar to the ENPH stock’s pre-pandemic heights. At those levels, we are looking at a moderate price target of $248.70, based on the projected FY2025 EPS of $8.29. Unfortunately, this number also suggests that there may be minimal upside potential from current levels.

We reckon that there may be more volatility in the short term as well, since the Fed’s recent meeting minutes suggest prolonged interest rate-related pains through 2023, before a pivot from 2024 onwards. Therefore, ENPH’s topline growth may be temporarily impacted by tightened discretionary spending over the next few quarters, especially for big-ticket items such as roof solar/energy storage/home EV charging installations, before picking up by H2’24.

Therefore, we prefer to continue rating the ENPH stock as a Hold here, since we think the moderation is likely not over yet. On the other hand, conservative investors looking to preserve some gains may consider selling part of their holdings and getting in again below $200.

Be the first to comment