stanley45

Enbridge (NYSE:ENB) is a strong energy player in the midstream market that is seeing robust growth in adjusted EBITDA, distributable cash flow as well as dividends. The energy firm released its financial projections for FY 2023 in November which indicate sustained growth across key metrics. Enbridge’s contracted cash flows also reduce market price risks for the firm and its investors which adds to the safety of Enbridge’s dividend. The firm’s strong dividend coverage and attractive long term dividend growth are two key reasons why investors may want to buy the shares of this midstream firm!

Enbridge: A key player in the energy transportation market with a high degree of contracted cash flows

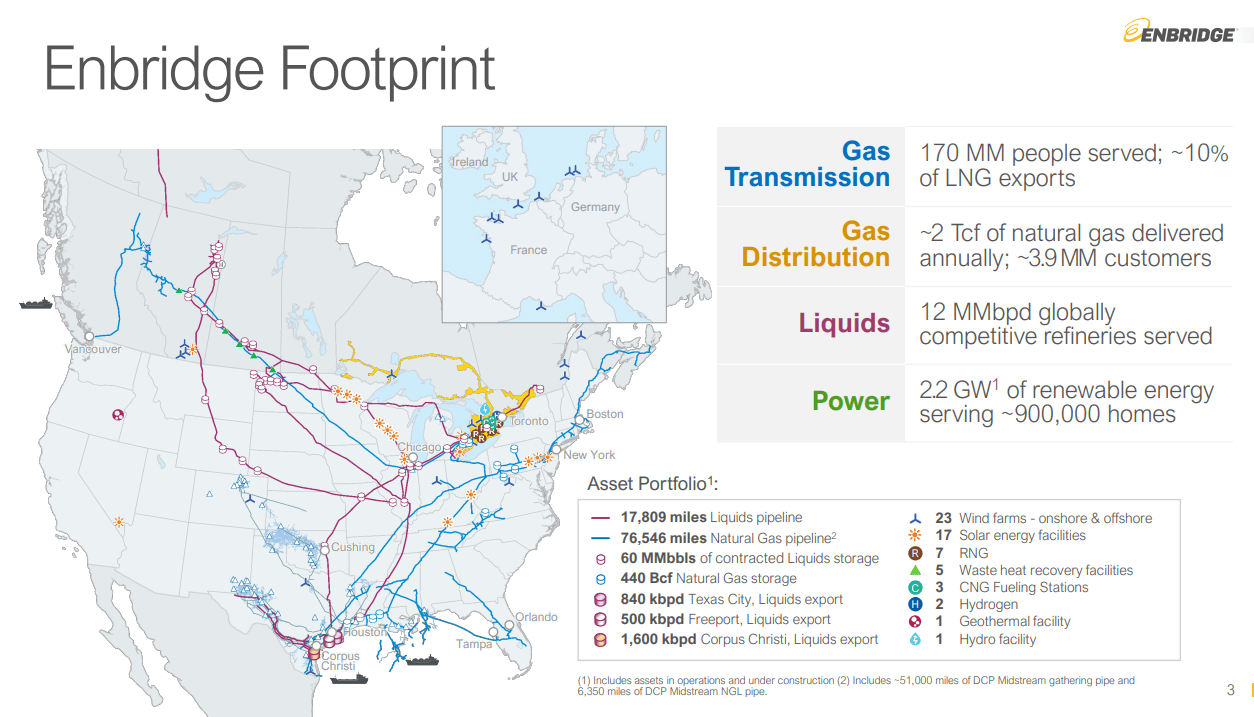

Enbridge is a Canada-based energy company with a growing and diversified asset base. The company operates 17,809 miles of liquids pipelines as well as 76,546 miles of natural gas pipelines in the US and Canada. Enbridge also owns North America’s largest natural gas utility and onshore as well as offshore windfarm assets that help diversify its core pipeline business. Enbridge transports approximately 30% of crude oil produced in the US and Canada which makes the company one of the largest energy transportation companies in the country.

Enbridge

Liquids pipelines account for about 58% of Enbridge’s FY 2022 EBITDA while gas transmission and distribution represent 38% of the firm’s EBITDA. The remaining 4% come from renewable energy.

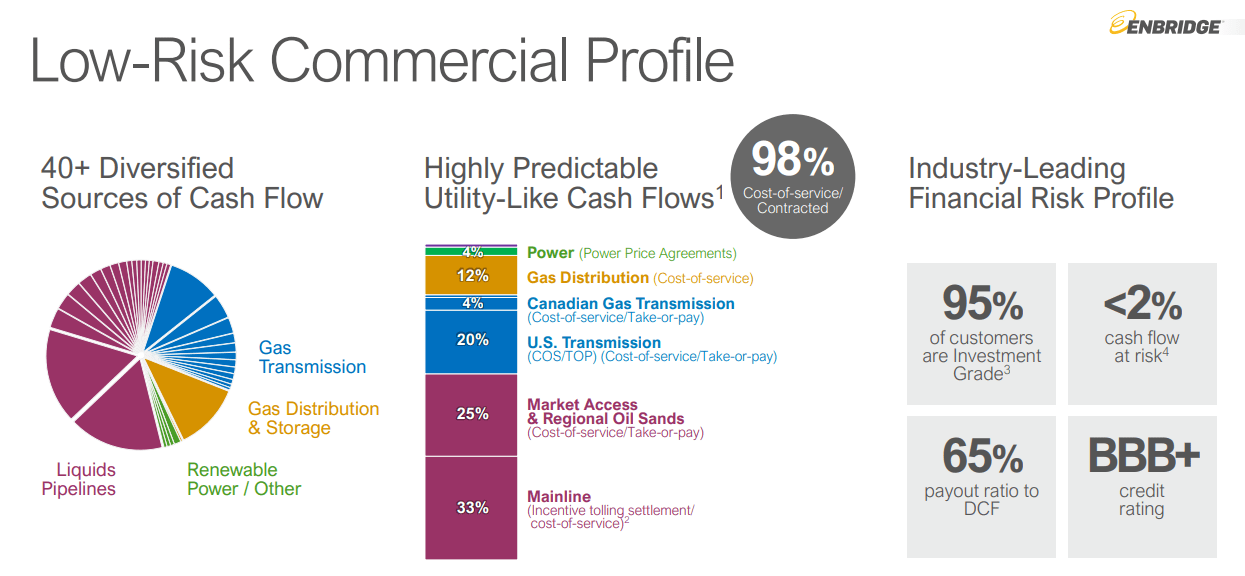

As a pipeline-focused energy company, Enbridge contracts its transportation volumes in advance which means the company offers investors highly predictable cash flows and therefore a very safe dividend. Enbridge’s cash flows across its businesses are 98% contracted which means the midstream firm has very little cash flow and market price risks.

Enbridge

Strong financial framework for FY 2023, solid DCF coverage

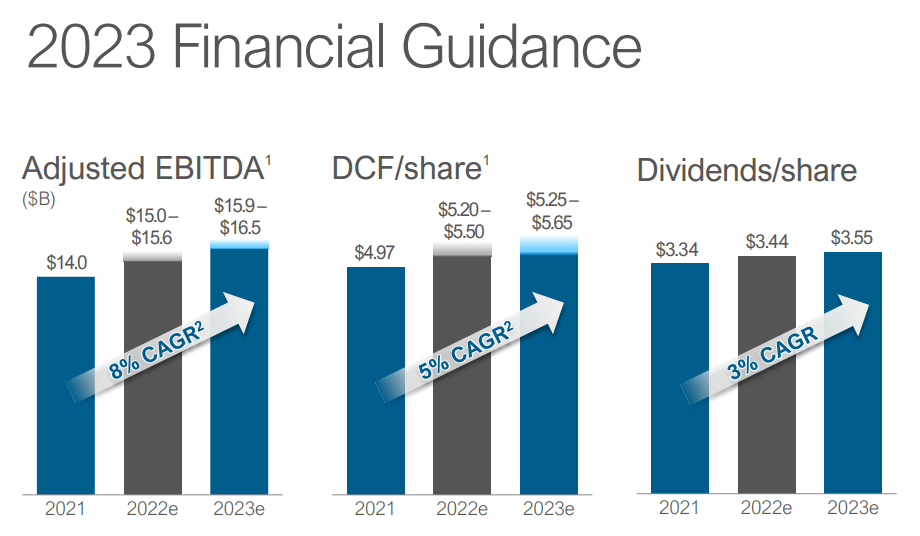

Enbridge expects continual growth across its businesses in FY 2023 as the company continues to invest in capacity expansion. The energy company released its budget plan for the current fiscal year which calls for $15.9-16.5B in adjusted EBITDA and $5.25-5.65 per-share in distributable cash flow, implying two-year compound annual growth rates of 8% and 5%.

Enbridge

With $5.25-5.65 per-share expected in distributable cash flow in FY 2023, Enbridge is looking at a DCF coverage ratio of at least 1.48 X, but in the best case, the dividend coverage ratio could be as a high as 1.59 X. In FY 2021, Enbridge’s DCF coverage ratio was 1.49 X while the FY 2022 DCF-based coverage ratio, at midpoint, is expected to be 1.56 X. From a dividend safety point of view, I believe Enbridge’s dividend is very well protected by DCF and the company has considerable room to keep growing its dividend in the future.

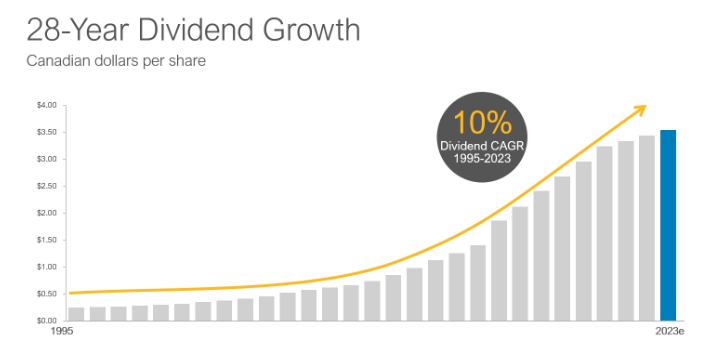

Enbridge has been a reliable dividend grower for decades. The midstream firm raised its dividend by 10% annually since 1995 (in Canadian Dollar terms) and although the dividend growth has moderated lately, dividend investors have every reason to believe that they can look forward to receiving a growing dividend stream the future.

Enbridge increased its Q1’23 dividend from $0.86 per-share to $0.8875 per-share, showing an increase of 3.2% quarter over quarter. Based off of this dividend, shares of Enbridge currently yield 6.6% for US investors.

Enbridge

Valuation of Enbridge

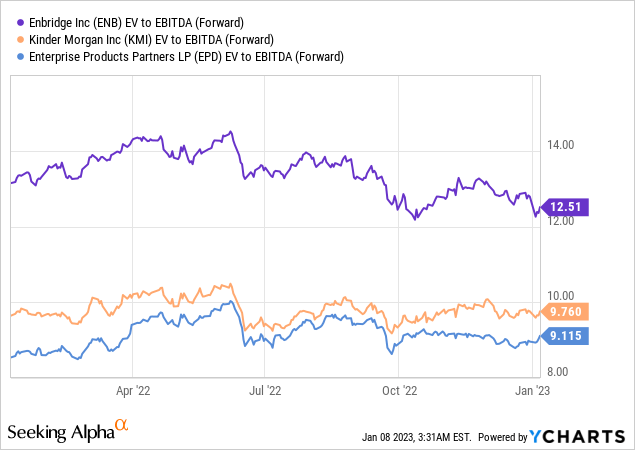

Enbridge, based off of EBITDA, is not the cheapest diversified midstream companies that investors can buy right now. Enbridge has a forward enterprise-value-to-EBITDA ratio of 12.5 X which makes it more expensive than Kinder Morgan (KMI) or Enterprise Products Partners (EPD). However, I believe, Enbridge’s ability to generate consistent dividend growth in the last couple of decades justifies paying a premium price for ENB.

Risks with Enbridge

Enbridge is a vital energy player in the US/Canada energy markets and the company transports a significant portion (30%) of North American crude oil. Despite the strong market position and extensive pipeline footprint, companies that deal with the transport of crude oil and natural gas may be subjected to more regulation going forward as governments around the world crack down on the fossil fuel industry. Any kind of fossil fuel-hostile regulation that limits Enbridge’s investment potential would likely result in lower adjusted EBITDA, distributable cash flow and dividend growth going forward.

Final thoughts

Enbridge is a solid choice for dividend investors in the midstream segment. The company has a diversified asset base, is growing its adjusted EBITDA and cash flow, and the financial framework released for FY 2023 strongly implies that the firm will continue to cover its dividend with distributable cash flow. The implied DCF coverage ratio of 1.5 X also implies that investors don’t have to worry about the sustainability of the dividend. While the valuation based off of EBITDA is not as cheap as the valuations of other midstream firms, I believe the high degree of contracted cash flows, the 6.6% dividend yield and the risk profile are very favorable!

Be the first to comment