Joe Raedle/Getty Images News

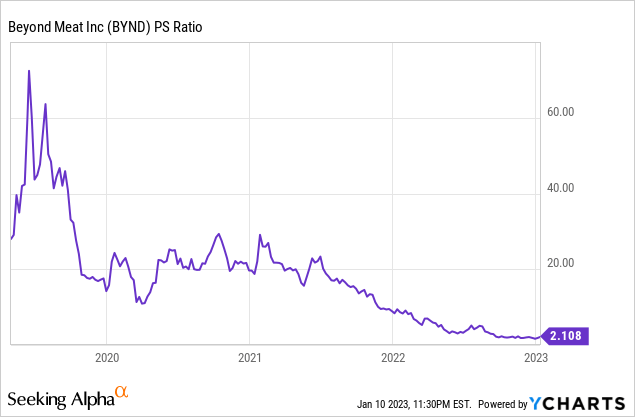

The 78% pullback of Beyond Meat’s (NASDAQ:BYND) common shares over the last 12 months masks the underlying operational progress the company has made to its product line-up beyond just the meat-free burgers it was known for. Beyond Steak, its latest product underlies the constant progress and the ever-growing SKU count of the El Segundo, California-based company. At a market cap of around $900 million, the company is now trading at a price-to-sales multiple of 2.11x, the lowest multiple since its May 2019 IPO.

The bears would be right to call out Beyond Meat for still trading 91% higher than the median PS multiple for its peer group even after the retracement of its commons. Further, whilst the current lows retrospectively look like a good value, this is against previously unrealistic valuation multiples that were propped up by low interest rates and unfettered trading euphoria. The secular growth thesis for Beyond Meat was built on the growing importance of plant-based diets to the overall drive to address carbon emissions and build environmental sustainability.

Plant-based foods continue to grow in importance to the global diet on the back of the increasing awareness of the environmental drawbacks of beef production. Indeed, cattle ranching currently accounts for 80% of deforestation seen in the Amazon. The current orthodoxy is not sustainable against a global population still growing.

Expanding Footprint But Cash Burn Is Tumultuous

To be clear, Beyond Meat is not the only company in this niche with a number of venture capital-funded startups like Impossible Foods competing for market share along with large consumer food companies like Monde Nissin and Tyson Foods. Beyond Meat last reported earnings for its fiscal 2022 third quarter. This saw revenue come in at $82.5 million, a 22.5% decline versus the year-ago quarter. Management pointed to broader economic pressure from inflation and intense competition in their SKU categories. The dual impact of greater competition and slowing consumer demand for more premium price plant-based meals has impacted their grocery sales.

Beyond Meat is now expecting revenue for its full fiscal year 2022 to be between $400 million to $425 million, against a consensus of $426.97 million. This would represent an 8.5% year-over-year decline if revenue comes in at the top end of this range. For some context, Impossible Foods realized a 50% revenue growth rate for its fiscal 2022. Hence, it looks like Impossible Foods has been the most direct beneficiary of the decline in Beyond Meat. However, the company remains private but had IPO rumours floating around last year.

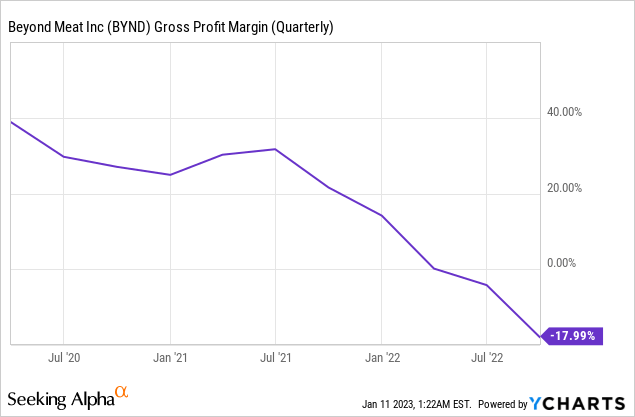

Beyond Meat’s declining gross margins is the main story. The company recorded gross margin of -17.99% for its third quarter, down sequentially from -4.08% in the second quarter. The marked decline highlights just how terrible of a macro backdrop the company is facing with rising product costs from inflation and competitive pressures forcing down a business that once brought in gross margins of around 40% during the early pandemic period.

This has placed its cash flows and overall liquidity position in view. Beyond Meat recorded cash burn from operations of $34.7 million and maintained capex at $18 million during the period. This was against cash and equivalents that finished the quarter at $390.2 million and with long-term debt holding steady at $1.13 billion. Beyond Meat is still expanding its footprint. The company is building on its partnership with McDonald’s in the UK with the Double McPlant, growing in China with the expansion to 100 Metro China grocery stores across 60 cities, and is bringing its Beyond Steak to membership clubs Costco and Sam’s Club. The Beyond Steak has also received good reviews, with most noting its meat-like texture and great taste. These overall initiatives along with continued innovation on the product line up could spark a sales revival and a reversal of the current declining gross margin trend.

Should You Buy Shares This Veganuary?

It’s likely best to avoid the commons until the company shows a clear reversal of gross margins seemingly stuck in a downtrend. Further, with short interest at nearly 40%, bears are betting that there is more downside ahead. The company is pivoting its business model and is aiming to achieve positive flows from operations within the second half of fiscal 2023. This will see more efforts to streamline operations as well as optimization of their production network. This comes on the back of a 19% cut to its workforce, around 200 employees, back in October.

2023 is set to bring more macroeconomic headwinds with inflation remaining at elevated levels until the second half of the year and with a recession broadly expected to hit the global economy including the US. Hence, there might be more pain to come. Beyond Meat’s ability to keep creating and scaling up more Beyond Steaks will form the core part of any eventual recovery.

Be the first to comment