Endava plc (NYSE:DAVA) appears to have impressive expertise in taking onboard new and large clients besides offering innovative and growing technologies. The company already discussed offering biometric payments or artificial intelligence technologies that most clients may not know today. I designed a few discounted cash flow models with my own assumptions and those from other analysts, which resulted in beneficial results. Even considering certain risks from a decrease in sales growth or lack of hiring, I believe that DAVA looks undervalued.

Endava

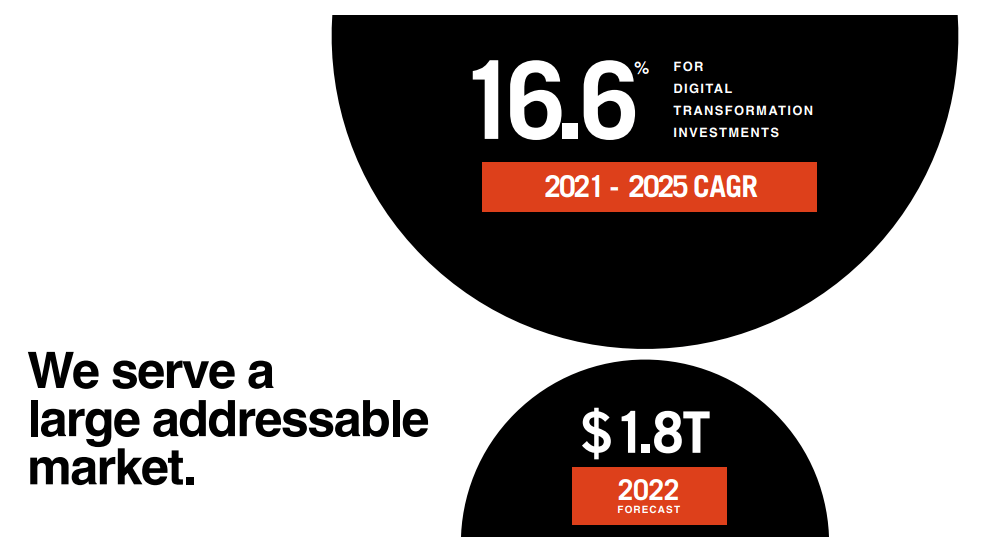

Endava offers next-generation technology services that accelerate disruption and evolution of clients. The company’s numbers are quite impressive. DAVA targets an addressable market of $1.8 trillion, which could be growing at a CAGR of 16.6% from 2021 to 2025.

Source: Investor Presentation

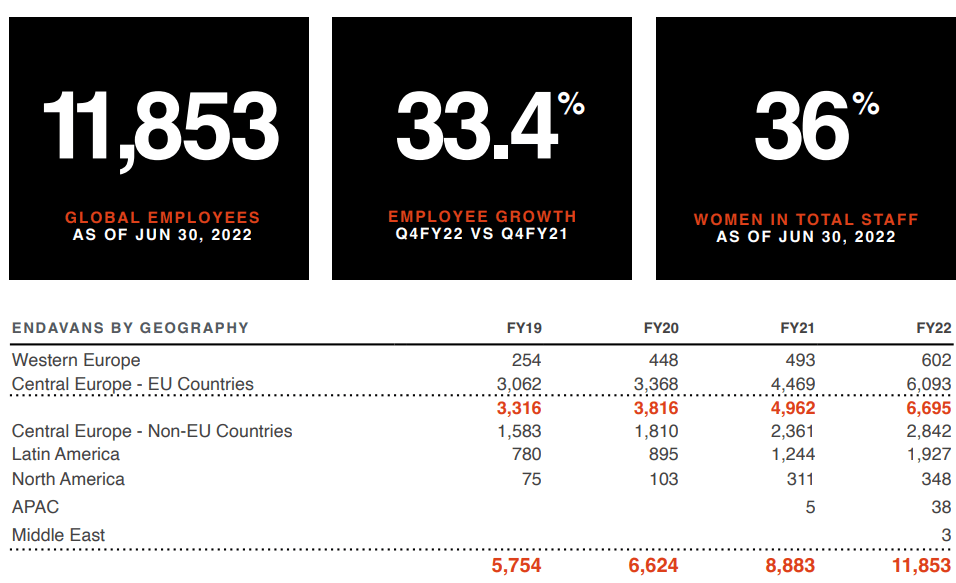

With employee growth close to 33% and more than 11k employees, the group is present all over the world. With significant acceleration in America, the increase in headcount since 2019 is simply quite impressive. Have a look at some of the company’s numbers:

Source: Investor Presentation

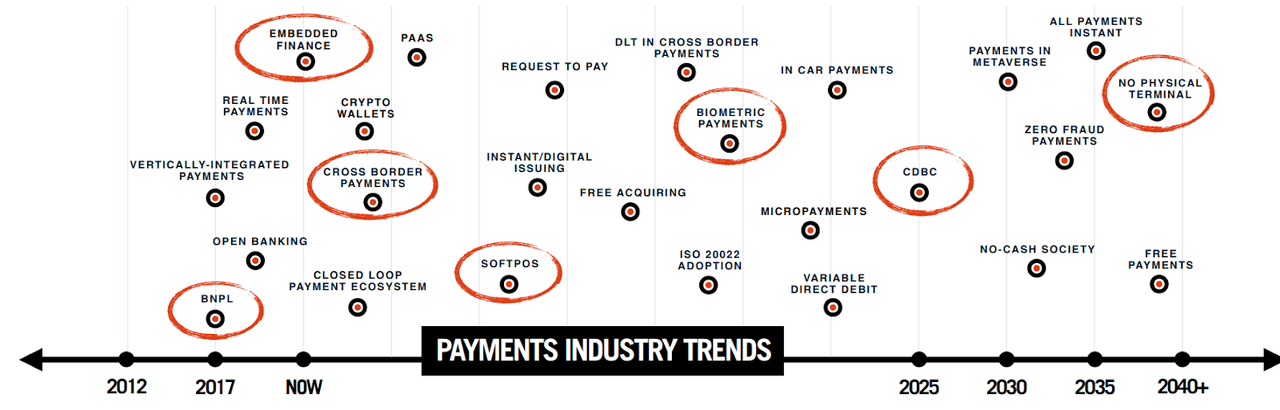

I couldn’t cover all the technologies offered by Endava, but I could see that management mainly thinks about what’s coming. In a recent presentation, DAVA noted many new technologies around the payment industry. DAVA is already thinking about biometric payments, zero fraud payments, and a no-cash society.

Source: Investor Presentation

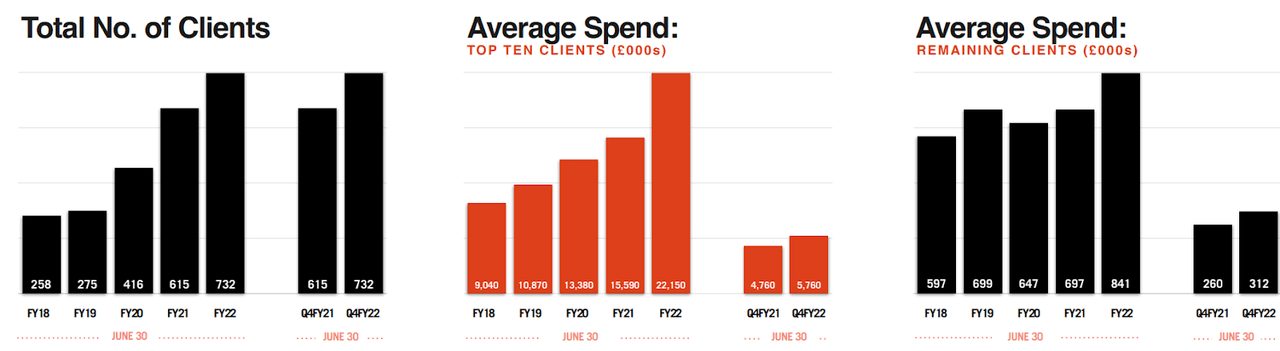

Considering the new technological ideas that Endava presents to clients, the company’s numbers make a bit more sense. The number of clients increased from 258 in 2018 to 732 in 2022 with increases in the average that clients spend.

Source: Investor Presentation

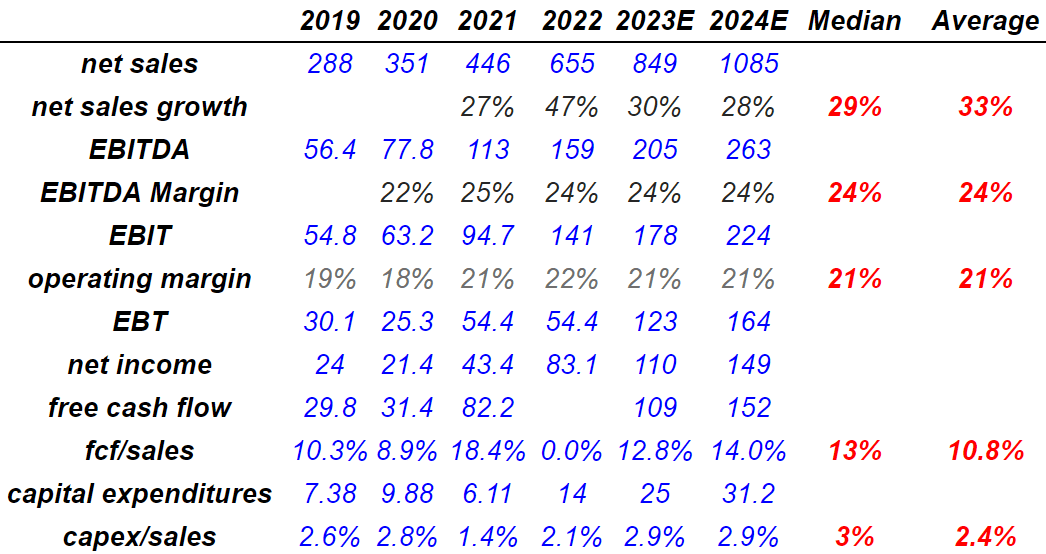

Expectations From Financial Analysts Include 29% Sales Growth And 24% EBITDA Margin

I believe that market expectations are very beneficial. In my opinion, readers should have a look at market estimates before seeing my expectations. According to investment analysts, Endava could obtain 2024 net sales of $1 billion, and the median net sales growth could be 29%. 2024 EBITDA could also stand at $263 million with an EBITDA margin of 24%. Expectations also include 2024 EBT of $164 million, with a net income of $149 million. Finally, free cash flow could stand at close to $152 million, with a median FCF/sales of 13%.

marketscreener.com

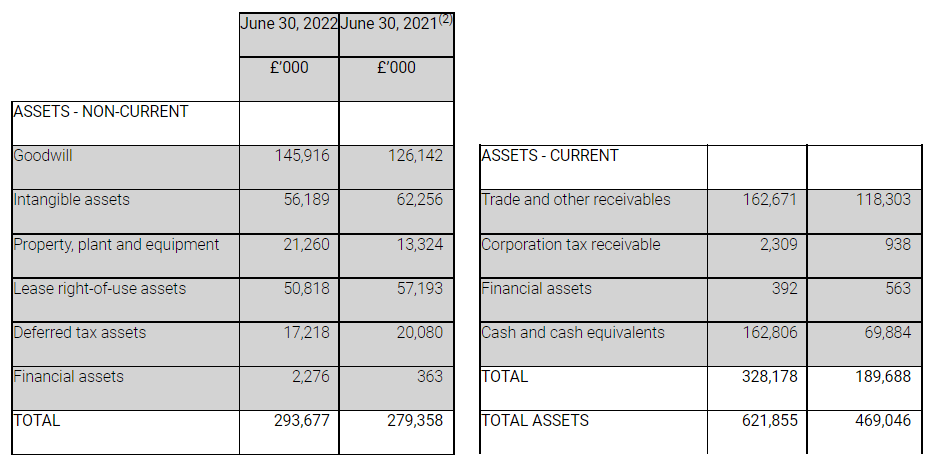

Balance Sheet

As of June 30, 2022, DAVA reports a significant amount of cash, GBP162 million, and goodwill worth GBP145 million accumulated from previous acquisitions. The asset/liability ratio is also quite healthy. In my view, the company’s financial shape would allow new acquisitions.

Source: Endava Announces Fourth Quarter Fiscal Year 2022 & Fiscal Year 2022 Results

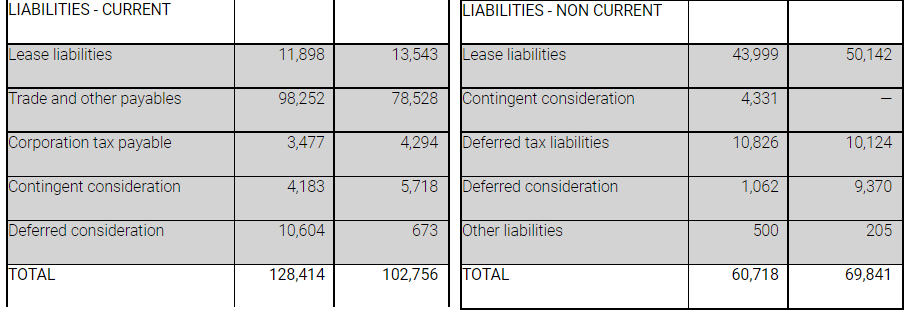

With respect to the total amount of debt, debt appears to be close to zero, and the company reports only some lease liabilities. The net debt appears to be negative. I wouldn’t worry about the company’s financial obligations.

Source: Endava Announces Fourth Quarter Fiscal Year 2022 & Fiscal Year 2022 Results

If Clients Continue To Demand Emerging Technology Trends, And More Acquisitions Take Place, I Expect A Fair Price Of $120

I believe that Endava has accumulated a lot of expertise in signing new relationships with clients. In the future, I would assume that the know-how accumulated will help management increase sales growth even more. The company did note in the last annual report that organic growth is among its domain of expertise because it knows how to offer emerging technologies:

We have a demonstrated track record of expanding our work with clients after an initial engagement. Expansion of our relationships with existing active clients will remain a key strategy going forward as we continue to leverage our deep domain expertise and knowledge of emerging technology trends in order to drive incremental growth for our business. Source: ENDAVA PLC annual report FY21

With that being said about the expertise with new clients, it is worth noting that Endava is currently involved in technological trends that may explode soon. If the company continues to focus on target markets like IoT, artificial intelligence, or augmented reality, revenue growth would likely trend north. Keep in mind that the global augmented reality market size is expected to grow at more than 31% from 2022 to 2028:

We are highly focused on remaining at the forefront of emerging technology trends, including in areas such as IoT, artificial intelligence, machine learning, augmented reality, virtual reality and blockchain. Source: ENDAVA PLC annual report FY21

According to the latest research study, the demand of global Augmented Reality Market size & share in terms of revenue was valued at USD 15.2 billion in 2021 and it is expected to surpass around USD 90.8 billion mark, by 2028, growing at a compound annual growth rate of about 31.5% during the forecast period 2022 to 2028. Source: Global Opportunities in Augmented Reality Market Size

The recent acquisition of Five and Levvel and potential M&A initiatives that DAVA could undertake are worth considering. In particular, if we include the expansion of sales presence and potential synergies from previous and new acquisitions, free cash flow growth could be substantial.

With our acquisition of Five and Levvel, we further increased our sales presence in the United States. In addition, we plan to evaluate other growth markets, including countries in the Asia Pacific region, to expand our client footprint. Source: ENDAVA PLC annual report FY21

ENDAVA PLC annual report FY21

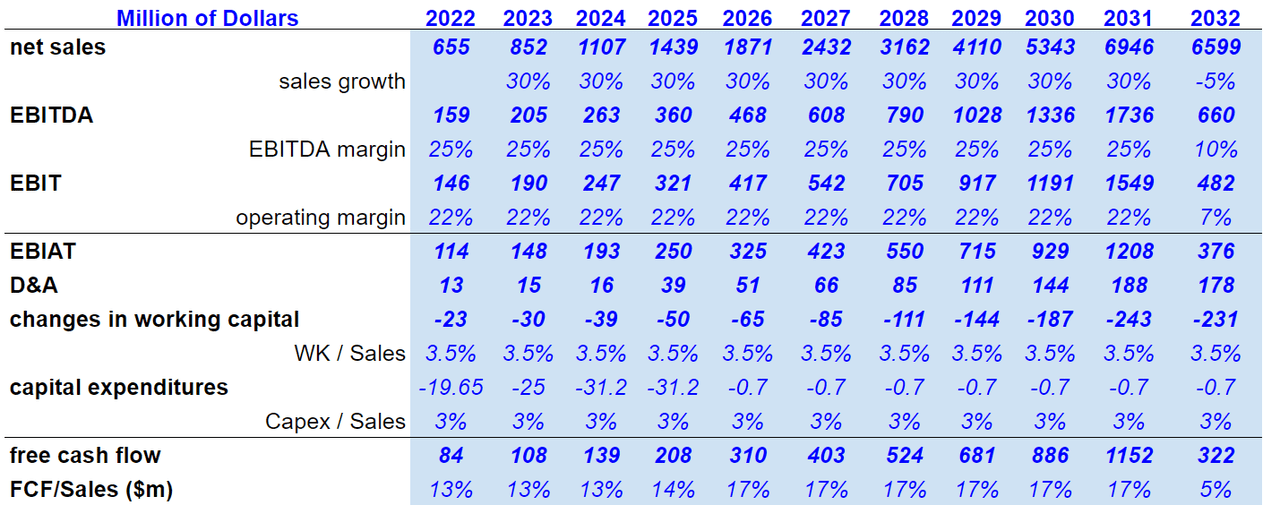

Under this case, Endava’s net sales for 2032 would be $6.5 billion, with a sales growth of -5%. I also foresee an EBITDA of $660 million, with an EBITDA margin of 10% and an operating margin of 7%. An EBIAT of $376 million could also be expected, plus D&A would be $178 million. Besides, changes in working capital would be close to $231 million along with a change in working capital/sales of 3.5%. Finally, I expected free cash flow to be $322 million, and FCF/sales to be 5%.

Author’s DCF Model

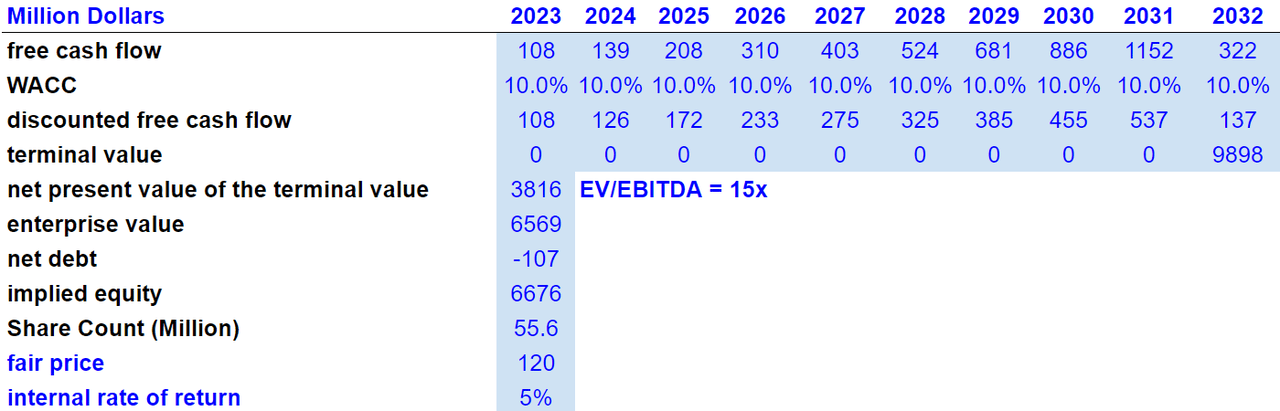

In 2032, my results include free cash flow of $322 million. With a WACC of 10%, I obtained a discounted free cash flow of $137 million in addition to a terminal value of $9.8 billion and a NPV of terminal value of $3.8 billion. I forecasted an EV of $6.569 billion and an implied equity of $6.676 billion. Finally, my results would also include a fair price of $120, plus an internal rate of return of 5%.

Author’s DCF Model

My Worst-Case Scenario Implied A Valuation Of $61 Per Share

In the last present history, DAVA reported significant sales growth, which may not continue in the future. If Endava can’t hire sufficient personnel, management finds technical difficulties, or new clients don’t show up, sales growth may slow down. As a result, I believe that certain traders may sell equity, which may increase the cost of equity. The stock price would decline.

We may not be able to sustain revenue growth consistent with our recent history or at all. You should not consider our revenue growth in recent periods as indicative of our future performance. Source: ENDAVA PLC annual report FY21

The company does not really sign long-term agreements with clients. If Endava fails to offer new technological solutions, the demand from clients could be lower. In the worst case, revenue growth would not grow as expected, and the demand for the stock would diminish. If a sufficient number of journalists notice the decline in revenue, the stock price could decline:

Our clients can terminate many of our master services agreements and work orders with or without cause, in some cases subject only to 15 days or less prior notice in the case of termination without cause. Although a substantial majority of our revenue is typically generated from clients who also contributed to our revenue during the prior year, our engagements with our clients are typically for projects that are singular in nature. Source: ENDAVA PLC annual report FY21

Endava already identified shortages in the availability of certain IT professionals. If DAVA has to pay too much to hire new personnel, or it does not hire personnel at all, the design of new products may not be that successful. Management warned about this risk in the last annual report:

Increased hiring by technology companies and increasing worldwide competition for skilled technology professionals has led to a shortage in the availability of suitable personnel in the locations where we operate and hire. Source: ENDAVA PLC annual report FY21

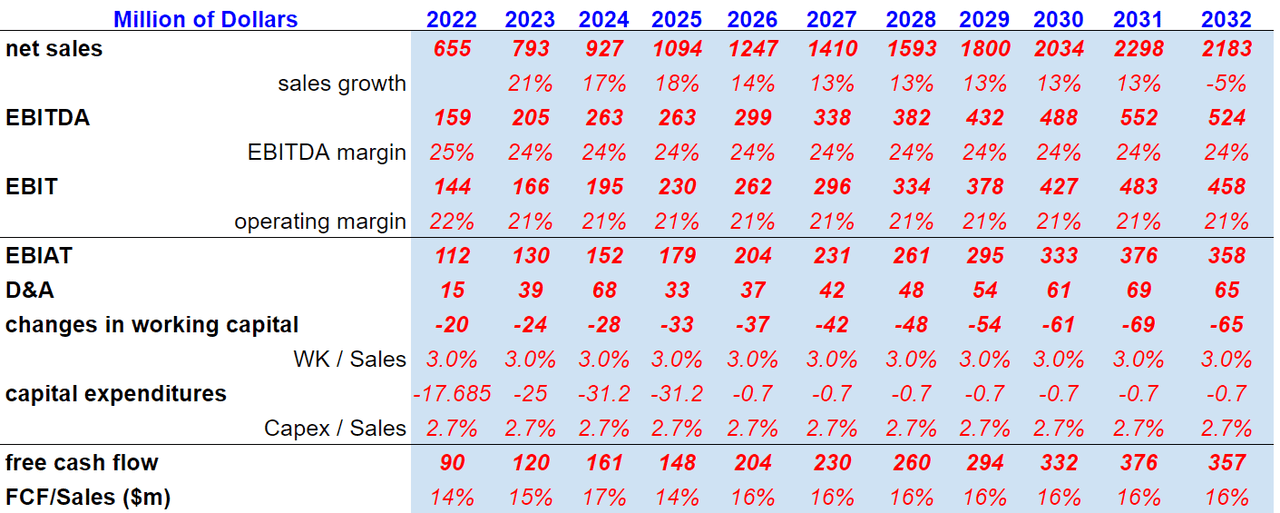

By 2032, the company could obtain net sales of $2.1 billion, with sales growth of -5%, 2032 EBITDA of $524 million, and an EBITDA margin of 24%. I also forecasted EBIT of $458 million and operating margin at 21%. Besides, my assumptions include EBIAT of $358 million, D&A of $65 million, and a change in working capital of $65 million. Finally, free cash flow would be $357 million, with an FCF/sales of 16%.

Author’s DCF Model

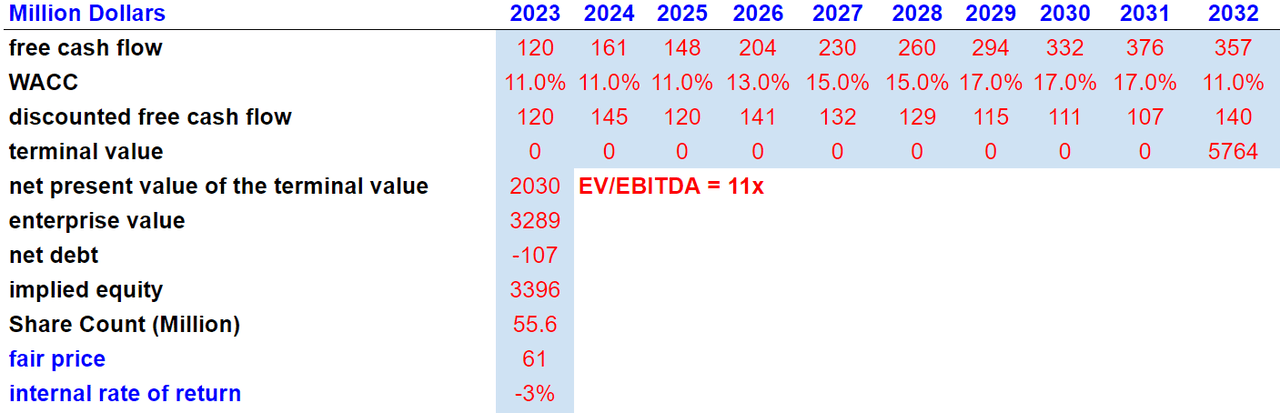

Under the previous conditions, my results included a free cash flow of $357 million, 2032 discounted free cash flow of $140 million, and a terminal value of $5.7 billion. With an EV/EBITDA of 11x, I obtained a total EV of $3.2 billion, with net debt of -$107 million and an implied equity of $3.396 billion. Under this case, the fair price stands at $61 per share with an internal rate of return of -3%.

Author’s DCF Model

My Takeaway

Endava knows how to sign services agreements with large clients, and intends to offer innovative technologies like biometric payments or artificial intelligence technologies. In my view, even if sales growth is a bit lower than expected, the company’s valuation could reach $120 with a few more acquisitions and successful closure of existing transactions. Yes, I see risks if DAVA can’t hire sufficient personnel, or sales growth diminishes. With that, my discounted cash flow models showed that there is significant upside potential in the stock valuation.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment