Sleepy, boring, stocks that the market seems to have forgotten are by far my favorite stocks to discover and to buy. This has only become more true in recent years with hyper-powered social media, meme stocks, celebrity CEOs, and money managers who seem to think staying in the news headlines is a job requirement. I usually end up avoiding these types of stocks like the plague. And in my February 11th, 2021 article “There Are Bubbles Everywhere, But Cash Is Not The Place To Be, Here Are 10 Stocks To Buy Now” I went out of my way to warn investors about many of the popular market bubbles I saw at the time.

There has been a lot of talk about bubbles in the marketplace lately, and bubbles certainly exist. Overall valuations of the stock market, by many accounts, are as expensive as they have ever been. Crypto-currencies like Bitcoin (BTC-USD) have risen to uncharted territory. The IPO and SPAC market is on fire. Residential real estate set new records in 2020. Bond yields are extremely low by most measures. I don’t think any of the above statements are particularly controversial. So, I suppose we shouldn’t be surprised to see discussions of bubbles becoming more frequent in the financial media. Let’s say, for the sake of argument that all of the people claiming these markets are too expensive to invest in right now because they will produce very low or negative medium-to-long-term returns (say, over the course of 5-10 years) are right. (My nice way of saying, they are bubbles.) What should investors who wish to get a potential inflation-beating long-term CAGR from their investments do?

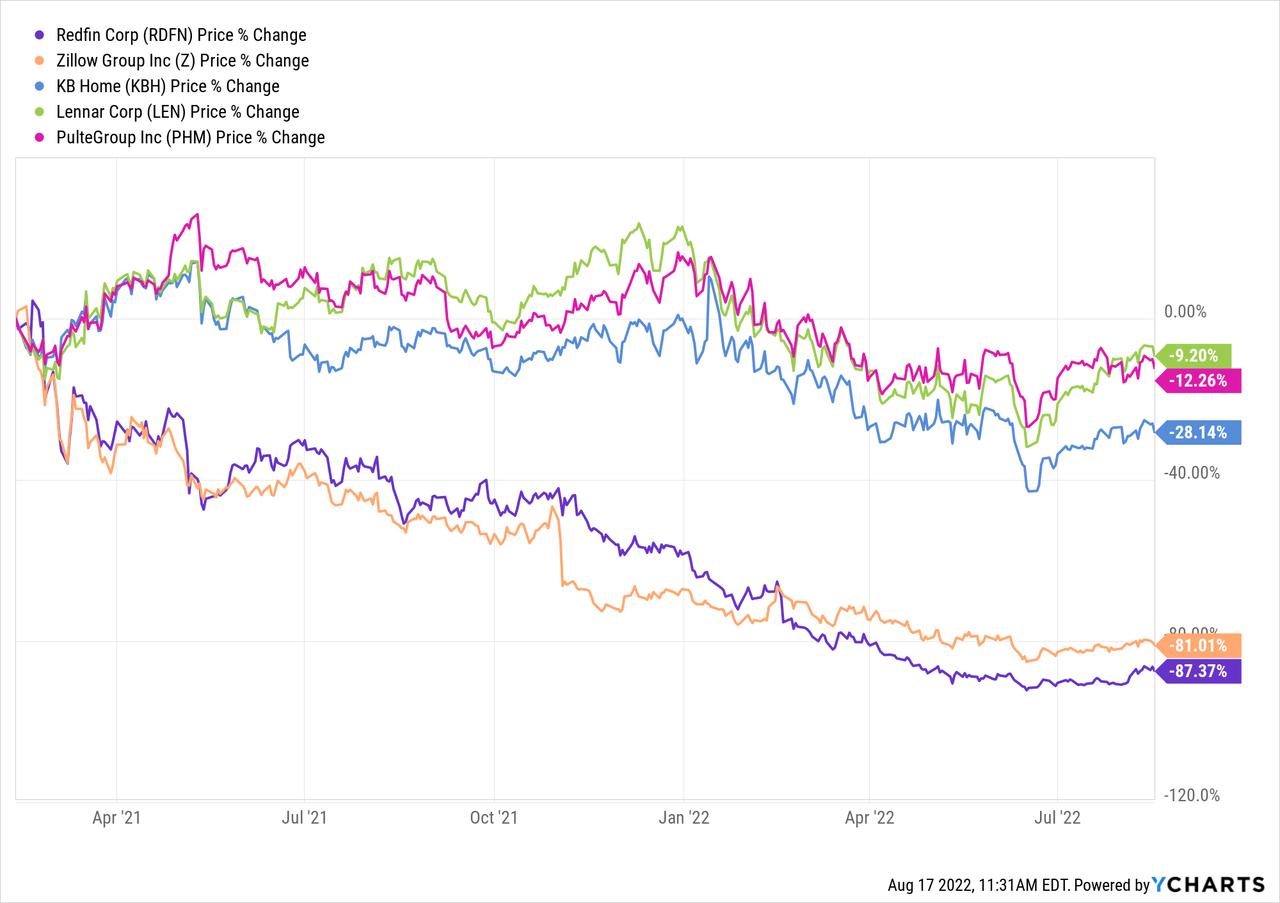

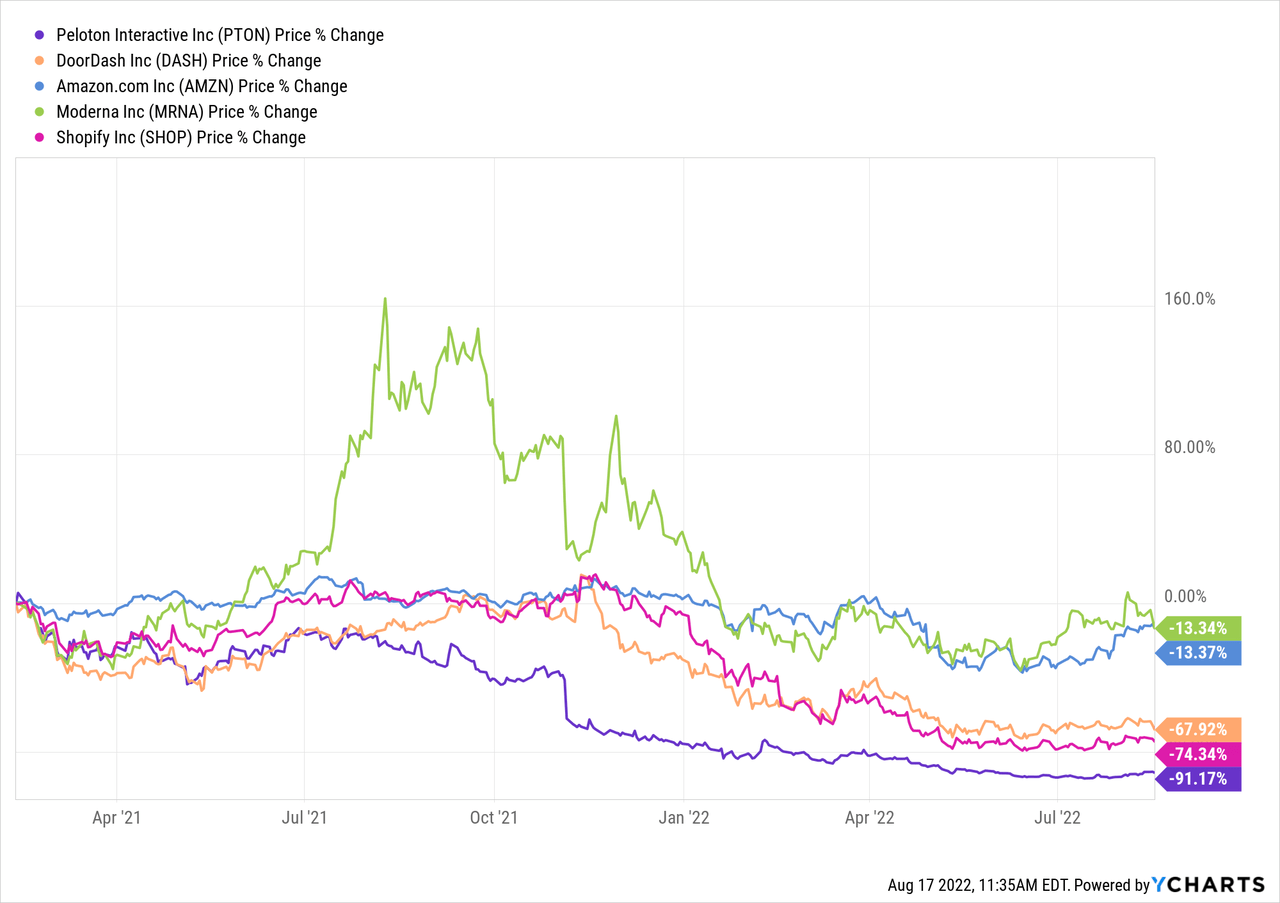

Perhaps we should first invert our thinking, and list what NOT to do if we want to achieve reasonably good long-term returns. In order to do that, we can think of things we should do if our goal is to produce poor long-term returns. If you really want to ensure you will produce poor returns over the next decade you should 1) go out and buy as many recent IPOs and SPACs as you can, 2) buy lots of crypto-currency 3) put more than 20% of your portfolio in long-duration bonds 4) buy stocks with low earnings yields 5) buy stocks with PEG ratios over 3.0, 6) buy stocks taking on massive amounts of new debt just to keep their businesses alive, 7) buy stocks who had a temporary 2-year lift from COVID and are now trading at high prices, 8) buy a new house that you don’t need just because your stock portfolio has performed well, 9) buy the stocks of businesses that have shown evidence they are being disrupted by new technology, 10) own index or mutual funds that are heavily weighted with many of the above types of stocks, and last, but not least 11) hold lots of cash because you think everything is in a bubble.

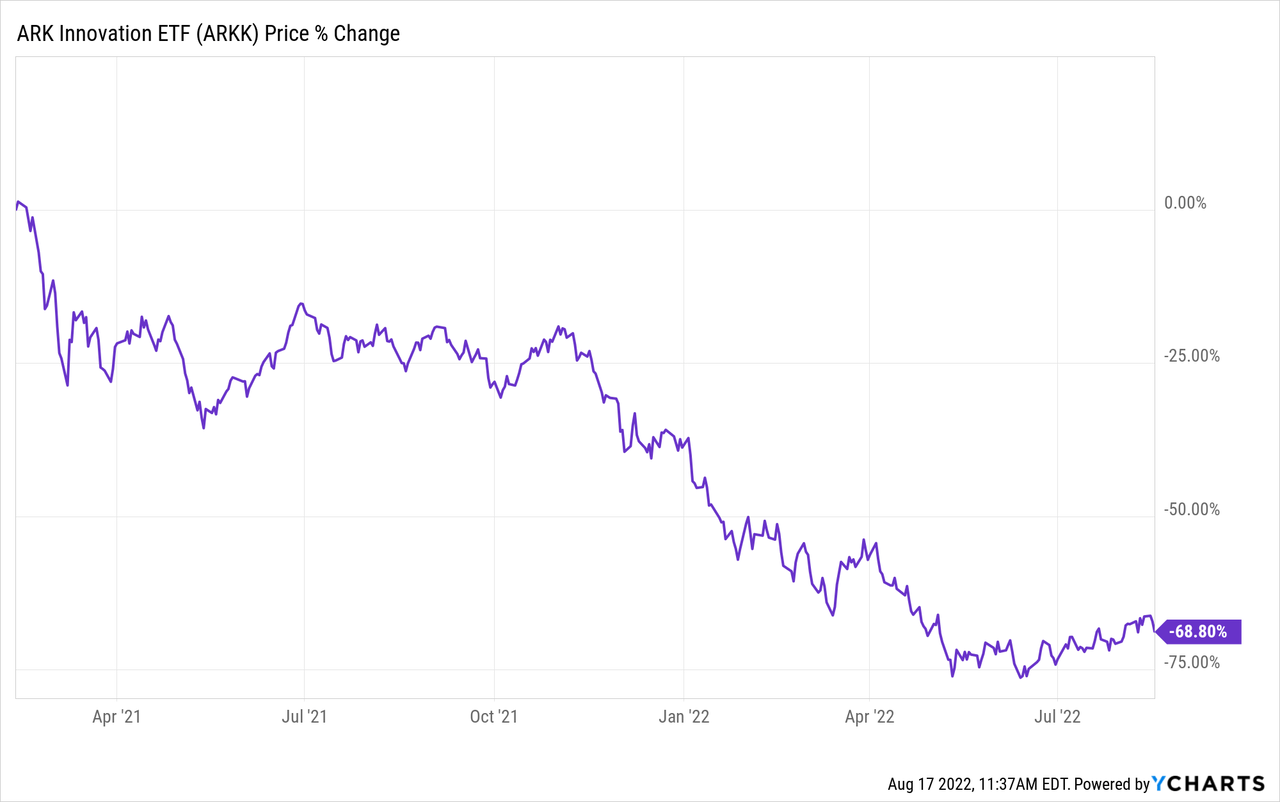

It might be worth examining some of the market proxies for what I warned investors about at the time.

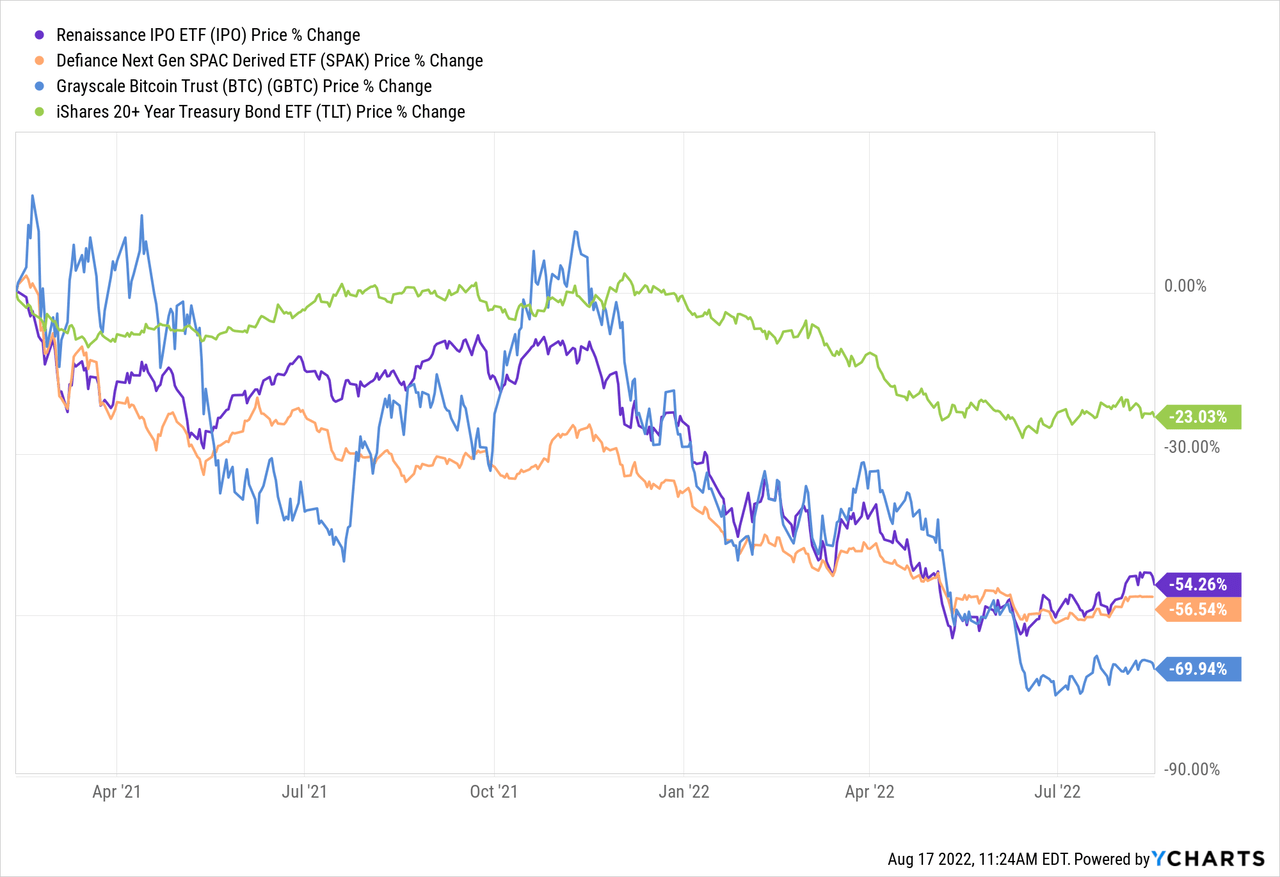

Here is roughly how the first four bubbles in IPOs, SPACs, Long-Duration Bonds, and Bitcoin have performed since the article.

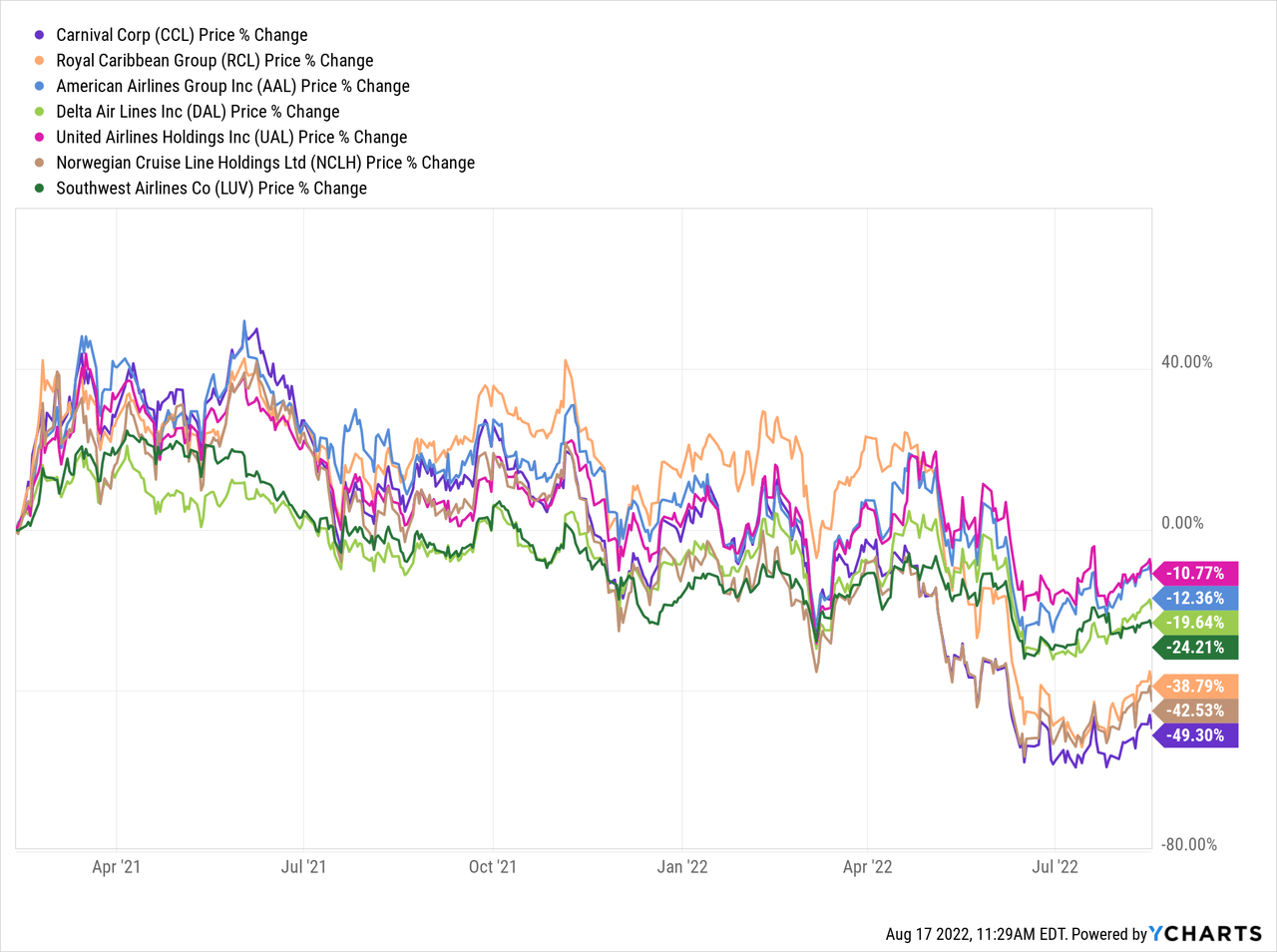

I don’t have a simple ETF proxy for high valuation/high PEG ratio stocks, but many of those have come down over the past 18 months. In terms of companies taking on debt to keep their businesses running, I mostly had airlines and cruise lines in mind.

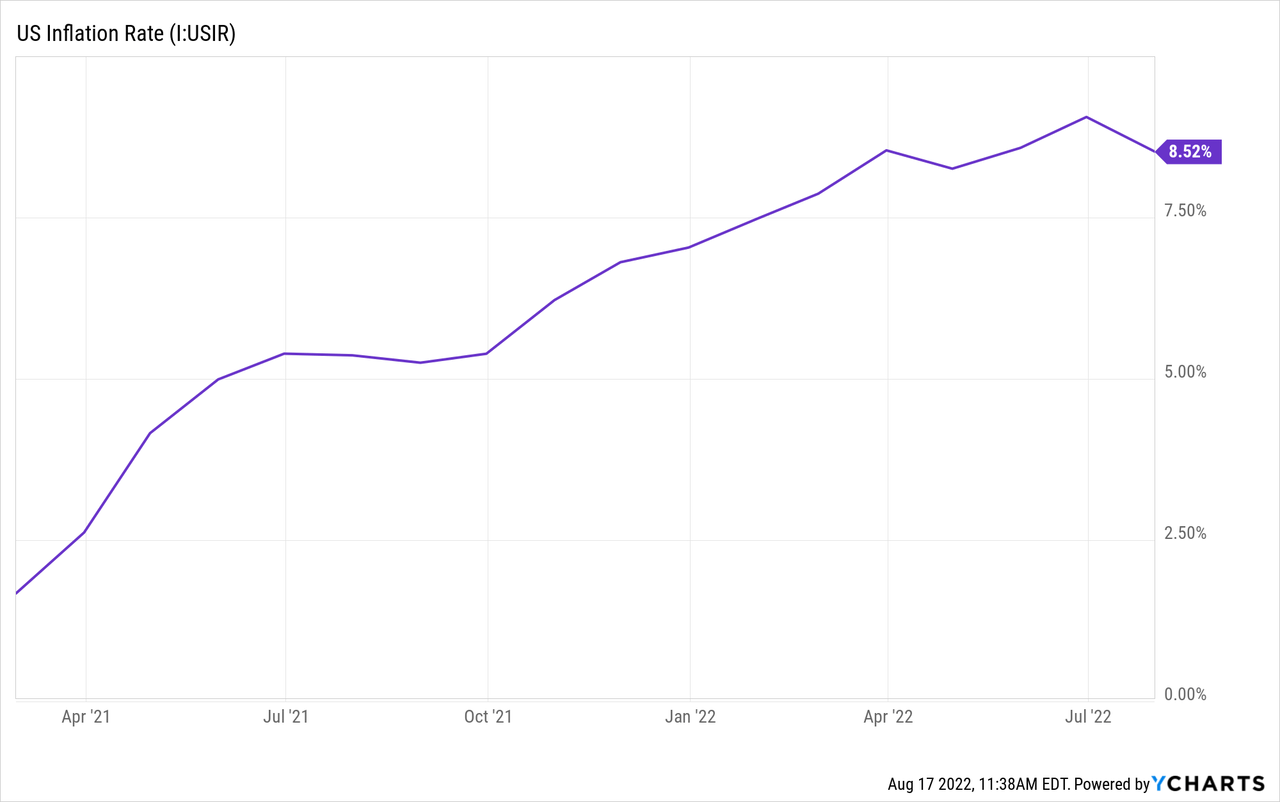

And last but not least, we can look at cash by comparing it to inflation, which was 4.7% in 2021 and is running about 8.5% this year. Let’s just say a loss of purchasing power of -10% or so over the past 18 months.

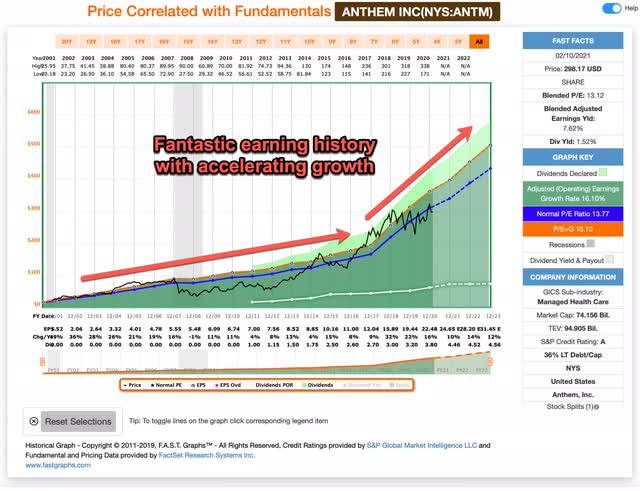

The reason I bring all this up, is because in that bubble article, I also shared 10 stock ideas that I thought, even at that time of many bubbles in the market, were still reasonable buys. One of those stocks was Anthem, which has since changed its name to Elevance Health (NYSE:ELV). Here is what I had to say about it at the time.

Anthem is a health insurer with a fantastic return record currently trading at depressed prices. I have previously written about it on Seeking Alpha and I think it has good medium and long-term potential. Like TROW, Anthem has a PEG ratio near 1.

FAST Graph from February 2021 (FAST Graphs)

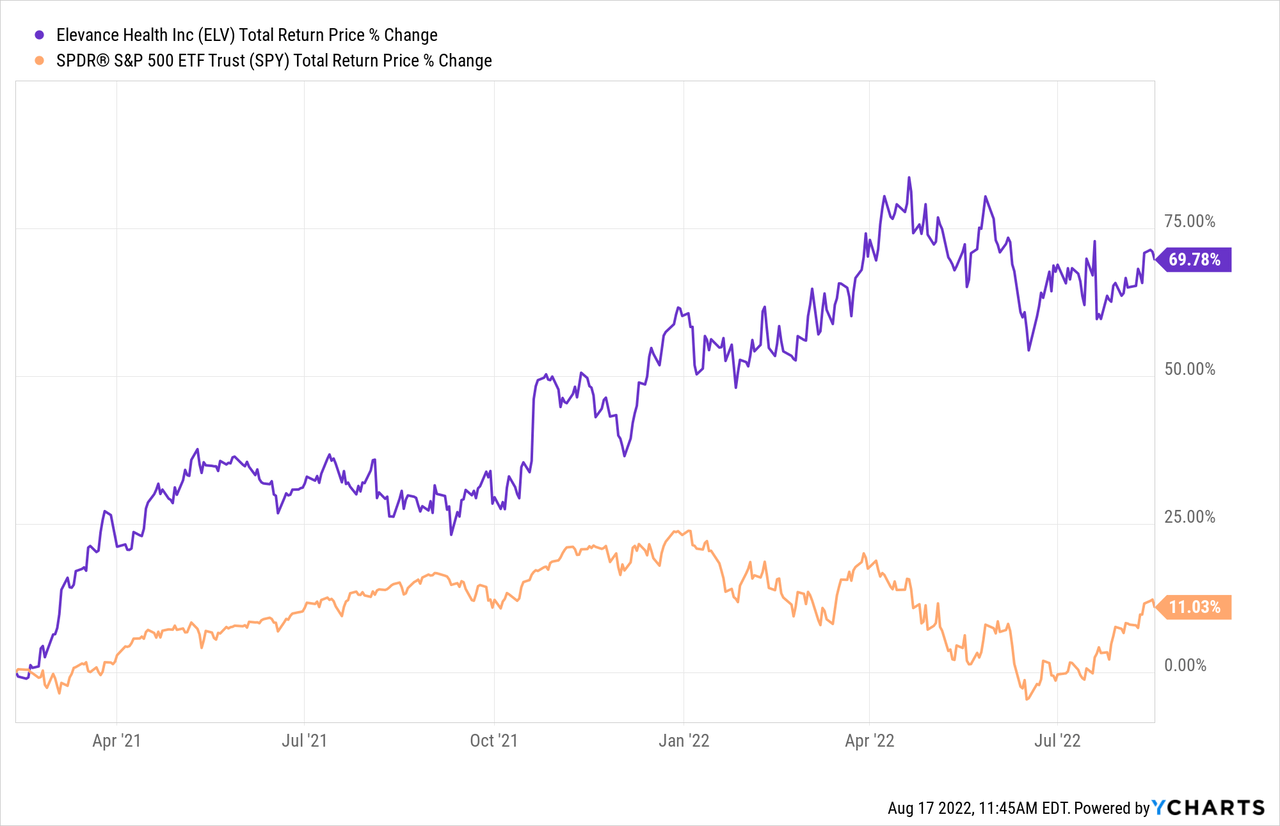

Since the publication of that article, here is how Anthem, now Elevance Health stock, has performed:

Not only has this sleepy, boring stock outperformed all the bubble stocks and ETFs, it has also provided 6x better returns than the S&P 500 index.

One of the main points that I want to make here is that the medium-term returns of popular stocks with great stories but no fundamentals to back up those stories will usually produce poor returns. But if investors totally ignore what social and financial media wants you to pay attention to, and instead focus mainly on the numbers compared to historical trends, you can systematically find stocks just like Elevance Health back in February of 2021. (We actually bought this one on 12/21/20 in my marketplace service, The Cyclical Investors Club, and we still own it.)

In this article, I’m going to share the exact same valuation process for Elevance that I used to initially identify and buy the stock. It is by tracking several hundred high quality stocks using this method that I am able to find good investments, even within the S&P 500, that the market simply isn’t paying attention to.

My Valuation Method For Elevance Health

The valuation method I use for Elevance Health first checks to see how cyclical earnings have been historically. Once it is determined that earnings aren’t too cyclical, then I use a combination of earnings, earnings growth, and P/E mean reversion to estimate future returns based on previous earnings growth and sentiment patterns. I take those expectations and apply them 10 years into the future, and then convert the results into an expected CAGR percentage. If the expected return is really good, I will buy the stock, and if it’s really low, I will often sell the stock. In this article, I will take readers through each step of this process.

Importantly, once it is established that a business has a long history of relatively stable and predictable earnings growth, it doesn’t really matter to me what the business does. If it consistently makes more money over the course of each economic cycle, that’s what I care about — numbers over stories.

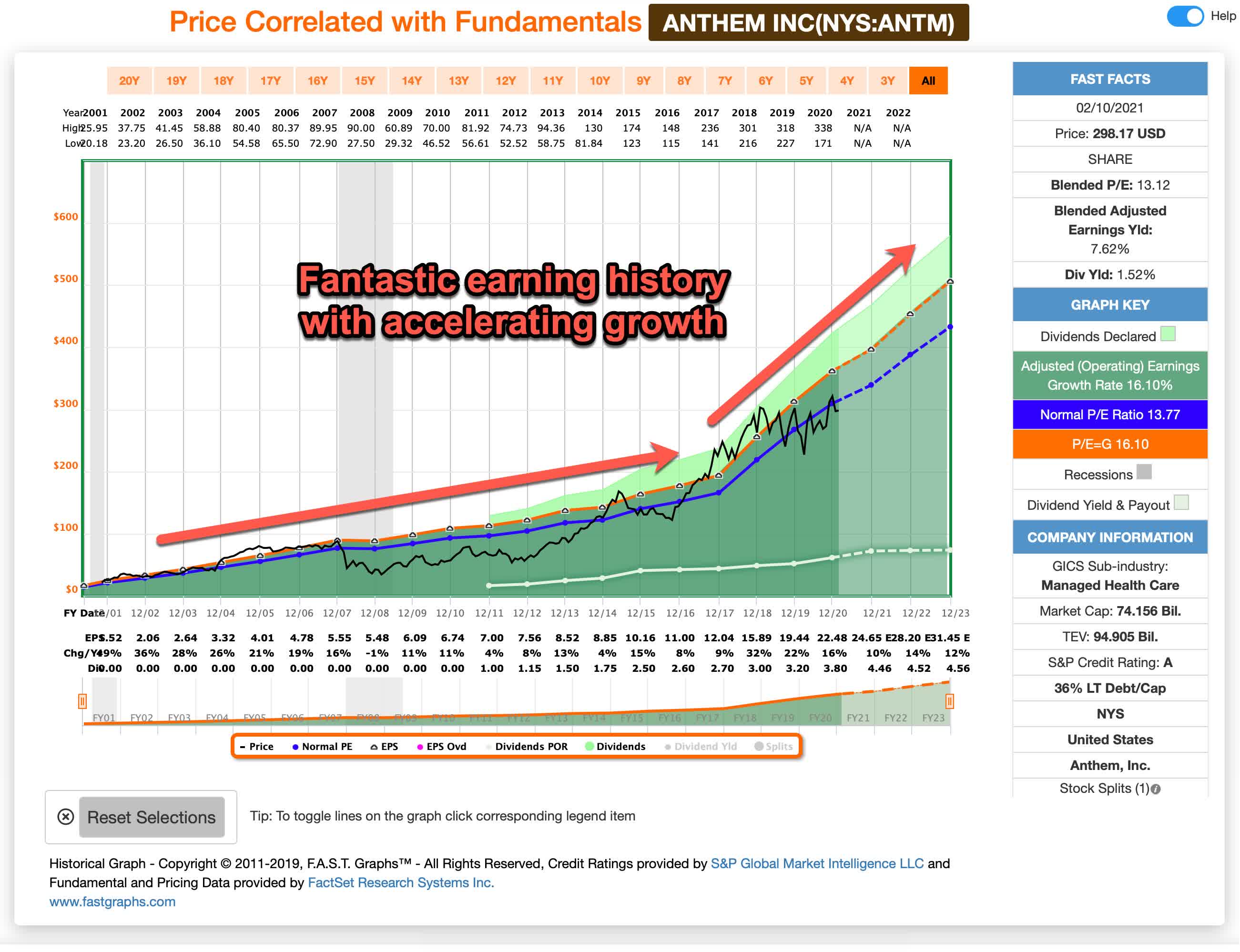

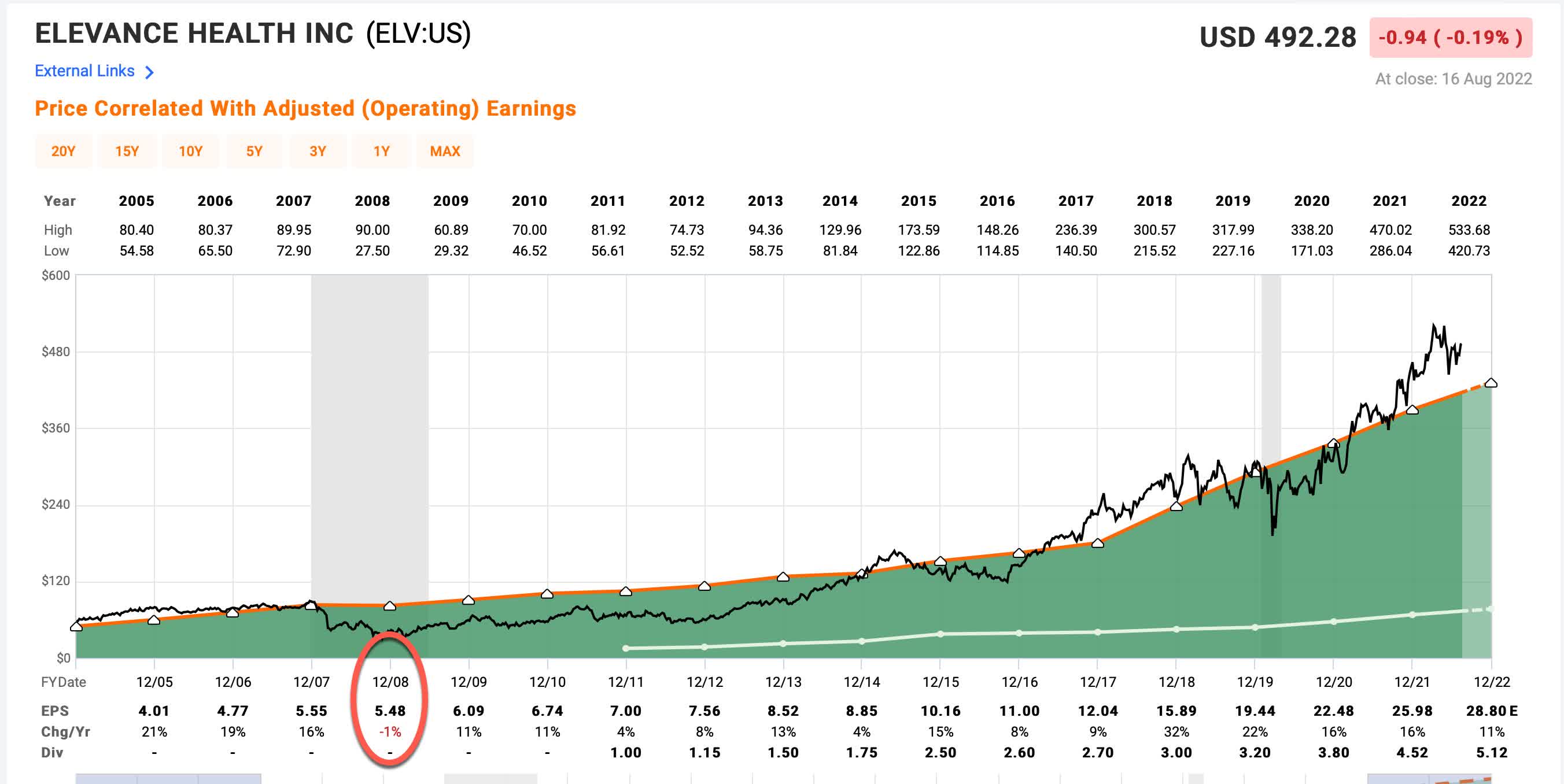

FAST Graphs

Elevance’s historical earnings are represented by the dark green shaded area in the FAST Graph above. Over the past two decades, Elevance only had a single year, during the Great Recession in 2008, when EPS growth declined, and it was only by -1%. This essentially makes Elevance a secular growth business. Additionally we can see that earnings growth has accelerated since 2018 and has been consistently growing double digits.

Because earnings have almost no cyclicality to them, it makes Elevance a very easy stock to analyze via earnings and earnings growth, which is what the “Full-Cycle Earnings” analysis I’m about to share does. If earnings had been more cyclical, then I would have used a different type of analysis.

Market Sentiment Return Expectations

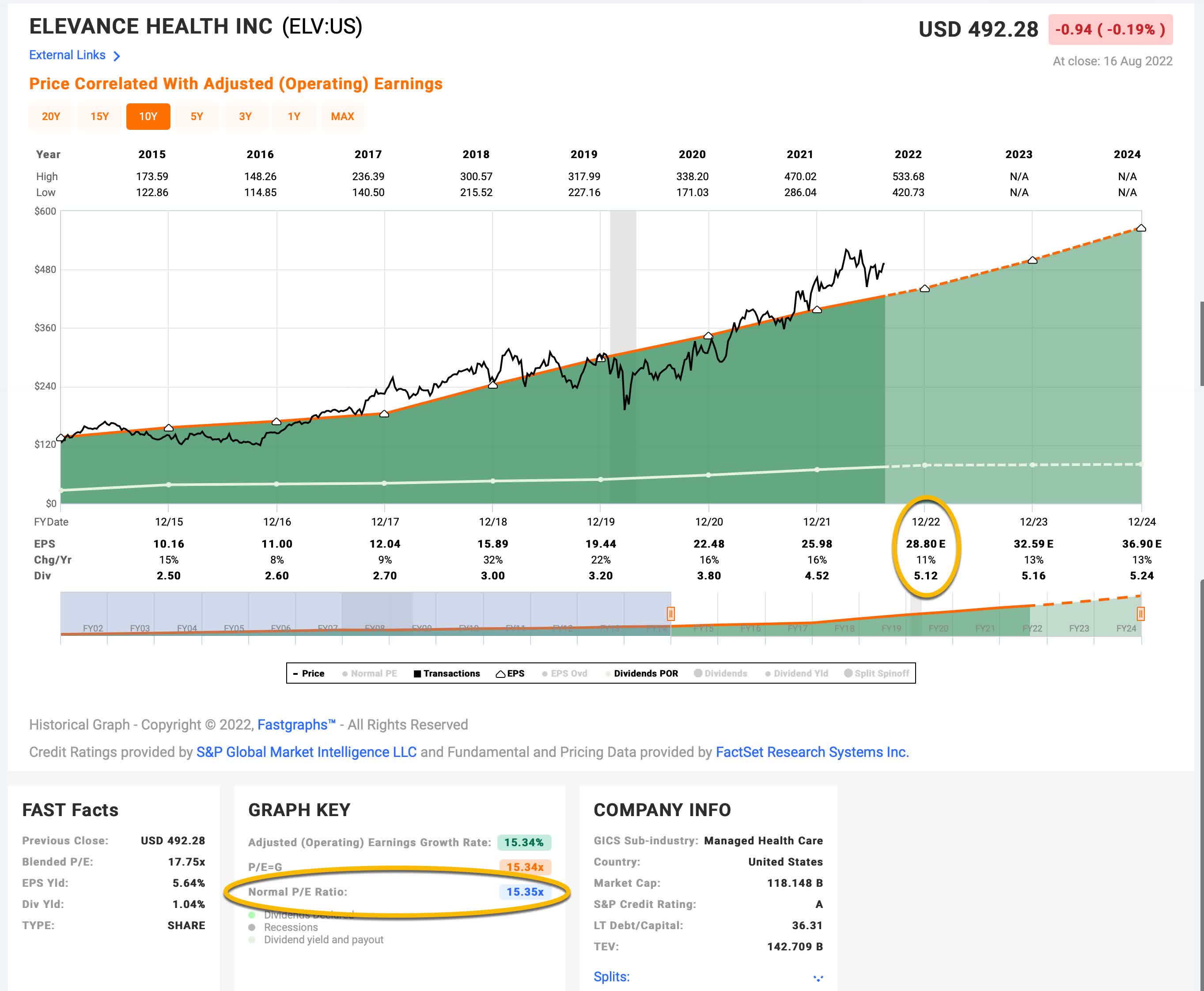

In order to estimate what sort of returns we might expect over the next 10 years, let’s begin by examining what return we could expect 10 years from now if the P/E multiple were to revert to its mean from the previous economic cycle. For this, I’m using a period that runs from 2015-2022.

FAST Graphs

Elevance’s average P/E from 2015 to the present has been about 15.35 (the blue number circled in gold near the bottom of the FAST Graph). Using 2022’s forward earnings estimates of $28.80 (also circled in gold), ELV has a current P/E of 17.10. If that 17.10 P/E were to revert to the average P/E of 15.35 over the course of the next 10 years and everything else was held the same, ELV’s price would fall and it would produce a 10-Year CAGR of -1.07%. That’s the annual return we can expect from sentiment mean reversion if it takes ten years to revert. If it takes less time to revert, the return would be lower.

Business Earnings Expectations

We previously examined what would happen if market sentiment reverted to the mean. This is entirely determined by the mood of the market and is quite often disconnected, or only loosely connected, to the performance of the actual business. In this section, we will examine the actual earnings of the business. The goal here is simple: We want to know how much money we would earn (expressed in the form of a CAGR %) over the course of 10 years if we bought the business at today’s prices and kept all of the earnings for ourselves.

There are two main components of this: the first is the earnings yield and the second is the rate at which the earnings can be expected to grow. Let’s start with the earnings yield (which is an inverted P/E ratio, so, the Earnings/Price ratio). The current earnings yield is about +5.86%. The way I like to think about this is, if I bought the company’s whole business right now for $100, I would earn $5.86 per year on my investment if earnings remained the same for the next 10 years.

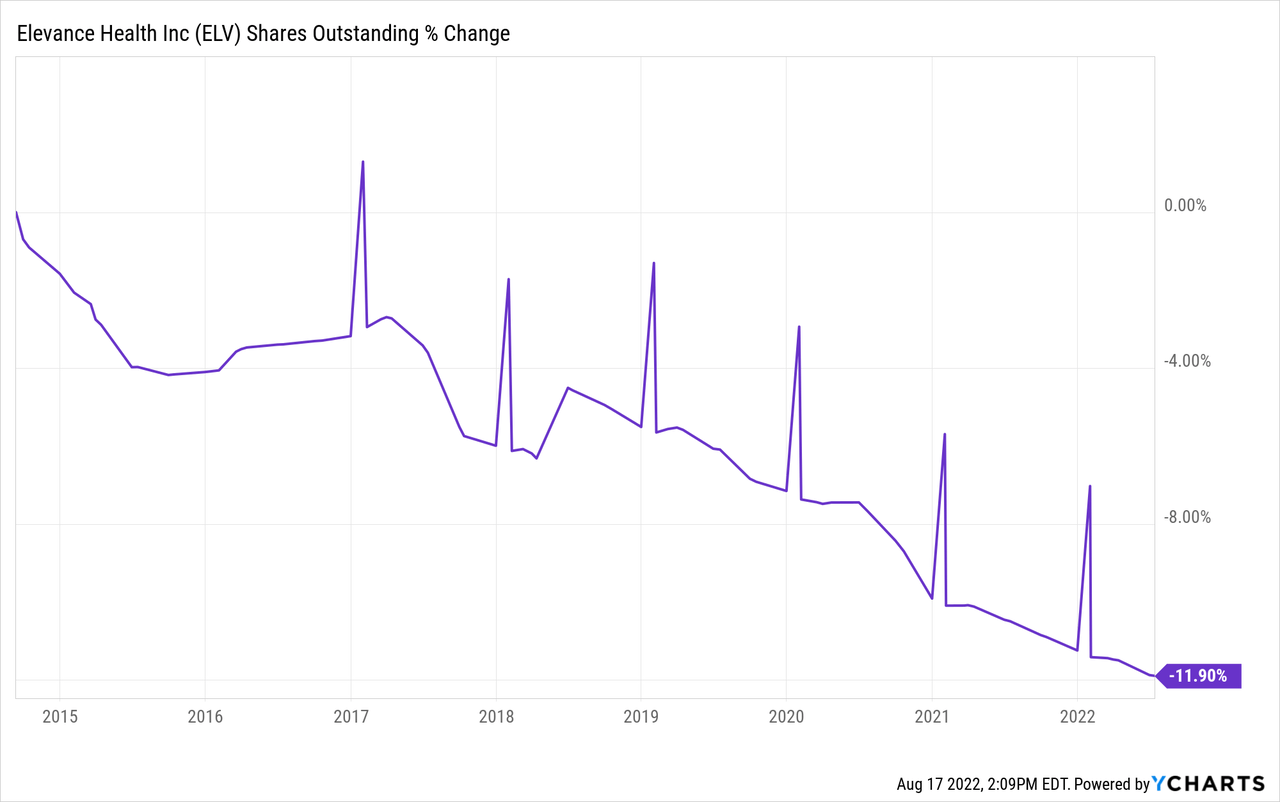

The next step is to estimate the company’s earnings growth during this time period. I do that by figuring out at what rate earnings grew during the last cycle and applying that rate to the next 10 years. This involves calculating the historical EPS growth rate, taking into account each year’s EPS growth or decline, and then backing out any share buybacks that occurred over that time period (because reducing shares will increase the EPS due to fewer shares).

Elevance has bought back about 12% of the company since this point in 2015. I’ll make adjustments for this when estimating the earnings growth rate. After taking the buybacks into account, I have an earnings growth estimate for Elevance of about +14.09%.

Next, I’ll apply that growth rate to current earnings, looking forward 10 years in order to get a final 10-year CAGR estimate. The way I think about this is, if I bought ELV’s whole business for $100, it would pay me back $5.86 plus +14.09% growth the first year, and that amount would grow at +14.09% per year for 10 years after that. I want to know how much money I would have in total at the end of 10 years on my $100 investment, which I calculate to be about $229.82 (including the original $100). When I plug that growth into a CAGR calculator, that translates to a +8.68% 10-year CAGR estimate for the expected business earnings returns.

10-Year, Full-Cycle CAGR Estimate

Potential future returns can come from two main places: market sentiment returns or business earnings returns. If we assume that market sentiment reverts to the mean from the last cycle over the next 10 years for ELV, it will produce a -1.07% CAGR. If the earnings yield and growth are similar to the last cycle, the company should produce somewhere around a +8.68% 10-year CAGR. If we put the two together, we get an expected 10-year, full-cycle CAGR of +7.61% at today’s price.

My Buy/Sell/Hold range for this category of stocks is: above a 12% CAGR is a Buy, below a 4% expected CAGR is a Sell, and in between 4% and 12% is a Hold. A +7.61% CAGR expectation makes Elevance Health stock a “Hold” at today’s price, and almost right in the middle of what I would consider the fair value range.

We can see the importance of buying a stock like this at a very attractive valuation. It allows for a situation like this, where the stock price can rise over +60% in less than two years, and still not be overvalued. In fact, it’s not unthinkable that this stock could see double-digit growth for many years to come and all an investor needs to do is hang on to it.

Conclusion

Boring stocks that almost nobody is paying attention to can often make great investments if they can be purchased at the right price. Not only is it unlikely the stock price will fall super deeply, but they also have the potential to provide market-beating returns, even while stocks that were once media darlings get crushed. The best way to find these boring stocks (other than by following writers like me) is to first and foremost, focus on the numbers and likely returns rather than the “stories” we, as humans, love so much. Elevance was extremely easy to identify as a good value in late 2020 and early 2021. Simply looking at the PEG ratio and previous earnings growth stability should have attracted lots of investors. And, eventually it did. But only after the fads and story-stocks of the day mostly fell by the way-side.

It’s possible that if we have a recession next year that Elevance could fall to buyable levels again. Currently, my buy price for the stock for new money is about $377 per share if we are not in recession, but if we have an average recession, the price could fall as low as $270, and which point it would be a steal for those investors who are paying attention.

Please note that foreign exchange and other leveraged trading involves significant risk of loss. It is not suitable for all investors and you should make sure you understand the risks involved, seeking independent advice if necessary.

Be the first to comment