shaunl

Description

To sum it up, things didn’t go quite as well as planned for E2open (NYSE:ETWO) in 3Q23. As I stated in my original post, I still believe that with ETWO it is better to stay on the side lines for now.

Their revenue was a bit lower than expected, mostly because of some issues with their professional services and a slowdown in the growth of their subscription revenue. But, the good news is that the company is still profitable and they’re holding on to their money pretty well. And, they’re also starting to generate more cash, which is always a good sign. Overall, I still believe that ETWO has a lot of potential in the long run, but there might be a few bumps in the road in the short term. Some of their big customers might be holding off on making big purchases, and there’s also a chance that the market could be affected by an economic recession.

3Q23 Review at a high level

Revenue growth and ETWO stock’s upside are likely to be muted for at least the next few quarters due to a combination of factors, including subscription revenue growth slowing into the single digits and professional services challenges, such as the deliberate shift of some services to SI partners. Despite this, I think it’s great news that E2open’s high gross revenue retention and profitability have been relatively stable, especially now that FCF pressures seem to be easing.

The ETWO long-term opportunity still excites me, and I’m keeping an eye out for catalysts like positive macroeconomic data and continued strong performance from the SI.

3Q23 results

While the $135 million in GAAP subscription revenue was in line with the $134 million predicted by market analysts, the $30 million in professional services revenue was below the $35 million predicted by analysts, resulting in an overall revenue miss of $165 million versus the consensus estimate of $169 million. Gross profit of $114 million on lower revenue was below expectations of $116 million. However, non-GAAP operating income was in line with expectations, coming in at $57 million compared to a consensus of $56 million. This was due to lower than expected spending on research and development and selling and marketing. That aside, with profitability and normalization of AR related to the BluJay acquisition, E2open was able to achieve a multi-year high in FCF of $32 million, marking a positive inflection from 2Q levels.

Overall, E2open’s third quarter revenue was below analyst estimates due to continued difficulties in the company’s professional services division. However, subscription revenues were flat, reflecting the reliability of the firm’s higher-margin subscription business. While organic growth in subscription revenues was 10% in the third quarter, management’s guidance indicates a significant slowdown to 8% in the fourth quarter. I attribute this to the persistent deal delays at major customers, which have pushed some projections out by multiple quarters. Positively, management restated profitability targets, and the third quarter’s FCF improvements encouraged me as the firm effectively stabilized its working capital following a string of negative cash impact quarters.

Performance compared to industry

The performance of ETWO in the third quarter does not surprise me because it is typical of the industry as a whole. ETWO continues to see customers, especially larger ones, critiquing relatively long duration initiatives, which can prolong sales cycles and pushback purchasing decisions. In some cases, deals were delayed by more than a quarter, which could have an effect on subscription revenue growth in the near future.

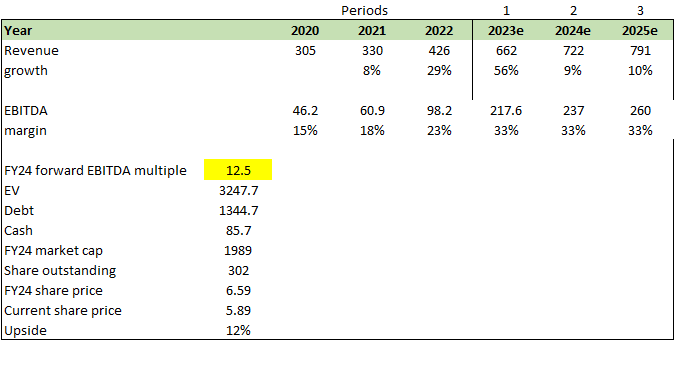

Valuation

After updating my model, I believe ETWO is approaching fair value in comparison to my initial coverage. The previous 19% gain has converged to a 12% gain.

I’ve updated my model to reflect the weaker near-term outlook, which has resulted in a decrease in both revenue and EBITDA. What was not updated was the price at which I expect ETWO to trade. While I believe ETWO could still trade at 12.5x multiple in FY24, I am concerned about what might happen in the near term if all of the headwinds materialize and the market attaches an even lower multiple to it. I’d like to point out that if we enter a full-fledged recession with rising unemployment, near-term performance could be much worse than what management and the market are expecting.

Own estimates

Summary

In summary, the 3Q23 results for ETWO show that the company’s revenue came in lower than expected due to challenges in the professional services segment and a deceleration in subscription revenue growth. However, the company’s profitability and gross revenue retention remained stable, and the company saw a positive inflection in free cash flow. I am still positive on the company’s long-term opportunity but see headwinds in the near-term due to delays in purchasing decisions from larger customers and potential impacts of a recession on the market.

Be the first to comment