zentilia/iStock via Getty Images

Shares of Wind Turbine Installation Vessel (“WTIV”) owner Eneti (NYSE:NETI) are down by more than 55% since I initiated coverage of the company almost two years ago.

At that time, the company was still operating as “Scorpio Bulkers” and in the process of selling its entire dry bulk carrier fleet right before the Baltic Dry Bulk Index (“BDI”) rallied to new multi-year highs after languishing for more than a decade.

In late 2020, I was hopeful of market participants discovering the company as the next red hot ESG play after the eagerly anticipated announcement of its first newbuild WTIV order but things haven’t played out as expected by me.

Last year, the company surprisingly announced the acquisition of Seajacks International Limited (“Seajacks”) “to become the world’s leading owner and operator of wind turbine installation vessels“.

The transaction not only diluted existing Eneti equityholders quite meaningfully while at the same time triggering a whopping $30 million in bonus payments to senior management but also weakened the company’s balance sheet substantially.

With most of the company’s cash having been spent on the Seajacks acquisition, a number of assumed short- and medium-term debt maturities and management’s stated intent to exercise the option for the construction of a second newbuild WTIV at a price of $326 million, Eneti apparently recognized the need of raising additional capital.

The announcement clearly caught market participants flat-footed as it took the underwriters a number of days to line up investors but the transaction with gross proceeds of $175 million still priced deeply in the hole and actually failed to raise the targeted amount of $200 million despite insiders and related parties purchasing more than 20% of the new shares.

In recent months, Eneti managed to secure additional work for its WTIV fleet, successfully closed on a new $175 million credit facility and repaid more than $100 million in Seajacks-related debt.

In addition, the company decided not to move forward with plans to construct a Jones Act-compliant vessel due to the perceived likelihood of international WTIVs being required to meet strong demand in the U.S. market expected for 2024 and beyond.

Last month, Eneti reported highly profitable second-quarter results but revenues and profitability were boosted by a number of extraordinary gains:

- Further, substantial appreciation of the company’s stake in Scorpio Tankers which the company sold subsequent to quarter end for gross proceeds of $83.3 million.

- Compensation for contract commencement delays for the WTIV Zaratan.

- Receipt of payments for claims related to projects completed last year.

- Higher reimbursable costs (mostly fuel).

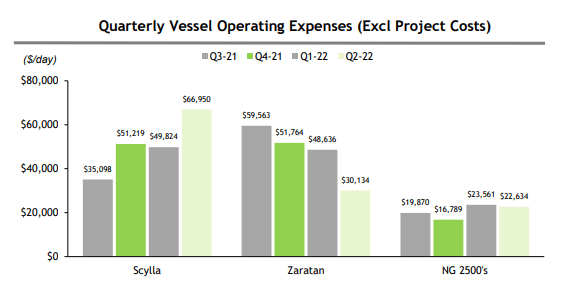

In contrast, daily operating expenses for the company’s largest WTIV, Scylla, increased by an eye-catching 35% sequentially to a new all-time high of $66,950 “due to higher COVID-related crewing and travel costs as well as fuel costs” as stated by management on the conference call.

Company Presentation

Third-quarter results should again show decent headline numbers as more Zaratan-related compensation will be recorded.

In addition, the gain from the recent sale of the company’s stake in Scorpio Tankers should add further to the bottom line.

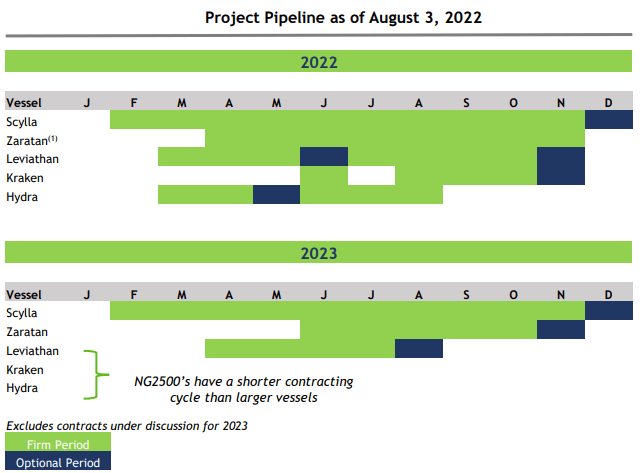

That said, Q4 and particularly Q1/2023 should be substantially weaker as the entire fleet is likely to sit idle in December and January and only Scylla having been contracted for work in Q1 so far.

Company Presentation

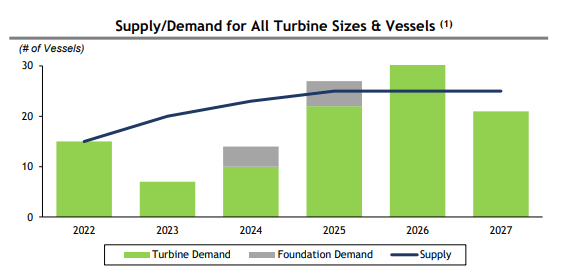

But Eneti’s story isn’t really tied to the legacy Seajacks fleet as the company is scheduled to take delivery of two newbuild, large-scale WTIVs in late 2024 and early 2025, respectively, with the first contract announcement expected by next year at the latest point.

The timing of the newbuild deliveries looks great as demand for the larger vessel classes is expected to outpace supply by 2025:

Company Presentation

On the conference call, management was quick to dismiss analysts’ concerns regarding the financial viability of the shipyard and resulting potential delays:

Turner Holm

(…) I wanted to check in on the newbuilds, maybe a question for Cameron here. Could you just give us an update and some color on construction progress and a little bit more on the delivery times? I guess the yard has had a few financial struggles, but kind of where are you all in terms of the newbuilds? Any color on that would be great.

Cameron Mackey

Thanks, Turner. Not much to report actually that — I’m not sure it’s fair to say the yard has had financial troubles. What they have experienced, of course, are some well-publicized labor disputes for some of their subcontractors; some uncertainty about their combination with one of their chief competitors, a business combination, but obviously, like the whole Asian shipbuilding complex, they are awash in highly profitable orders from conventional ship types like containers and tankers, so we aren’t concerned about their financial stability at all. We are much more focused on the on-time and on-budget progress of our vessels. And being highly specialized offshore vessels, they take on a certain, first of all, separation from the conventional shipbuilding docs and processes; and a higher status.

And also we are conveniently alongside and aligned with some major clients in oil and gas bespoke projects, so we feel actually quite confident in the progress, so far, the schedule and the ability of the yard to deliver these vessels as planned.

According to management, the company is making good progress on securing debt facilities for the newbuilds with current proposals offering financing for approximately 65% of the contracted prices.

A $33.0 million installment is currently scheduled for Q4 followed by an aggregate $65.5 million in Q3/2023.

At the end of July, Eneti had cash and cash equivalents of $59.8 million and approximately $86.6 million of availability under its $175 million revolving credit facility.

Adjusted for the proceeds of the Scorpio Tankers stake sale and the recent $17 million share repurchase from a legacy Seajacks owner as well as anticipated cash flows generated during the quarter, I would estimate the company’s cash balance at the end of Q3 to be at least $135 million assuming no material utilization of Eneti’s new $50 million share repurchase program.

Additional liquidity could be generated from a potential sale of Eneti’s smallest vessels Kraken, Hydra and Leviathan which have been re-classified as non-core assets. While it’s difficult to assign a certain price tag to these legacy WTIVs, I would guesstimate an aggregate sales price between $60 and $120 million.

Bottom Line

Investors can reasonably expect decent headline numbers from Eneti’s Q3 report in November due to a combination of strong fleet utilization and some meaningful, extraordinary gains. That said, Q4 and particularly Q1/2023 will be weaker and there’s still plenty of white space in the fleet employment schedule for 2023 but the company’s story isn’t really tied to the legacy Seajacks fleet anyway.

Going forward, investors should look for the following catalysts:

- Utilization of the company’s new $50 million share repurchase program

- New contracts for the legacy fleet

- Potential sale of legacy vessels Kraken, Hydra and Leviathan

- Financing announcements for Eneti’s newbuild WTIVs

- Contract announcements for the newbuild WTIVs

Granted, management has made some terrible decisions in the past, but stars might be aligning for Eneti now.

At this point, I feel much better about the company’s prospects than at the time of my coverage initiation almost two years ago.

With an estimated 65% discount to net asset value (“NAV”), Eneti’s shares continue to trade at bargain levels.

I am reiterating my “Buy” rating on the shares with a near-term price target of $10 which still represents a meaningful discount to NAV to reflect remaining uncertainties regarding the company’s legacy fleet utilization in 2024 and potential charter rates for the company’s newbuild WTIVs.

Be the first to comment