Hispanolistic/E+ via Getty Images

Introduction

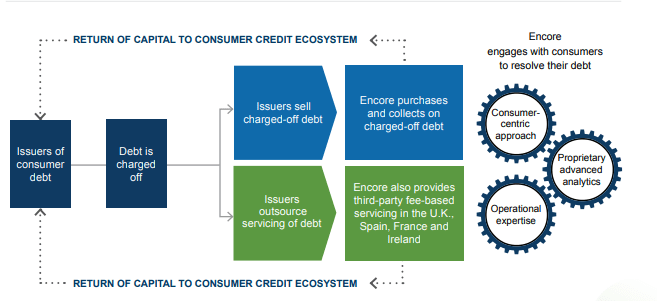

Encore Capital Group (NASDAQ:ECPG) is a consumer finance company that assists in the resolution of unpaid debts by purchasing portfolios of underperforming loans. In other words, they are a collection agency. That type of business might not be everyone’s cup of tea so understanding and accepting that is the first hurdle to learning about or potentially investing in Encore’s stock.

2021 Annual Report

Encore operates in multiple international markets in addition to the US like France, the UK, and Spain. The US operating company is Midland Credit Management and the European countries operate under the Cabot name.

The company began its journey to the public markets around a decade ago through a series of mergers and acquisitions that grew its scope and allowed the company to enter new markets.

Strategy

Their advantages claim to be their use of data and other analytical tools to improve their capital allocation, collection rates, and better utilize their scale.

For a company like this, there are two primary levers to pull. The first is on the purchasing side. Encore’s goal is to buy receivables that end up having the most amount collected as fast as possible relative to the price paid for the portfolio.

To generate these opportunities they leverage their relationships with companies and financial institutions to source new deals while using their 20 years of data and models to analyze the potential purchases.

The 2nd lever is the collection activity. Encore uses direct mail campaigns, global call centers, digital activities, and legal action through a network of retained law firms to perform their collections.

Financials

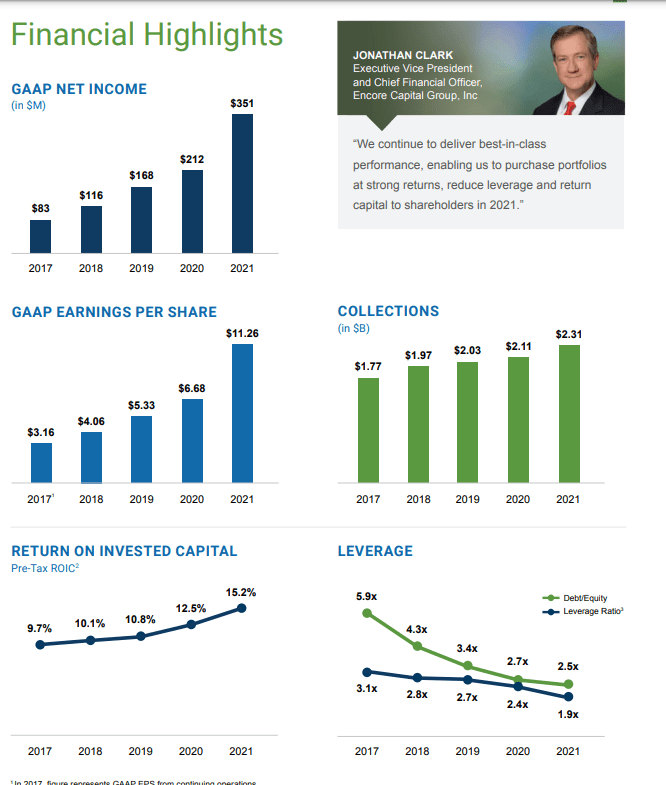

2021 was a banner year for the company, with net income and EPS jumping drastically over the previous year.

2021 Annual Report

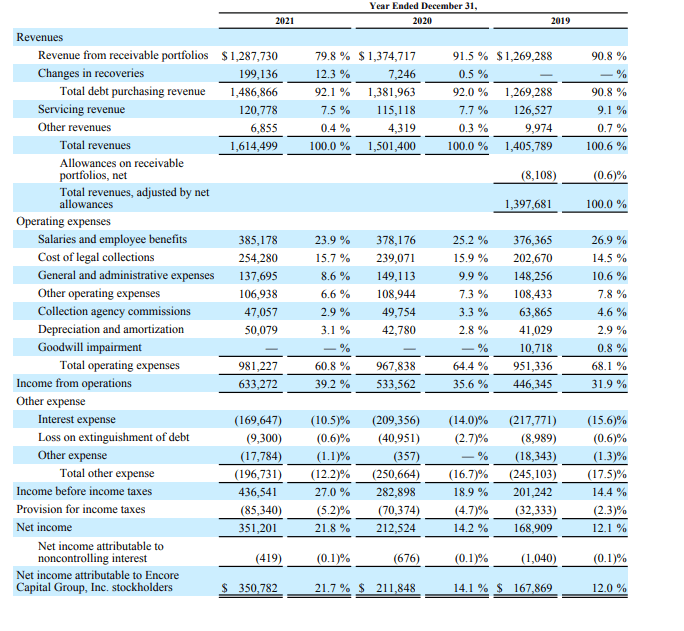

Looking deeper at a 3 year income statement, we can identify the drivers of the 2021 outperformance to see if they are sustainable or one-offs.

2021 Annual Report

The first big one is the 200k in “change in recoveries” in the revenue section.

The change in recoveries is due to collection results higher than the companies forecast and higher than previous periods which the forecast was based on. The company sighted improved execution and a change in consumer behavior due to the pandemic as the main causes of the higher recoveries.

Next, their interest expense decreased about $40k versus 2020. SG&A expenses were flat and revenue was down slightly but flat versus 2020.

The reduction in interest expense was due to refinancing and redeeming certain debt securities in 2020 and 2021 with new securities that had lower interest rates.

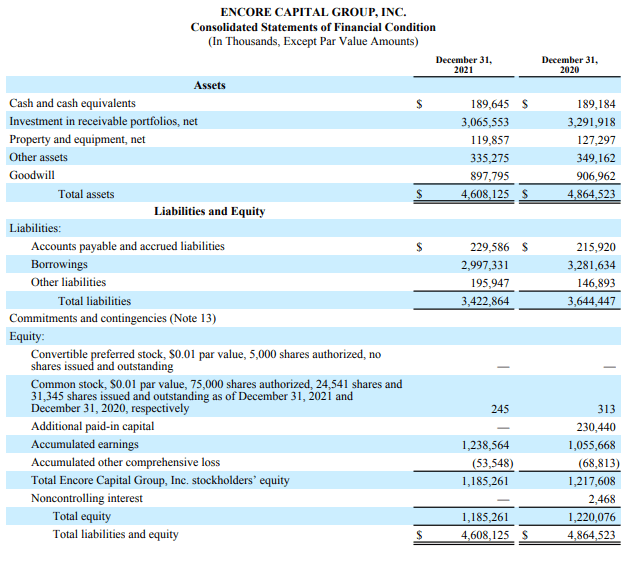

Encore’s balance sheet is mostly made up of their purchased collection portfolios and the borrowings associated with those. They have very few hard assets, a fair amount of goodwill from acquisitions, and a large amount of accumulated earnings.

balance sheet

Source: 2021 Annual Report

Positive accumulated earnings are a good sign as this means that the company has been profitable for many years. Not much else to say on the balance sheet, the company’s value continues to be reliant on how much they pay for their portfolios and how well they do collecting on those receivables.

More Recent Financials

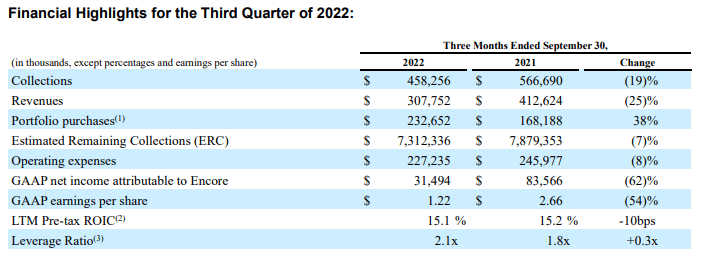

For Q3 2022, Encore’s results look a lot less rosy. Across the board, collections, revenue, and net income fell.

Q3 2022 release

Encore’s says this is due to currency effects in Europe and a shifting collection environment in the US as charge offs rise. At the same time, the company is purchasing more assets than ever as lending increases in the US.

The company believes that this higher purchasing level will result in stronger results in a couple of years, similar to how the current disappointing results are due to lower purchases and activity during 2020-2021 as the pandemic unfolded.

The question I have is how the higher price of these purchases, driven by interest rates but partially offset by lower than expected collection rates, will affect the company’s profitability and return on capital.

Q3 2022 release

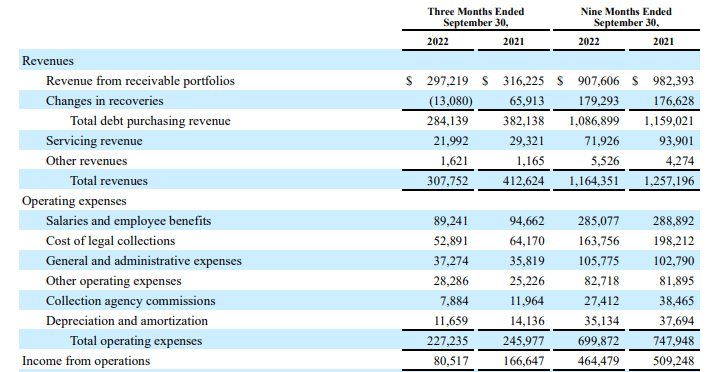

Operating income was half what it was a quarter ago, driven by lower collections revenue partially offset by slightly lower operating expenses.

Q3 2022 release

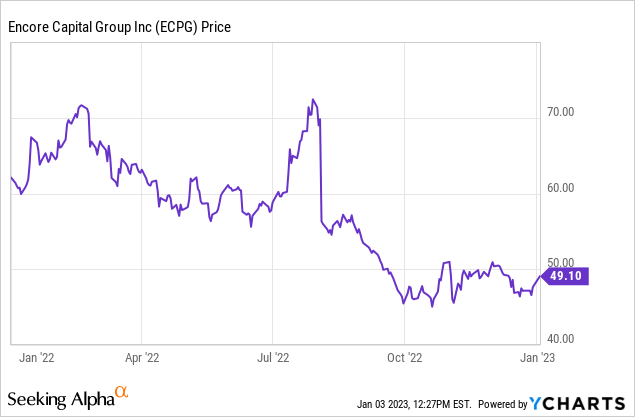

In the past year, Encore’s stock has fallen 20%, which is about what the overall S&P 500 has done as well. Given that Encore itself expects a few quarters of poorer results, one might see this as justified.

Extrapolating out current EPS to a full year, forward EPS is $4.88. That makes the forward p/e around 10x.

I would say that would be a decent bargain if I did not expect furthering worsening of Encore’s results in the near term. A recession that everyone is predicting or that we may already be in, higher interest rates, and worsening collections rates all make it seem likely that full year EPS figure will be high.

The tricky nature of using p/e as the main evaluation starting point is that both halves of the equation can move.

Conclusion

Long term I don’t see a reason to invest in Encore specifically versus another company or strategy. While they might have a little edge here or there, whether it’s in markets, technology, relationships, at the end of the day it just seems to be a small cap collection agency going into an unfavorable part of the cycle for its business model.

While the results we can see show a consistent history of profitability and the company is returning that profitability via stock buybacks, I do not think an above average collection agency is a wise place to use capital unless there is a special circumstance or an insanely cheap price, both of which I do not think are present here.

Be the first to comment