Aliaksandr Litviniuk

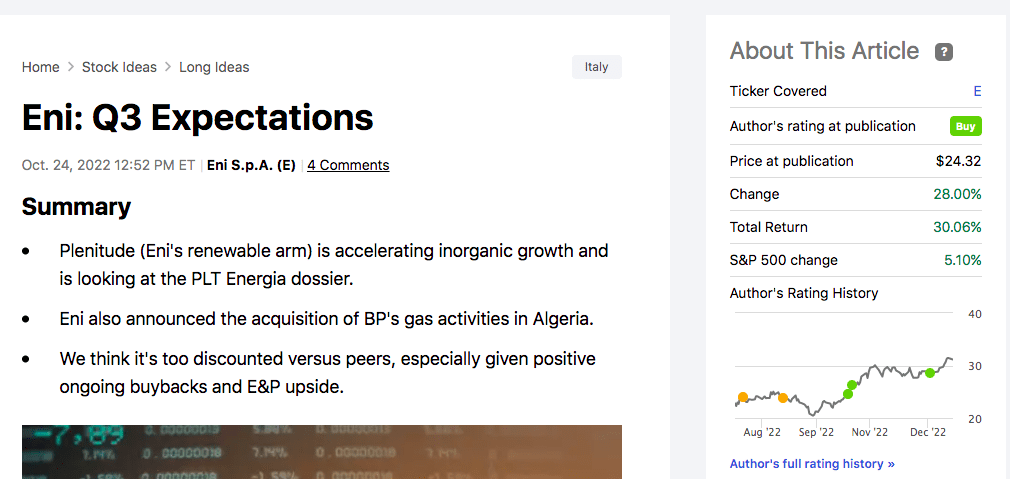

In 2022, we initiated Eni‘s coverage (NYSE:E) with a neutral rating, and then, when we understood that political risks were priced in, our internal team decided to overweight the major oil player. As a reminder, in September, it was election time in Italy, and being that the government is the main shareholder with an equity stake of 30.59%, we decided to take a ‘wait-and-see‘ approach. Our patience paid off and since then, the company is up by more than 30% compared to the S&P 500’s return of just 5%. To sum up, our investment case recap was based on: 1) years of underinvestment in oil which supported Eni with double income generation: its internal exploration division and Saipem new contracts; 2) the company’s ongoing buyback and its tasty dividend yield; 3) almost no debt; and for the long-run 4) Plenitude IPO upside in a sum-of-the-parts valuation.

Mare Evidence Lab’s previous publication

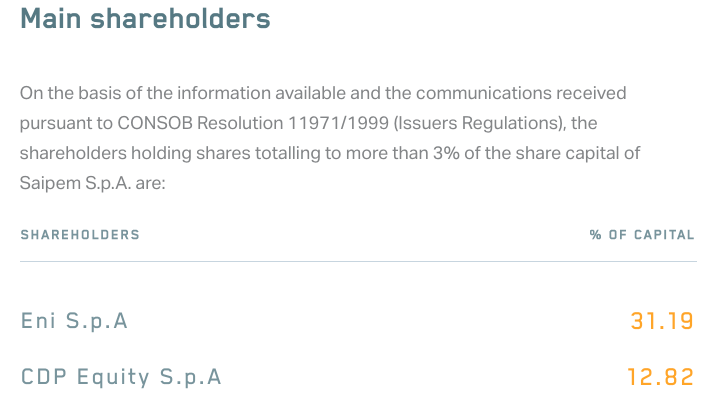

In our first analysis, we explained how Saipem was not a fairy tale; however, related to our point 1), there is now a full potential for a record year. According to our estimates, Saipem’s order backlog “could reach €9.2 billion compared to an average of the period 2017-21 of less than €4 billion” with new contracts at a double-digit margin level. Eni participated in the company’s capital increase with almost €500 million for a 31.19% stake, and now Saipem equity value stands at €2.44 billion.

Saipem’s main shareholders

Source: Saipem Corporate Website

Aside from the financial consideration, and to move on with our key takeaways, the latest oil discovery in Guyana could require a new Floating Production Storage and Offloading facility (FPSO) which in jargon is a platform used for oil production and storage. Last week, at Goldman Sachs Global Energy conference, Hess’s CEO announced that the Fangtooth oil discovery could be large enough to require a new rig. As a memo, Hess is part of the consortium led by Exxon Mobil Corp that confirmed plans for six production vessels floating which will lead to an output of 1.2 million barrels a day by 2027. Currently, Guyana has two operating platforms producing more than 360k barrels per day, while a third production vessel is almost completed and is expected to start draining oil over 2023 end. The company’s assets in Guyana and the Bakken Shale Basin in the United States will account for 80% of the company’s $3.7 billion in investments planned for this year. In addition, looking at the CEO presentation, oil production from the Guyana site is likely to more than double by 2027. Here at the Lab, we believe that this could be good news for Saipem, which has been awarded all the contracts for Exxon, the last one (UARU oil field located in the Stabroek block) was announced last December 15th and is already implied in our future estimates. If awarded, it should represent another high-margin contract that could take Saipem’s Offshore E&C backlog to record levels in 2023 and fully support Mare Evidence’s lab thesis.

This week was marked by another important discovery near Egypt. The new gas field is close to the Nargis-1 exploration site in the eastern Mediterranean Sea. More important to report is the fact that Eni might leverage its infrastructure’s proximity and confirms the effectiveness of Eni’s strategy with a focus on the Egyptian offshore. Discovery details were not provided, but in December 2022, Welligence Energy Analytics indicated that the gas field could be worth for 3.5 TCF (100 billion cubic meters). If the Welligence numbers are confirmed, we believe that could be equal to a few hundred million dollars for Eni.

Currently, the Italian company is the main producer in Egypt with a hydrocarbon output of around 350k barrels per day considering the fact that the region is now a hot spot following the discovery of the Zohr field in 2015. As a reminder, Eni produces approximately 60% of the North African country’s total gas production and also operates the LNG export facility of Damietta for a value of five million tons per year.

Conclusion and Valuation

For the above reasons, we decided to maintain our buy rating and the target price of €16 per share. Despite the recent stock price appreciation, Eni is still trading at a 4x P/E compared to the sector average of 7x with a dividend yield of 6.1% versus the sector average at 4.7%.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Be the first to comment