FeelPic

Investment Thesis

e.l.f. Beauty, Inc. (NYSE:ELF) is experiencing healthy demand for its product portfolio. The healthy demand is driven by the company’s ability to deliver product value at all accessible price points as compared to legacy mass cosmetic and prestige brands. This has led to consumers trading down to e.l.f. color cosmetics and e.l.f. Skin products in an inflationary environment. Additionally, the company is benefiting from increased demand and market share thanks to its pipeline of industry-leading innovative products and its capacity to attract and retain existing as well as new customers of all ages and income levels. Furthermore, in the second quarter, the company was able to gain retail space both domestically and internationally, which should further help in market share gain. Looking forward, the company should be able to deliver revenue growth, benefitting from healthy demand due to trade downs and increased consumption rates, the pipeline of new innovations, and retail space gains domestically and globally. In terms of margins, the company should benefit from price increases, cost savings, volume growth, and moderating inflation. However, the company’s growth prospects are already reflected in its valuation at the current price, leaving me on the sidelines. Hence, I have a neutral rating on the stock.

Revenue Outlook

In the second quarter of fiscal 23, e.l.f. Beauty reported revenue of $122.3 million, up 33.2% Y/Y. The company’s sales benefitted from higher demand for e.l.f. color cosmetics products, which are the company’s core products. In addition, the company’s recent innovations along with an increase in Average Unit Retail (AUR) also contributed to the sales growth. The growth in sales was reflected among both international and national retailers. The consumption for e.l.f. cosmetics grew 27% in tracked channels. Moreover, the company is also experiencing healthy demand for its e.l.f. Skin product category due to the rising interest of teenagers in skincare, helping the category grow consumption by 44% in tracked channels.

ELF’s Historic Revenue Generation (Company Data, GS Analytics Research)

The company focuses on five key areas or strategic imperatives to attract healthy demand for its brand and deliver revenue growth. These five strategic imperatives are step-up in digital, leading innovations, driving productivity on a sales-per-foot basis through retail channels, driving brand demand, and cost savings to fuel brand investments.

The three drivers which are helping ELF achieve its strategic imperatives are value proposition, leading innovation, and digital-first marketing. The first driver of its strategic imperatives is the value proposition. The company makes premium quality products which are inspired by the best products in prestige categories (ELF calls them “holy grail” products) and makes them available at accessible price points. The company is benefiting from trade down as consumers prefer the holy grails and the value they provide over prestige and legacy mass brands. The average e.l.f. price point today is slightly more than $5, compared to around $9 for legacy mass cosmetics brands and more than $22 for prestige brands. This pricing strategy, unlike many of its peers, focuses on everyday value rather than broad-based promotions.

The second driver is leading innovations. The company constantly delivers new innovations in its seven segments – brushes, primers, setting sprays, eyeshadows, concealers, bronzers, and sponges – which has helped it gain market share in these categories over the last several years. Some examples of the company’s leading innovations include the Power Grid primer at $10 versus a prestige equivalent at $34 and the recently launched Halo Glow liquid filter at $14 versus the prestige equivalent at $46. The putty blush and putty bronzers in blush and bronzer category have also received industry recognition.

The third driver is the company’s ability to attract and engage consumers through digital-first marketing. The company constantly engages consumers and has gained market share through multiple social platforms. In August, e.l.f. Beauty became the first major beauty brand on BeReal, a reality-based photo-sharing platform that’s rising in popularity among the younger generation or Gen Z and became the #1 brand among teenagers of all income groups. Moreover, the value proposition and innovations at reasonable prices have led the brand to gain market share among millennials and Gen X.

Investor Presentation

In addition to healthy demand, these three strategic drivers have helped e.l.f. Beauty to gain more retail space domestically as well as internationally. The company is expanding space with both Walmart (WMT) and Target (TGT) in spring 2023 along with the space gains previously announced with CVS (CVS) in fall 2022 and spring 2023. Internationally, the company is expanding space with Shoppers Drug Mart in Canada for spring 2023 along with the space gains previously announced with Superdrug in the U.K. for fall 2022. Moreover, the company had recently added a third-party manufacturing facility that is Fair Trade Certified. This has made the company become the first beauty company to have productions that are Fair Trade Certified, along with value proposition at accessible price points. These combinations in its product category should help in delivering growth and gaining market share in the coming years.

Looking forward, I am optimistic about the company’s ability to deliver revenue growth in the second half of fiscal ’23 and beyond. The company should benefit from healthy demand due to trade downs from legacy mass cosmetics and prestige products to the company’s product portfolio. In addition, the company should be able to grow market share and consumption rate through its pipeline of new innovative products along with the Fair Trade Certification on its products. Moreover, the company has a history of delivering good ROI on its marketing investments, which are above the industry benchmark in terms of gross sales per dollar invested. In the second quarter, the company raised its outlook for marketing spending, which should help attract and engage new and existing consumers and increase market share in the second half of fiscal ’23. The higher ROI on marketing spend, healthy demand due to trade downs and increased consumption rates, and the pipeline of new innovations along with space gain in the U.S. and globally should help the company in delivering revenue growth in the second half of fiscal 2023 and beyond.

Margin Outlook

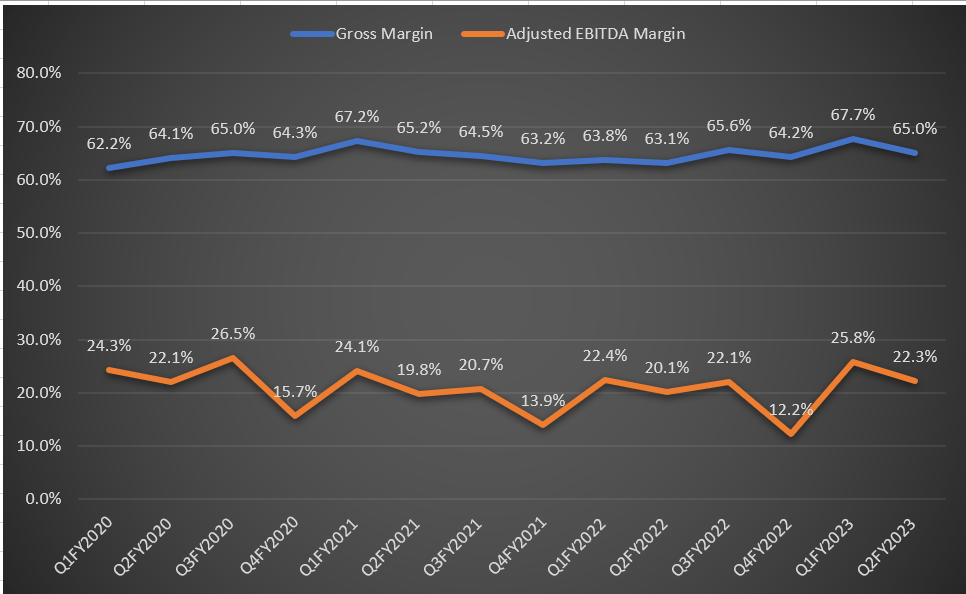

In the second quarter of fiscal 2023, e.l.f. Beauty delivered a gross margin of 65%, up 190 bps Y/Y. The increase in gross margin was a result of price increases, cost savings through supply chain optimization, and a favorable product mix. The increase in gross margin more than offset the impact of inventory adjustments and higher transportation costs in the quarter. Turning to adjusted EBITDA, the company delivered adjusted EBITDA of $27 million, up 47% versus last year and the adjusted EBITDA margin was 22.3%, up 220 bps Y/Y. The increase in adjusted EBITDA margin was due to higher leverage generated from volume growth and lower marketing and digital spending as a percentage of sales due to better-than-expected top-line growth.

ELF’s Historic Gross and Adjusted EBITDA Margin (Company Data, GS Analytics Research)

Looking forward, I believe the company should be able to deliver gross and adjusted EBITDA margin growth. Gross margin should benefit from price increases, lower transportation costs due to moderating inflation, and a margin-accretive product mix. In addition, the company has demonstrated its ability to expand gross margin through cost savings in its supply chain. For example, the company has a hybrid supply chain model that combines outsourced asset-light manufacturing in China and multiple distributional centers. This should continue to benefit the gross margin moving ahead. For EBITDA margin, management expects the adjusted EBITDA margin to expand by 50 bps for fiscal year ’23. Beyond fiscal 2023, the adjusted EBITDA margin should continue to benefit from higher volume leverage from sales growth, gross margin expansion, and leverage generation from non-marketing SG&A expenses.

Valuation and Conclusion

e.l.f. Beauty is currently trading at a P/E of 49.15x FY ’23 consensus EPS estimate of $1.12 and 44.41x FY ’24 consensus EPS estimate of $1.24. The stock is trading at a significant premium to its historic 5-year average forward P/E of 34.15x. Looking forward, I believe the company’s five strategic imperatives along with healthy demand, space gains, moderating inflation, price increases, and favorable product mix should help the company deliver growth in the second half of fiscal ’23 and beyond. However, the company’s growth prospects are already reflected in its higher valuation at the current price, Hence, I would prefer to be on the sidelines and have a neutral rating on the stock.

Be the first to comment