ljubaphoto/E+ via Getty Images

In our last Autoliv (NYSE:ALV) article we argued that shares were attractively priced if things started to normalize for the company, and rated shares as a ‘Buy’. Since then shares have outperformed the S&P 500 index (SPY) by more than 2x, going from ~$73 to ~$93. We believe the undervaluation has been corrected, but since the company is performing well operationally it can be considered a solid ‘Hold’.

The company delivered a particularly strong fourth quarter, where profitability recovered substantially. The company is seeing the benefits from price increases it implemented to offset higher costs, as well as some operating efficiency initiatives. The company said it continues to further renegotiate new and running contracts and that it is implementing greater pricing flexibility into them to better account for changing costs and be fairly compensated. For instance, it now has ~50% of its contracts with raw material clauses.

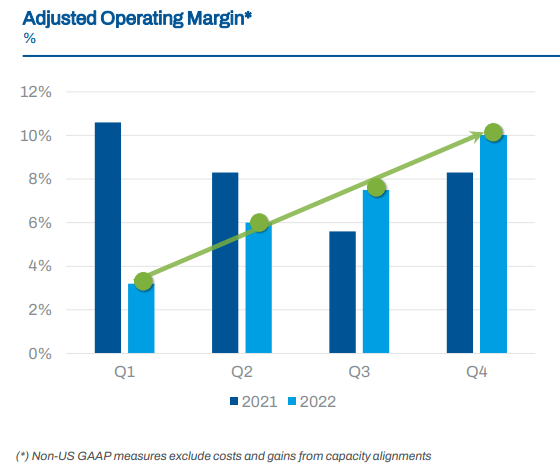

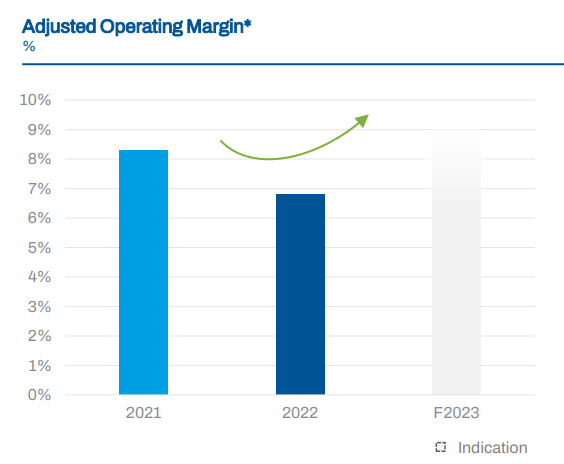

The company’s order intake for the year was strong, with a high rate of wins for new EV platforms, and order win rates with new EV makers and traditional OEMs increased. The company expects an increase in product launches in 2023. The adjusted operating margin was 10% in the quarter, significantly higher than the previous quarters, as can be seen in the graph below.

Autoliv Investor Presentation

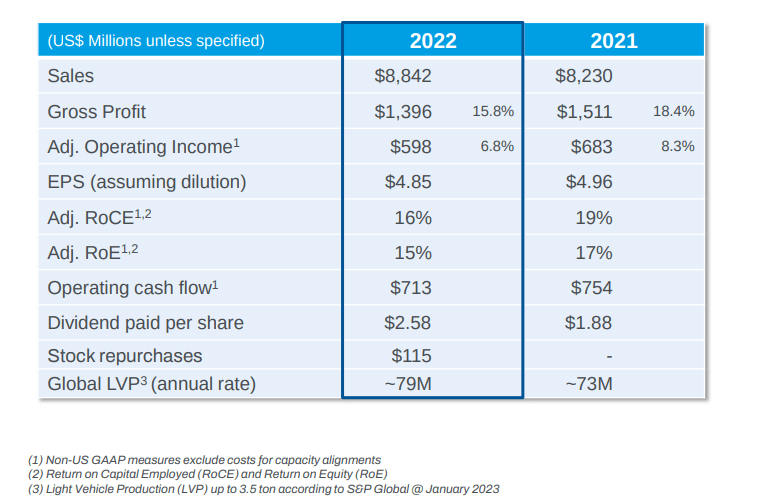

The year 2022 was marked by turbulence in light vehicle production with supply chain disruptions causing lower and more volatile production than expected. The company’s net sales were $8.8 billion, up 14% organically, while adjusted operating income decreased by 12% to $598 million, with a margin of 6.8%. The company expects stronger cash flow in 2023 from higher net income and more stable light vehicle production.

Outperforming Light Vehicle Production

Despite concerns surrounding the ongoing volatility of the supply chain and recessionary fears, global LVP is projected to increase ~3 % in 2023. Importantly, Autoliv expects market share gains to be larger in 2023 than they were in 2022.

North America US car sales are expected to rise by over 1 million units but still remain well below the pre-pandemic norm of over 17 million. Europe is expected to remain very weak, and in China first quarter production has been reduced by close to 0.5 million units, with volume losses expected to be recovered in subsequent quarters.

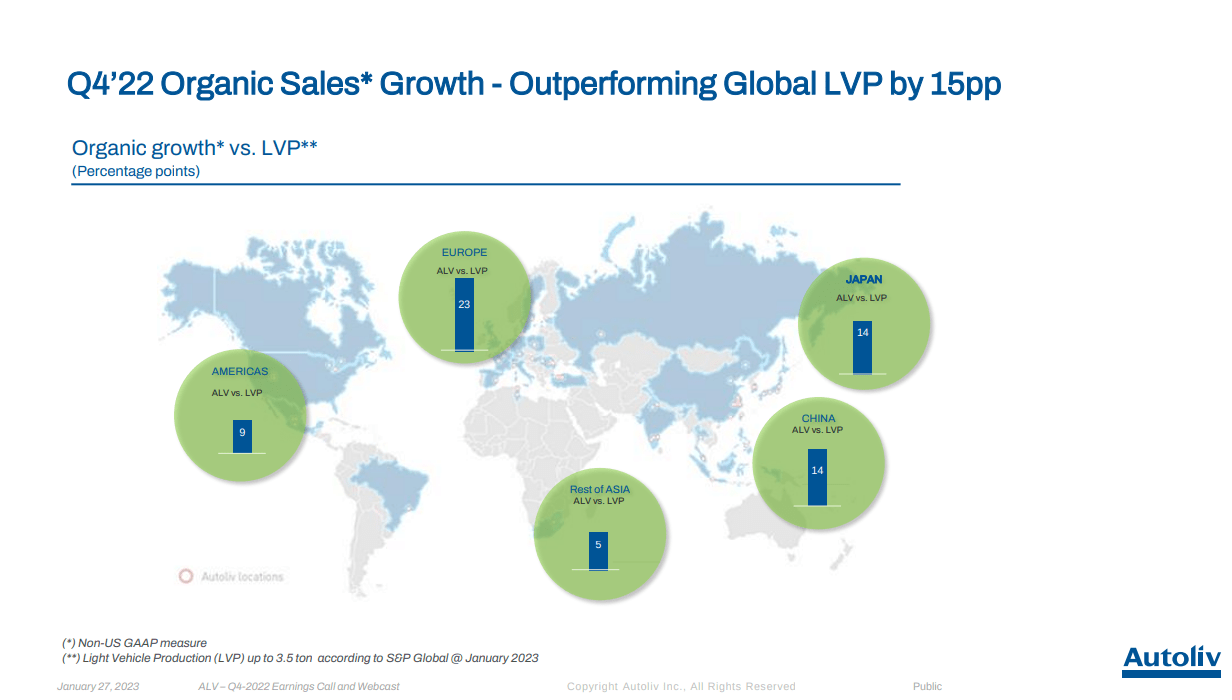

Autoliv sales tend to correlate strongly with LVP production, but they tend to outperform its growth thanks to increasing safety content per vehicle, and market share gains. For example, in Q4 the company outperformed global LVP by 15%.

Autoliv Investor Presentation

Still, the company had guided for stronger outperformance for 2022 than what they delivered. For 2022 the company expected ~11-12% outperformance, and ended delivering only about ~7% outperformance for the year. During the earnings call an analyst asked why the company underperformed their previous guidance, and this is what CEO Mikael Bratt replied:

Yes, the main difference when we compare to the beginning of last year was the regional mix. So, Europe was expected to be up, I think it was 17%, 18% on a year-over-year basis and it actually ended up being down 1% or 2%. And that, as it has been one of our highest content per vehicle markets that created a very large negative regional mix, which is the main explanation of that difference.

Financials

In 2022 Autoliv faced the worst cost inflation in decades, which impacted its profitability significantly. Through aggressive price adjustments the company gradually managed to offset raw material cost inflation, and profitability was for the most part, restored by the end of the year. It also took some cost saving activities and higher volumes to accomplish this, but now the company is in more solid footing. Still, earnings per share were a little bit lower in 2022 compared to 2021 despite higher sales, and share repurchases.

Autoliv Investor Presentation

Balance Sheet

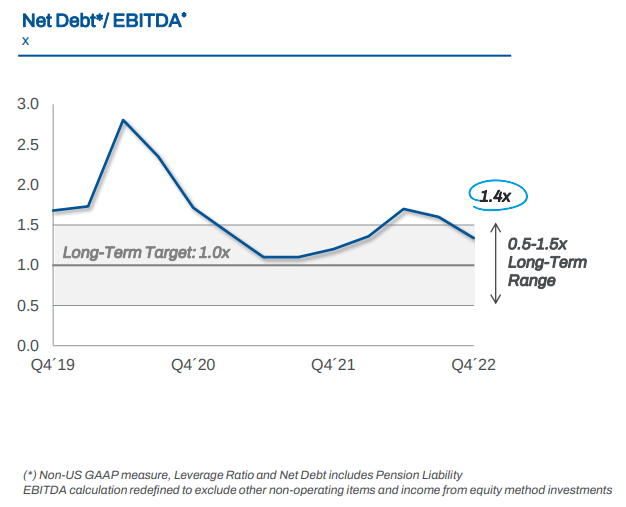

Leverage improved, with net debt decreasing by $99M from the third quarter and EBITDA for the trailing twelve months increasing by $49M. Net debt to EBITDA is now ~1.4x, which is within the company’s long-term range target. The company has maintained its BBB credit rating from S&P Global, and has ~$1.7 billion in liquidity. What this means for investors is that the company is in decent financial shape, but given the cyclicality of its industry we would prefer if the company operated with even lower leverage.

Autoliv Investor Presentation

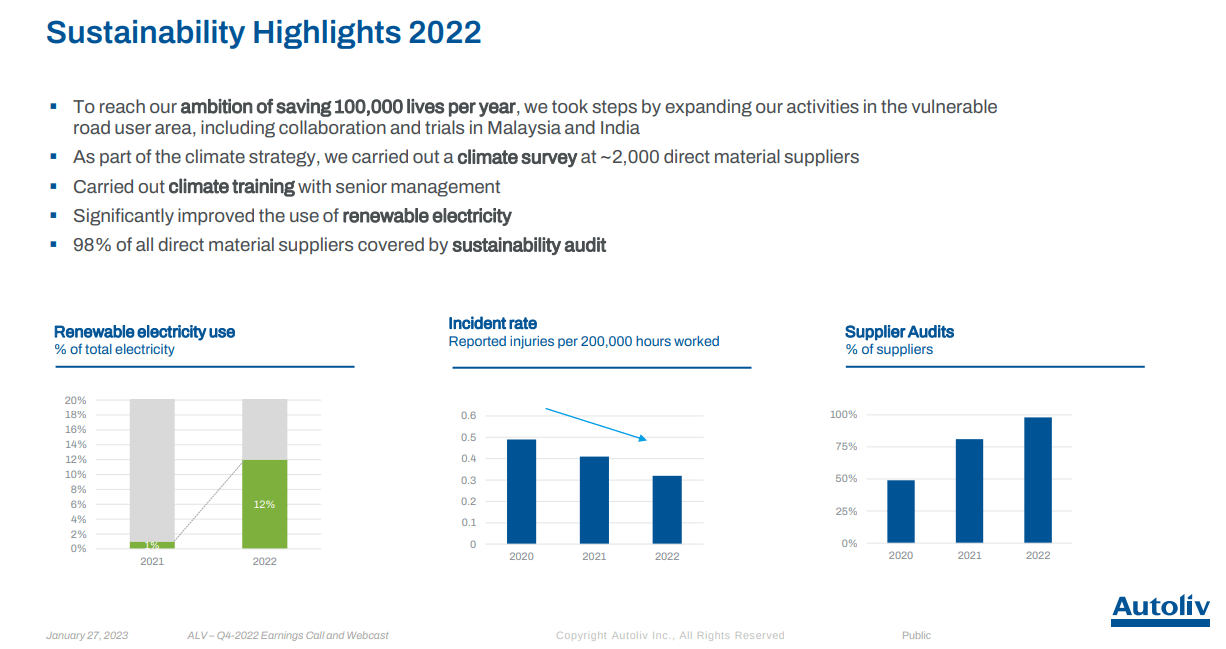

ESG

Autoliv made significant progress on its ESG initiatives in 2022. In particular it significantly increased the percentage of renewable electricity it uses in its operations. The work incidents rate continues to trend downward, and it is doing a better job auditing its suppliers.

Autoliv Investor Presentation

Guidance

Autoliv is guiding for significant outperformance compared to LVP growth. LVP is expected to grow ~3%, and Autoliv is guiding for organic sales to increase by around 15%, and for an adjusted operating margin of ~8.5% to 9%. The company plans to achieve this operating margin through price increases, efficiency initiatives, strict cost control, more supply chain stability. It expects gradual improvements quarter by quarter, a similar pattern as that of 2022. The adjusted operating margin for Q1 of fiscal year 2023 is likely to be at the mid-single digit level.

Autoliv Investor Presentation

Valuation

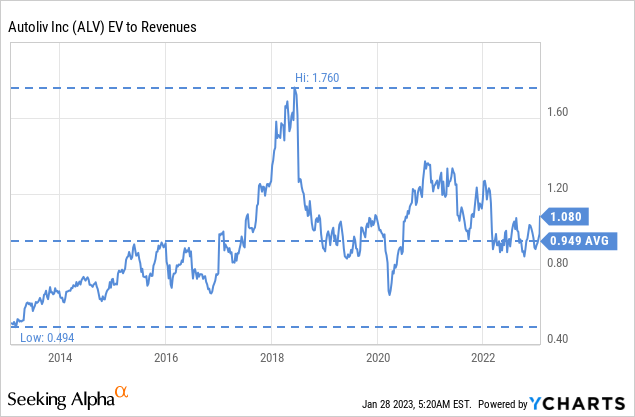

Most valuation indicators now point to shares being fairly valued. For example, the EV/Revenues multiple is now at ~1.08x, roughly 14% above the ~0.94x ten year average. Given that strong revenue growth is expected for 2023, this multiple remains reasonable, but we do believe most of the previous undervaluation has been corrected.

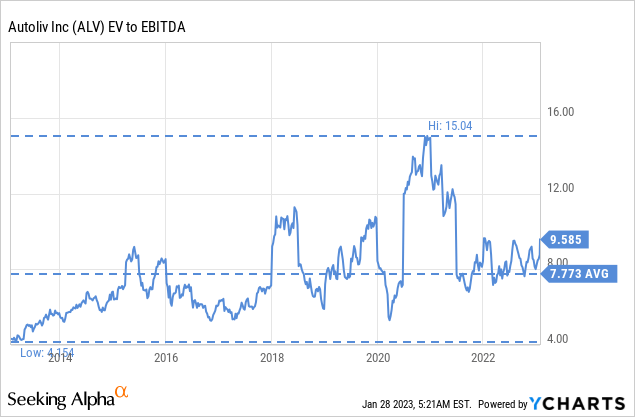

The EV/EBITDA is roughly 23% above the ten year average of ~7.7x, but still at what can be considered a very acceptable multiple for this type of business. With the price/earnings ratio close to 20x, we believe the company is fairly valued given its growth and profitability characteristics.

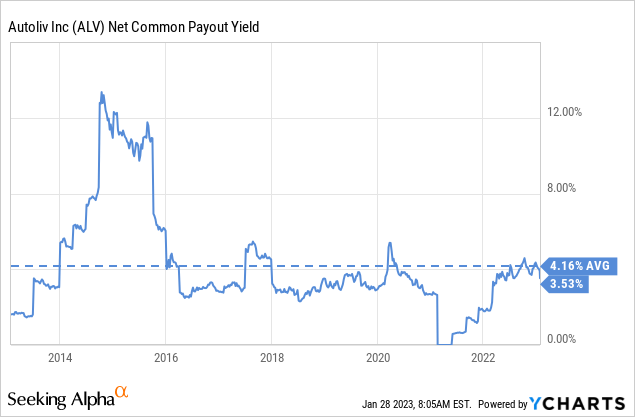

At current prices shares have a dividend yield of close to 3%, and given some share repurchases the company is doing, the net common payout yield is ~3.5%, somewhat lower than the ten year average.

Risks

The main risk we see is that the company operates in a tough industry, with significant cyclicality and relatively slim profit margins.

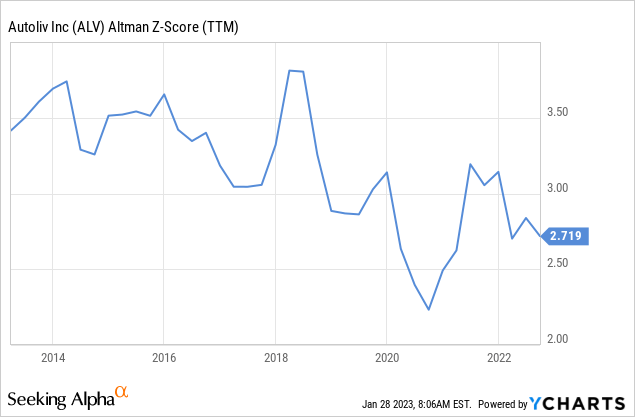

Given that cars are for the most part a discretionary purchase, a recession could have a significant negative effect on sales and profits. While we believe the company’s balance sheet is sufficiently strong to withstand a recession, we would feel more comfortable if its Altman Z-score was above the 3.0 threshold.

Conclusion

Autoliv delivered surprisingly good results, and it has shown resilience against the significant headwinds it has been facing. These headwinds include inflationary pressures, weak light vehicle production, and supply chain issues among others. Despite of these challenges, the company delivered very decent earnings and guidance for 2023. These positive developments have helped eliminate the previous undervaluation of the shares, and we now believe they are trading very close to fair value.

Be the first to comment