LuckyBusiness/iStock via Getty Images

Hard Landing for Defense

Retail value investors can find a potential opportunity for growth in aerospace and defense (AD) stocks. 2021 was a banner year for defense stocks. 2022 was a volatile one plagued by inflation supply chain issues, especially the shortage of semiconductor chips, and skilled labor shortages. 2023 is muddling along.

We are moderately bullish on Elbit Systems Ltd (NASDAQ:ESLT), Israel’s biggest military and arms company, for the long term. We think the stock is near the bottom but might slip another 10%. It is currently out of favor because of recent weaker financial reports. Wars and skirmishes around the world depend on high-tech electronics sustaining the AD industry. The industry is overcoming the macroeconomic issues it struggled with in the last couple of years.

Shares are selling a tad above their 52-week low of $159. The shares hit a high of $244.59 last August and tumbled from there. In the fall of 2022, Defense News reported flat sales and earnings among major AD companies; forecasts were for no increases in 2023. We are moderately bullish. The shares will likely recover along with the AD industry.

2021 was a stellar year for aerospace and defense or AD stocks. The SPDR S&P Aerospace & Defense ETF (XAR) hit $133 per share. The price tumbled in 2022. After bottoming into the mid-$90s, shares began a steady climb. The XAR share price is up 5% YTD. Seeking Alpha lifted its Quant Rating on XAR from Hold to Buy. Elbit shares are -3.25% over the last 12 months but +3.8% YTD.

Decent Grades

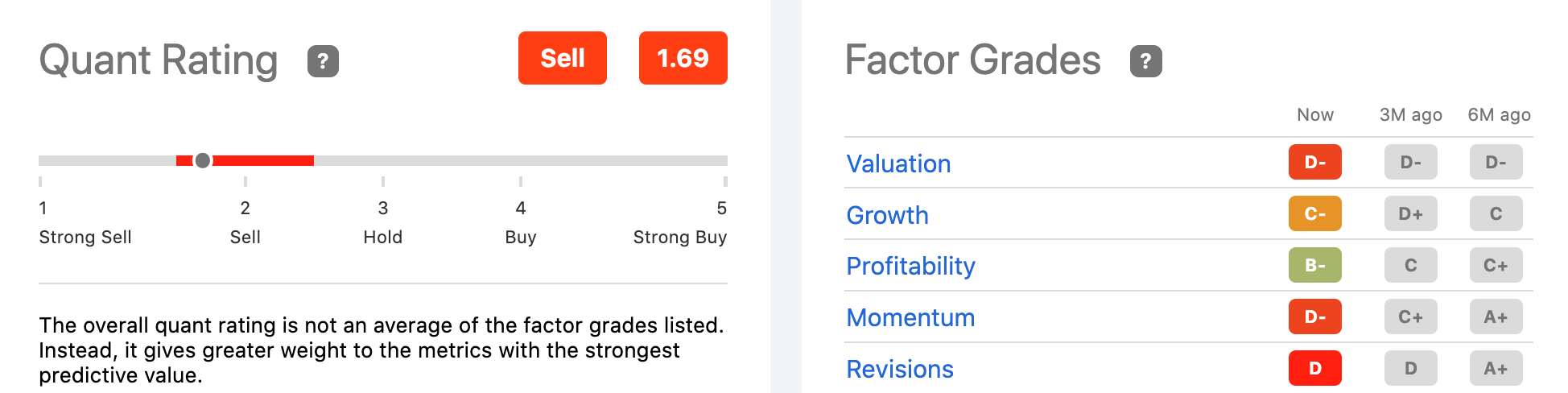

Despite SA’s Factor Grades for Elbit Systems of B- (up from C) for profitability and C- (up from D+) for growth, the Quant Rating YTD is Sell to Strong Sell. It was a Buy in Q1 FY ’22, a Hold rating through August, and a Sell in the Fall into January ’23 when AD stocks were flat.

Quant/Factor Grades Elbit Systems (seekingalpha.com/symbol/ESLT/ratings/quant-ratings)

The Numbers

The Stockholm International Peace Research Institute bills itself as “the independent resource on global security.” SIPRI’s arms industry database puts Elbit Systems at 28th in worldwide weapons sales in ’21. We discuss this in greater length in our earlier articles.

Elbit’s financial fundamentals are positive portents after a weak year for the industry and predictions for growth in 2023.

Fundamentals (ycharts.com/companies/ESLT)

Elbit has a $7.6B market cap and holds $2.5M in cash. Total debt at the end of the last quarter was $1.4B leaving it an enterprise value of $8.8B. In 2021, Elbit Systems had annual total returns of 34.77% compared to the S&P 500 total return of 28.7%. Elbit’s debt-to-equity ratio is 2.63, as of September 30, 2022.

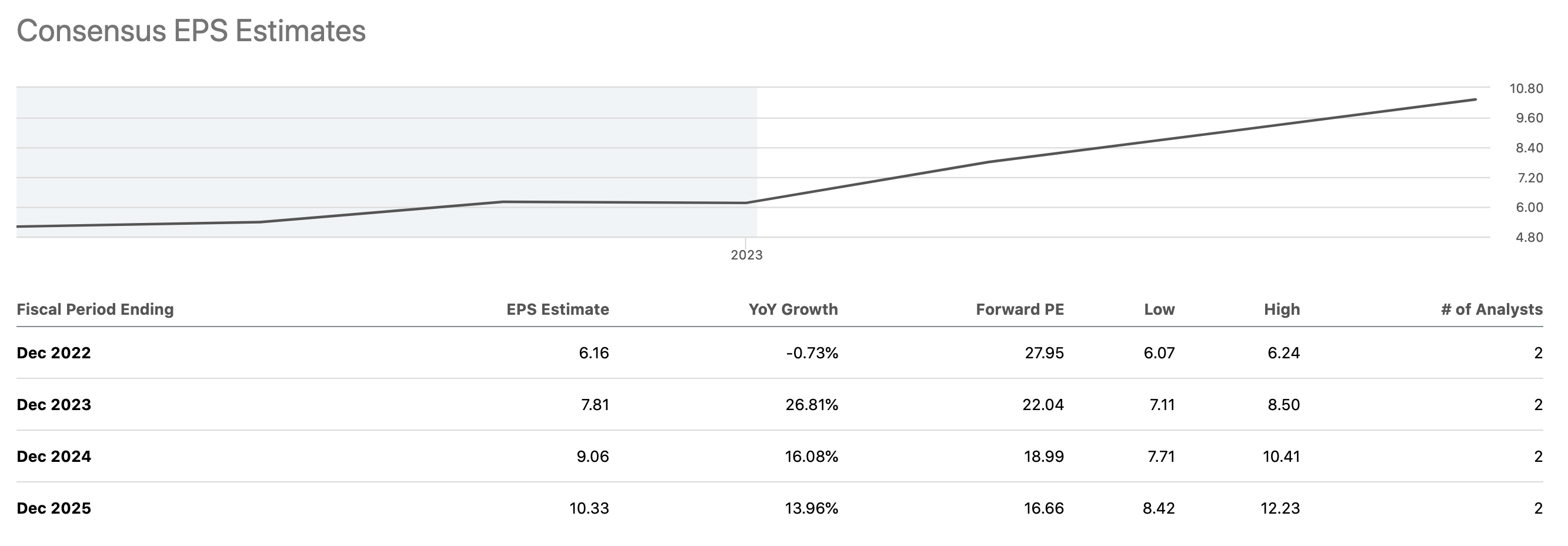

Elbit’s next earnings release will be on April 4, 2023. At the low end, we forecast an EPS of $1.85. There are estimates for an EPS of up to $1.96 in the next report. SA issued a warning 5 weeks ago that Elbit is at risk for performing badly. SA gives the stock a D- for valuation. The company P/E Non-GAAP (FWD) then was 27.42; the PE (TTM) is now 38.05.

The last time the actual EPS figure topped the estimate was in Q3 ’21. Since then, the actual EPS came in lower than estimates. In Q3 ’22, the EPS estimate was $1.90 but actually was $1.26. We forecast a Q4 ’22 EPS at $1.95.

Annually, earnings estimates are looking better and underpin our positive feelings about Elbit. The dividend is weak with a yield (FWD) of just 1.16% but it is safe, consistent, and has grown.

Consensus EPS (seekingalpha.com/symbol/ESLT/earnings/estimates)

Annual revenue estimates are for 5.2% growth to $5.55B in FY ’22, 6.04% to $5.89B in FY ’23, and 7.44% to $6.33B in FY ’24. Financial struggles at Elbit Systems are the primary cause of the stock drop. It is also due to light news coverage, some successful boycott activity of Israeli AD companies, light average daily trading volume, and only a small handful of analysts writing about the stock.

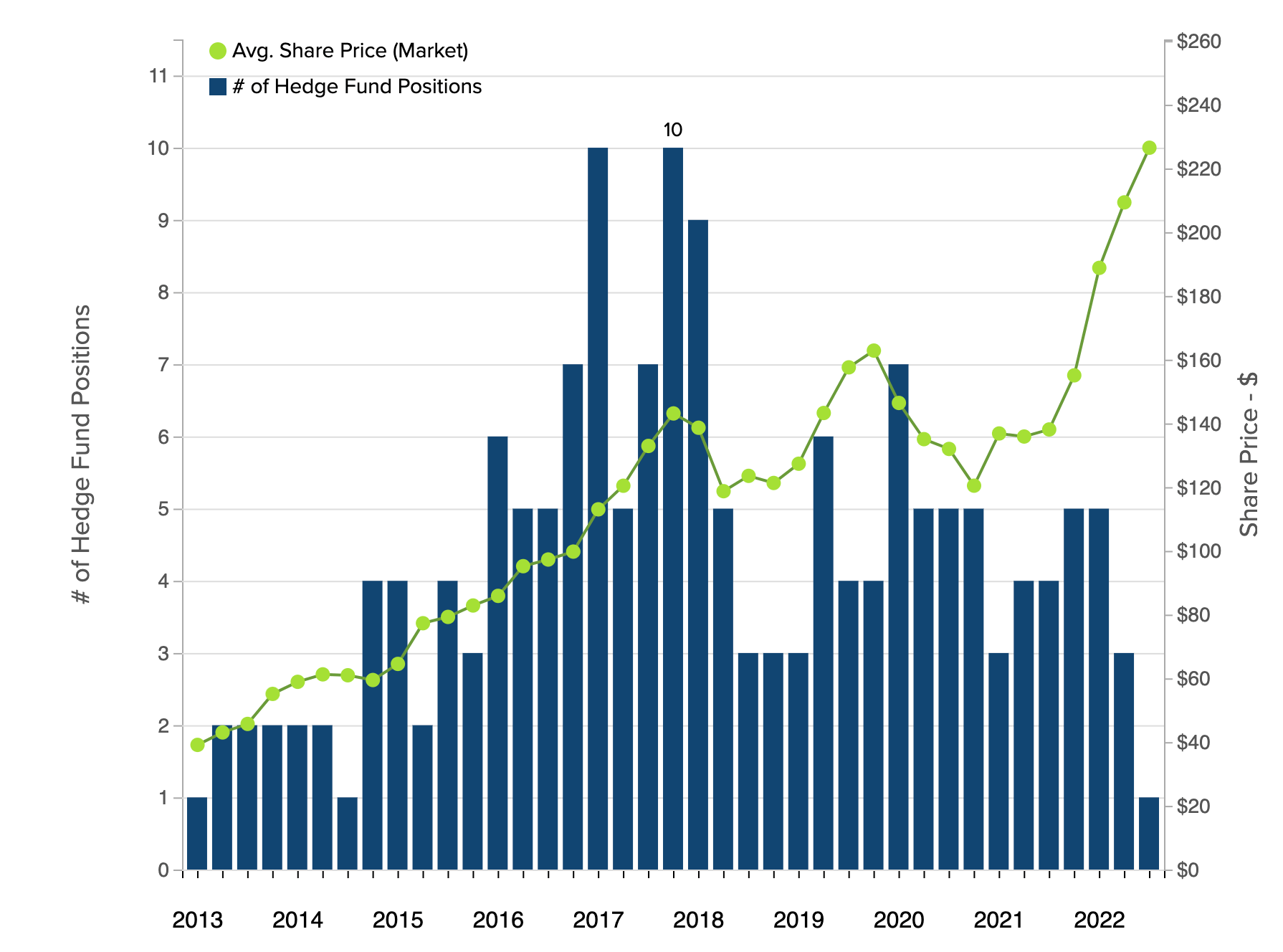

The stock fell out of favor with hedge funds and major investors even as the share price moved higher. Cathie Wood’s fund was long and the leading stakeholder at the end of Q3 ’22 according to one report we read.

Hedge Funds Investment (insidermonkey.com)

According to Deloitte,

88% of surveyed senior executives indicated that they believed the general business outlook for the aerospace and defense industry for the next year is ‘somewhat to very positive’.

Insider Monkey contends Elbit Systems is going to be one of the best AD industry stocks to own in 2023. Its portfolio of high-tech arms and weapons is constantly in demand. They cover the land, sea, and air; defense and offense; manned and self-driving; cyber-security software and simulation training systems. Israel is Elbit’s biggest customer with a consistent need for defensive weapons and military cyber systems. Several business news services are reporting an optimistic outlook for the Israeli AD industry.

As far back as 2014, there were rumors that some Israeli AD companies might be for sale. Rumors persisted and then last year RADA Electronics sold to an Italian-American defense contractor. That move might have monster companies with market caps well over $100B looking at Elbit Systems. The industry is emerging from a three-year long drought of M&A activity, observes PWC corporation. Its outlook for 2023:

A&D dealmaking trends continue in the direction of smaller defense and government services transactions, as companies seek to optimize their portfolios and focus on areas with the greatest potential for profitable growth. The industry remains in a very strong cash position, and we suspect many deals could be made by leveraging the strength of balance sheets.

Takeaway

Elbit Systems stock is out of favor and has weak momentum. The stock may be near bottom after missing Q3 misses of EPS and revenue, as reported last November. The company is profitable and has growth potential. Its dividend yield is middling but safe, consistent, and also with growth potential. Institutions and private corporations own 65% of the stock. The public and others own +34%. Stakeholders in Elbit might be economically attracted to offers.

Its customers are largely governments around the world looking to remake their military defense systems into cutting-edge electronic high-tech fighting forces. Since January 1, ’23, Elbit signed over $450M in deals with:

- Israel for electro-optical systems,

- to maintain training centers for Israel’s F-15 and F-16 fleet

- to supply rockets to a European country

- to supply the British army with Magni-X drones and systems

- The firm has a global reach and is based in the start-up nation. That makes it, in our opinion, particularly attractive as a niche acquisition once the AD industry gets legs again for M&A activity.

Meantime, the greatest risk is that the stock drops further, perhaps another 10%, especially if the Q1 ’23 earnings report is lame. But in time the share price will likely climb again to its high as it did last year. Mark Twain might have thought war is “a wanton waste of projectiles,” but is inevitable and keeps companies like Elbit Systems in demand.

Be the first to comment