da-kuk

iShares MSCI EAFE Growth ETF (BATS:EFG) is an exchange-traded fund that provides investors with exposure to a broad range of companies across Europe, Australia, Asia, and the Far East, whose earnings are also anticipated to grow at an above-average rate. The fund is popular, with net assets under management of $11.3 billion as of January 27, 2023. EFG’s expense ratio is reported as 0.36%. The fund does not invest in the United States or Canada.

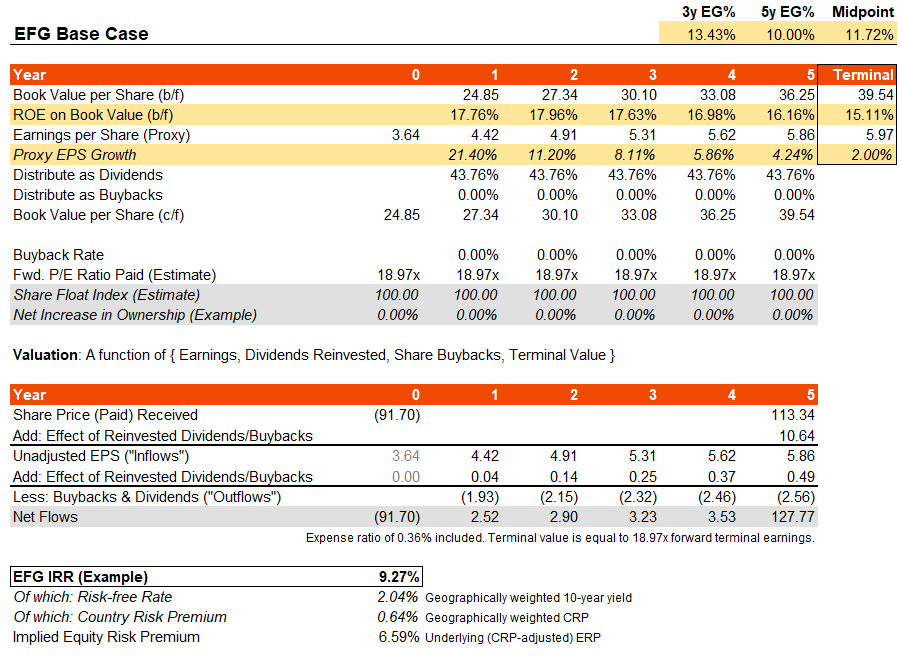

EFG seeks to replicate the performance of its chosen benchmark index, the MSCI EAFE Growth Index, for which we can retrieve a factsheet as of December 30, 2022. The factsheet’s data can serve as a proxy for EFG’s portfolio: with trailing and forward price/earnings ratios of 23.03x and 18.97x as of that date. The price/book ratio was stipulated as 3.37x, with a trailing dividend yield of 1.90%.

This data would suggest 21.40% earnings growth in the next twelve months, with a forward return on equity of 17.76%. Based on this, and assuming return on equity trickles down to a more modest 15% or so over the next 5-6 weeks, I am going to assume an average geometric earnings growth rate of 10% per year over the same time frame (falling to 2% in the terminal year). That is just under, or in line with, Morningstar’s three- to five-year estimate of 11.46% at the time of writing for EFG’s portfolio.

I would also take note of the earnings multiple. In my calculations, I find a geographically-weighted risk-free rate of 2.04% at present (based on 10-year yields of the countries EFG is exposed to, which include principally Japan at 21%, France at 15%, Switzerland at 14%, the United Kingdom at 10%, etc.) and a country risk premium (weighted) of 0.64% based on the same geographical weights and based on Professor Damodaran’s work. I think it would be wise to not assume a significant drop in risk-free rates in the long run, given the weighted average is still only 2% (even if recent inflationary pressures abate). I also would prefer not to move the country risk premium element. Assuming 2% terminal growth and an adjusted 4.5% equity risk premium, a fair multiple in the terminal year would be up to 20x.

The current forward earnings multiple is 18.97x, as mentioned earlier, for EFG. I would think it unwise to assume an expansion, so instead I will keep this constant throughout my forecast period. My base assumptions are illustrated below, offering a healthy IRR potential of 9.27% with an underlying (adjusted) equity risk premium of 6.59%.

Author’s Calculations

That, to me, suggests under-valuation. A fair IRR in this case might be circa 7%. Of course, equity capital is not infinite; so, international stocks can be pulled down by the competitiveness of U.S. and other well-performing markets. However, ex-U.S. stocks have been doing well recently, and I think there is some fundamental basis for it. On the basis of fair value alone, I think EFG’s portfolio is trading at a potential forward 30% upside potential on valuation alone (i.e., at a -20% to -25% discount). Regardless, an IRR of over 9% per annum is possible by holding EFG over the long run by my calculations. This makes EFG interesting to me as an international diversifier.

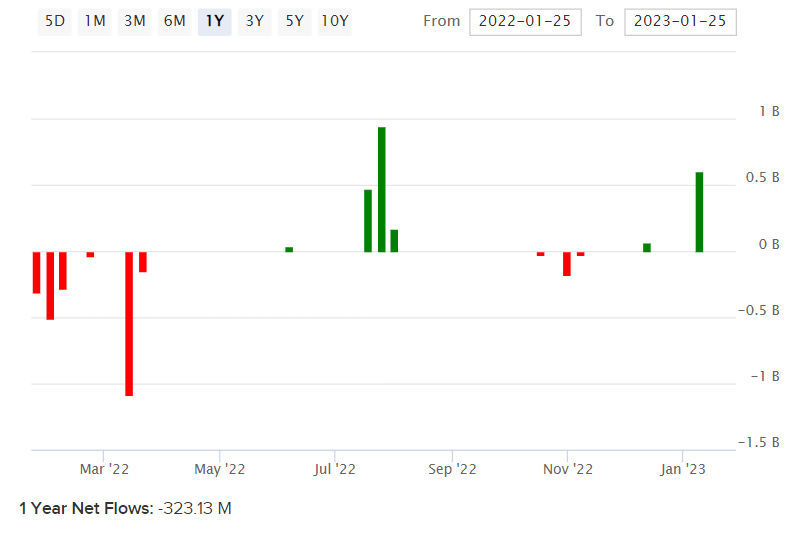

Over $300 million has been pulled from EFG over the past twelve months (see below).

ETFDB.com

I think there is room for a rebound via both inflows and valuation change, plus via a strong headline IRR potential independent of valuation change. Into the next global business cycle, as economic activity picks up, I think international growth stocks will look especially appealing. I would take a bullish view at this juncture; the only reason why I would not take an extremely bullish view that the headline IRR potential is still “within the atmosphere”. Occasionally you might come across an ETF with a 15-20% IRR potential, but in this case you cannot count on the valuation gap closing. Still, 9% per annum would be good.

Be the first to comment