KanawatTH

Written by Nick Ackerman, co-produced by Stanford Chemist. This article was originally published to members of the CEF/ETF Income Laboratory on December 27th, 2022.

DoubleLine Income Solutions Fund (NYSE:DSL) has once again paid out a special year-end distribution of $0.196. These are required when a fund earns too much and needs to distribute out the excess. A fund must distribute almost all of its income and capital gains to maintain regulated investment company compliance.

DSL had a special last year, which is interesting to note because it was also the year they cut their distribution. That was after maintaining it for quite a few years before the cut. The latest special was about half of the last year, likely due to net investment income coming down overall. The fund sports a high distribution yield that’s fully supported by net investment income, but that coverage has slid with lower NII year-over-year.

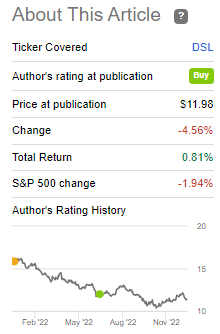

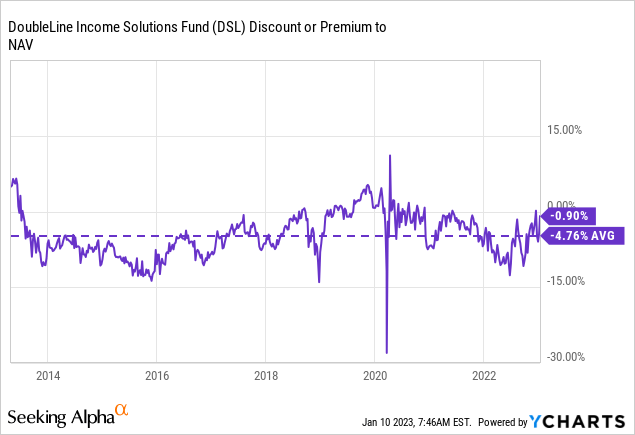

Since our last update, shares have held up relatively well. However, the slight positive results on a total return basis are simply due to discount compression. The fund is not as attractively valued as it was previously. The 1-year z-score has gone from about -2.5 to around 1 now, reflecting this move.

DSL Performance Since Previous Update (Seeking Alpha)

While the fund itself isn’t showing a deep discount, the underlying holdings are. That’s where an interesting dynamic comes in for fixed-income CEFs, as you can get discounts on discounts. Ultimately, if par is returned back when these bonds mature, there could be quite a bit of upside potential.

As it is an actively managed fund, the likelihood of maintaining the position until that happens isn’t guaranteed. Being actively managed means we don’t know exactly what they will do; therefore, it is incalculable on the exact benefit in the future. The average maturity in their portfolio is also ~8.5 years, so an eternity in the investing world.

The Basics

- 1-Year Z-score: 2.03

- Discount: 0.90%

- Distribution Yield: 10.94%

- Expense Ratio: 1.51%

- Leverage: 23.66%

- Managed Assets: $1.581 billion

- Structure: Perpetual

DSL has an investment objective to “provide a high level of current income, and its secondary objective is to seek capital appreciation.” The fund is invested “in a portfolio of investments selected for their potential to provide high current income, growth of capital, or both. The fund may invest in debt securities and other income-producing investments anywhere in the world, including in emerging markets.”

The fund’s leverage is rather moderate. However, any leverage is going to negatively impact the fund in a down market and positively impact it in a rising market.

Additionally, with interest rates rising, there is a big focus on the costs of leverage. This has a direct impact on the fund’s NII as NII is simply the income received from interest and dividends in the fund minus the expenses. When expenses are rising, that is taking a larger bite out of the income left over for shareholders.

Interest for this fund’s borrowings is one-month LIBOR plus 0.70%. They also mention that “under certain conditions, interest rate can be charged at the rate of the federal funds rate plus 0.55%.”

The other big impact of leverage here is increasing or decreasing leverage. In the case of DSL, they’ve been deleveraging for most years. That includes 2022, which now puts it at the lowest level of leverage utilization – impacting NII by reducing the overall amount of income-generating assets in the portfolio.

DSL Leverage Levels (DoubleLine)

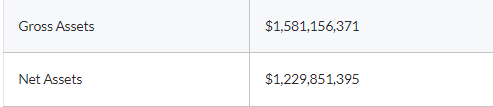

That was at the end of their fiscal year-end. Since then, it seems that they have deleveraged even further. Comparing the gross assets to the net assets would mean that leverage is now down around $351.3 million, or the website could be showing an error.

DSL Assets (DoubleLine)

Deleveraging isn’t necessarily a bad thing, especially when things are going south. Deleveraging can reduce further relative downside had they remained with higher leverage. If they can time it right, they could benefit back from a rebound when times are better. Given the trajectory of lower and lower leverage, I wouldn’t necessarily count on that happening over the long term.

Performance – Discount Narrows

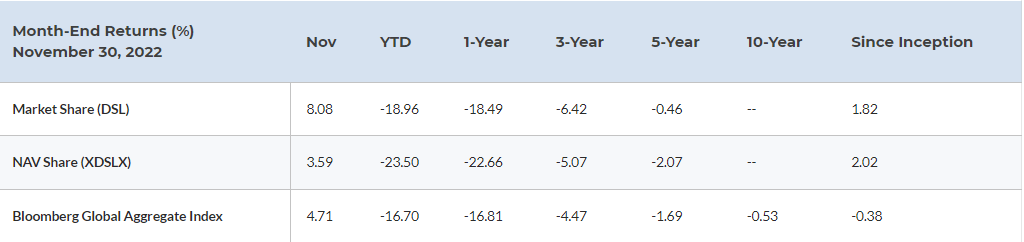

The fund compares itself to the Bloomberg Global Aggregate Bond Index, which seems like a good place to start, providing some context of relative movement. However, I would note that the fund holds a heavy allocation specifically to emerging markets and their debt.

DSL Annualized Returns (DoubleLine)

For the most part, DSL hasn’t done well, but neither has the index it benchmarks against.

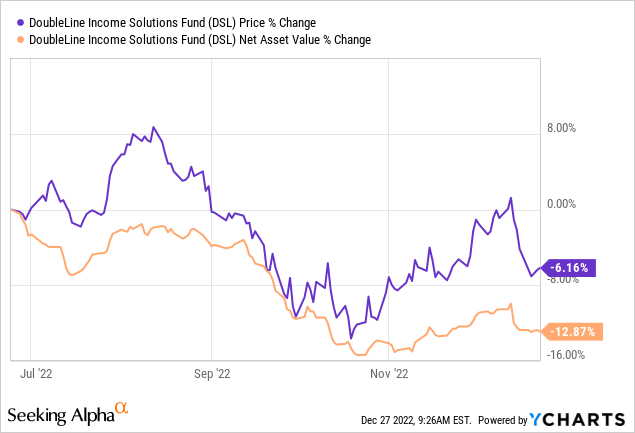

One reason to buy closed-end funds over individual stocks or ETFs would be to get funds at some large discounts. Unfortunately, the benefit of buying DSL (the discount) has also closed quite significantly since our previous update. I highlighted above that DSL has shown some slightly positive total return results since our previous update. However, the NAV has actually declined quite considerably while the share price has held up much better.

Ycharts

When that happens, a fund’s discount narrows. That’s when a CEF becomes less attractive overall. In the last week, DSL’s discount has narrowed considerably. It is now trading above its longer-term average.

Ycharts

Distribution – ~11% Distribution Rate Fully Covered, For Now

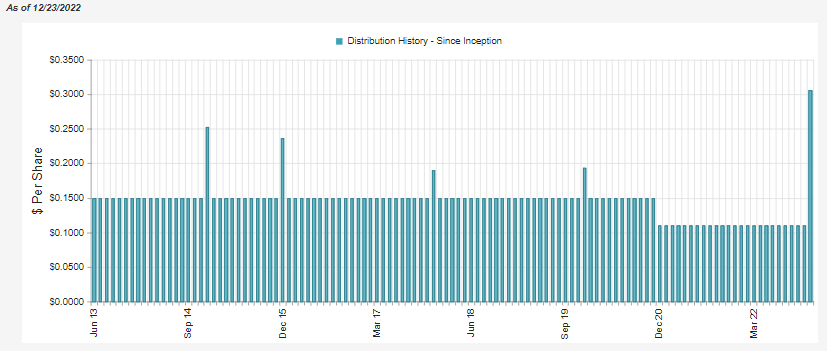

With a 10.94% distribution rate, that’s rather attractive. Due to a shallow discount, the NAV distribution rate is quite close at 10.84%. A year ago, those types of yields would have sent up a red flag. Now that yields have risen due to interest rate increases, it isn’t an alarming sign. (CEFConnect’s chart doesn’t reflect the special paid last year, for whatever reason, it was missed.)

DSL Distribution History (CEFConnect)

This is reinforced by the fact that the fund’s distribution has been fully covered with NII. Although, when looking at the annual report, it might not appear that way at first.

DSL Annual Report (DoubleLine)

The above shows NII against distributions to shareholders at around 85%. However, that’s also reflecting the year-end that was paid out of $0.411 last year. When taking that out, the fund pays an annualized $1.32, while they pulled in $1.47 per share of NII for the fiscal year.

The main problem is that NII decreased from last year’s $1.66 per share. That means the amount of distribution coverage has fallen quite meaningfully. That’s reflected in the annual report above, seeing NII go from ~$170 million to ~$150 million.

The decrease is a culmination of deleveraging and higher leverage expenses. The fund carries some bank loans, CLOs and other floating rate debt, but it doesn’t appear enough to offset the declines elsewhere. If they have deleveraged further, then the current 111% NII coverage is likely no more.

Total investment income for the last fiscal year came to $183.889 million, with interest expenses of $10.340 million. That’s compared to fiscal 2021, which saw $203.233 million TII and interest expenses of $5.913 million. They were deleveraging but still paid more in interest expenses as interest rates rose.

DSL’s Portfolio

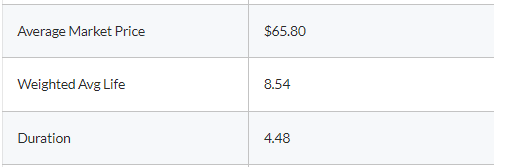

The fund might not be as attractively discounted as it was previously, but the fund’s average market price coming in at $65.80, suggests that the debt they hold is severely depressed in price. This was a drop from the $79.18 it was earlier this year – thus, why we’ve seen NAV take such a hard hit.

DSL Portfolio Stats (DoubleLine)

There are two main reasons why their debt holdings are taking such a big hit. The first would be the most obvious; interest rates are rising. Interest rates rising push yields higher on risk-free debt, making riskier debt holdings less attractive. Investors sell off the riskier debt in favor of the now higher-yielding risk-free debt, and then the yields on riskier debt rise as the prices are pressured. Thus, making them once again more attractive until rates rise again.

The problem with 2022 isn’t necessarily rising interest rates, but not knowing where the end is. Every Fed meeting seems to extend the terminal rate further and further as inflation stays elevated. It’s akin to taking a bandaid off slowly instead of just ripping it off all at once. Their portfolio duration is 4.48 years. Theoretically, every 1% increase in interest rates should send their portfolio down 4.48%.

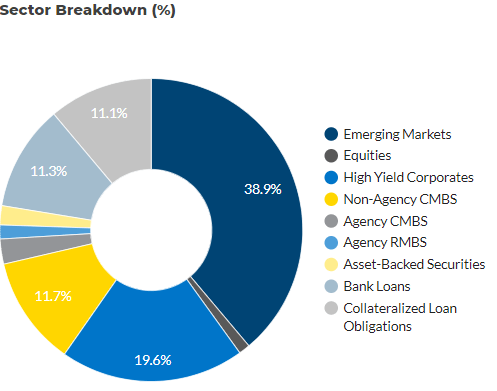

The second big consideration for debt prices here is credit risks. If we enter a recession year, as most expect, defaults will rise. DSL’s portfolio is heaviest in emerging markets, so its prospects are less attractive. At least in terms of credit quality due to the overall financial stability of the economies that they are invested.

DSL Sector Allocation (DoubleLine)

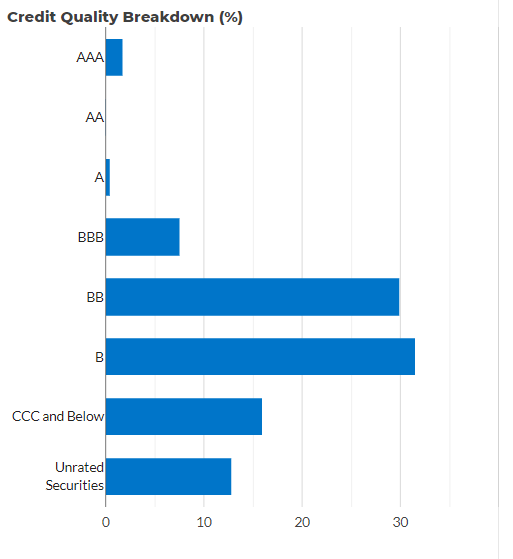

The bulk of their portfolio is below-investment grade. In particular, they have a nearly 16% allocation to CCC and below.

DSL Credit Quality (DoubleLine)

CCC debt is the type of rating that I like to say; if the wind blows in the wrong direction one day, they default or go bankrupt. They are essentially the types of debt issued by entities where just about everything has to go right.

It isn’t all bad news investing in junk because the prices are certainly reflecting some significant headwinds already. So that makes the current price fairly attractive – even if DSL’s discount isn’t attractive at this time.

Another point is that they generally pay higher yields and have shorter maturities, which makes them relatively less interest-rate sensitive. That’s what the portfolio’s duration tells us; while it isn’t 0, it’s certainly lower than investment-grade debt. If we look at iShares iBoxx Investment Grade Corporate Bond ETF (LQD), the duration of that fund is 8.40 years.

Some of their debt – primarily the CLO, bank loans and some of the MBS securities – is floating rate based. That means as interest rates rise, they should see higher income from these. It might not have seemed to help the fund on the surface in terms of coverage since TII still dropped. However, if that hadn’t been the case, TII and NII would have dropped even further.

Conclusion

DSL continues to cover its distribution. However, the coverage has weakened, which isn’t a great sign. The year-end distribution was nice to see, but a reduction from last year also tells of the coverage’s direction. The portfolio itself is heavily discounted while the fund is trading about where it has historically. Overall, that doesn’t make me excited enough to still consider this fund a buy. I’d be looking to see if that discount at the fund level would widen out further before finding it more attractive again.

Be the first to comment