FeelPic

Investment Thesis

Eaton Corporation’s (NYSE:ETN) stock is up ~16% since my previous bullish article. The company is continuing to benefit from the strong demand in the industrial, data center, and utility end markets. This led to a healthy order rate and solid backlog levels, which should benefit the company’s revenue in the near term. Given the strong order and backlog levels, the company plans to invest in its supply chain and capacity to efficiently complete its order book. In the long term, ETN should benefit from the secular trends in electrification, digitization, and energy transition as well as from the U.S. infrastructure act. The margins should benefit from restructuring actions, portfolio actions, volume growth, and pricing actions, partially offset by investments in technology and capacity building. The stock is currently trading at 19.13x FY23 consensus EPS estimate of $8.21, which is in line with its five-year average forward P/E of 19.29x. I like the company’s good growth prospects, but believe they are getting appropriately reflected in the stock price at the current valuations. Hence, I am moving to a neutral rating on the stock.

Revenue Outlook

ETN is experiencing strength across all of its businesses, especially in the Electrical Americas, eMobility, and vehicle segments, which is benefiting its volume growth. The company is also effectively managing higher input costs by increasing prices. These tailwinds are more than offsetting the adverse FX impact.

Given the continued strong demand in its end markets, the company reported a strong order rate in the third quarter of 2022, which should help its future revenues. Orders on a 12-month rolling basis in the Electricals business were up 27%, resulting in 75% Y/Y growth in the backlog. The orders in the Electrical Americas segment increased by 36% Y/Y, and in the Electrical Global segment, orders increased by 14% Y/Y, resulting in a backlog increase of 97% Y/Y and 22% Y/Y, respectively. In addition to the strong order and backlog, the project pipeline in the Electrical Americas segment more than doubled due to the solid trends in manufacturing, data centers, industrial, and utility end markets. The orders in the utility markets were up 60% sequentially due to the increased investments in energy transition and grid resiliency.

In the Aerospace segment, the company saw strength in its order rate across its end markets as travel continues to accelerate within the commercial markets. Additionally, defense spending across the world increased post the Ukraine war. On a 12-month rolling basis, aerospace orders increased by 22% while the backlog grew by 17%. The commercial aftermarket orders increased 40% YTD.

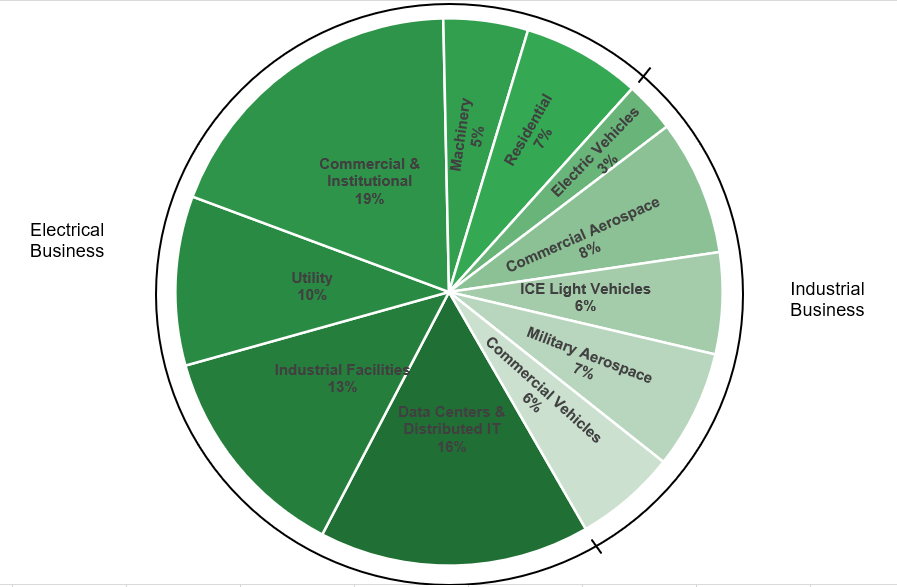

ETN’s end markets (Company data, GS Analytics Research)

Looking forward, I believe the company should be relatively less impacted by the weakening macroeconomic conditions given its strong order rate, secular trends in its end markets, and healthy backlog levels. In its Electrical business, the company is expecting solid growth in data centers, industrial facilities, and utility end markets. Commercial & Institutional (C&I) as well as machinery end-market are also expected to grow modestly due to strong orders from the government and institutions. The growth in these end markets should more than offset the weak residential market.

In the Industrial business, increasing government regulations and incentives, and a large number of new EV introductions should benefit the electric vehicle end market. The commercial aerospace and light motor industries are expected to see a cyclical recovery. The vehicle makers are rebuilding their inventory levels, which were previously impacted by the supply chain challenges. The growth in the aerospace aftermarket and ramp-up in commercial OEM production should drive aerospace markets higher. Approximately 85% of ETN’s end markets are expected to see positive organic growth in 2023.

Given the strong order rate, the company is continuing to invest in capacity and capability and improving the supply chain to complete its orders.

The company’s long-term growth should benefit from the three secular trends in its business. This includes electrification, energy transition, and digitalization. The company booked ~$700 mn of new wins in the last quarter that were tied to this trend. Within Electrification, a large number of manufacturing projects in the U.S. have been announced. This includes new semiconductor facilities, big investments in new electric vehicle manufacturing plants, new EV battery investments, and investments in EV charging infrastructure. In the energy transition business, the shift from fossil to renewable energy is accelerating, and every addition of a renewable resource requires electrical infrastructure. It requires investments in technology to keep the grid stable and investments in batteries to store excess energy. ETN is well positioned with its products to serve this market. Additionally, with the extreme weather conditions and increased demand for energy independence, the company is seeing investments in grid resiliency improvement. Another secular trend is digitalization, which should help drive higher selling prices as the company adds technology to its legacy products and introduces new software platforms. Apart from these secular trends, the company should also benefit from the projects related to the U.S. infrastructure act. This should help accelerate growth over the next three to four years.

I believe the company’s revenue should improve in the near term given the healthy backlog levels and strong order rate. In the long term, the secular trends in the end markets should help drive revenue growth.

Margin Outlook

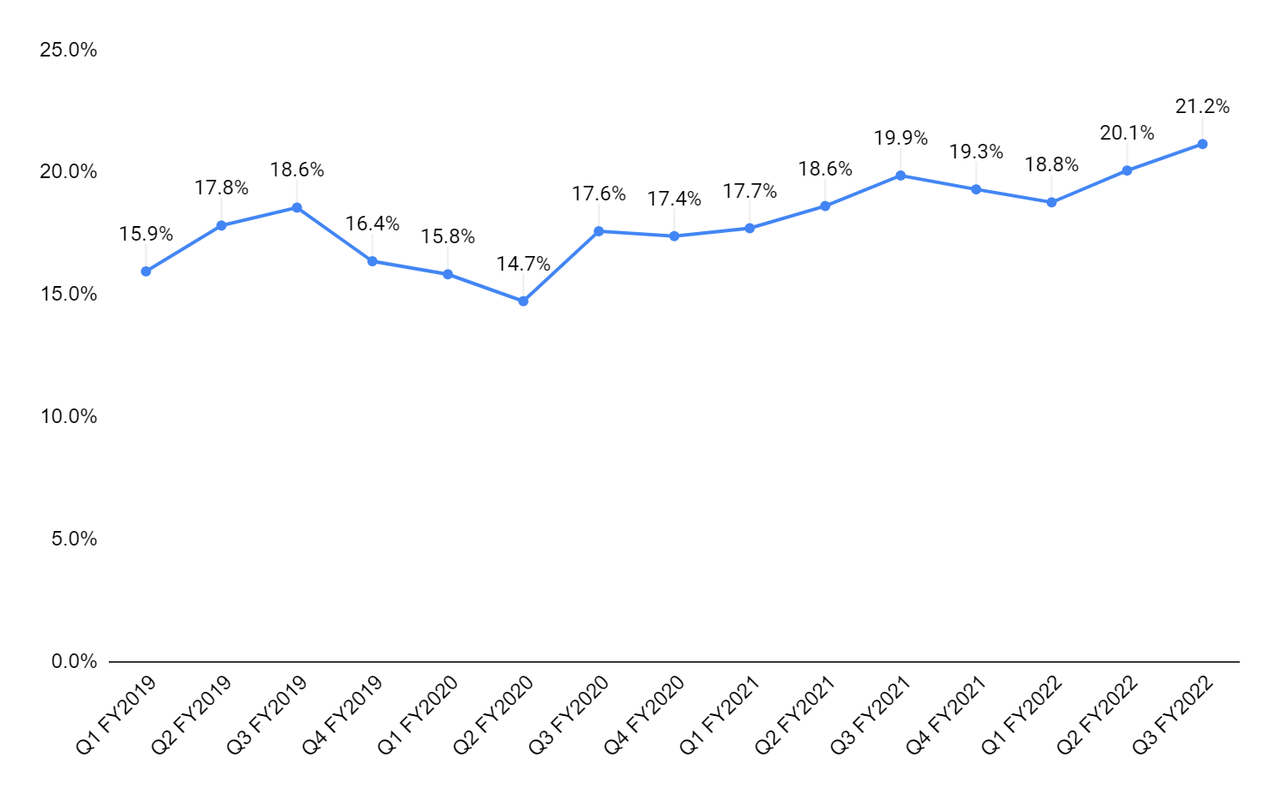

The company’s segment operating margin has been on an upward trend for the last few quarters. This improvement is driven by pricing actions, volume growth, portfolio changes, and restructuring savings. The company has been taking restructuring actions by rightsizing its business and eliminating fixed costs. The company has also been making changes to its business portfolio through acquisitions and divestitures. The transformation of its portfolio has resulted in improved business quality with higher margins. The company acquired Tripp Lite (March 2021), Mission Systems (June 2021), and Royal Power Solutions (January 2022), and divested its Hydraulics business in August 2021.

ETN’s segment operating margin (Company data, GS Analytics Research)

Looking forward, I believe the company’s restructuring actions should continue to benefit the margins. Additionally, the volume growth, along with the pricing actions, should help drive margin improvement in 2023. The company is seeing a reduction in commodity costs such as steel, copper, and aluminum as well as freight costs. This should benefit the gross margins in the coming quarters. While these positives should be partially offset by the company’s future investments in technology and capacity building, I expect the margins to improve in 2023 and beyond.

Valuation & Conclusion

The stock is currently trading at 19.13x FY23 consensus EPS estimate of $8.21, which is in line with its five-year average forward P/E of 19.29x. The company’s revenue in the near term should benefit from a solid end market, healthy order rates, and strong backlog levels. Secular trends such as electrification, energy transition, and digitalization should benefit the company in the long term. The margins should benefit from restructuring actions, portfolio actions, volume growth, and pricing actions, partially offset by investments in technology and capacity building. While I like the company’s growth prospects, I believe they are already reflected in the stock price at the current valuation. Hence, I have a neutral rating on the stock.

Be the first to comment