welcomia/iStock via Getty Images

Dragonfly Energy’s (NASDAQ:DFLI) common shares fell by just under 41% yesterday in a heavy slump that mirrored the wider trading of its peers and other climate economy stocks including FuelCell Energy (FCEL) and Amprius Technologies (AMPX). These both fell by 3.7% and 20.7% respectively. Dragonfly designs and manufactures high-performance lithium-ion batteries for a variety of applications. The company has developed what management describes as a new manufacturing process for producing electrodes for batteries that do not involve the use of solvents or the need for ovens or vacuum conditions.

Coinciding with their slump, the company released a newswire yesterday on being granted a new US patent covering a manufacturing process for their solid-state batteries. Solid-state batteries hold a lot of promise as the full replacement of a liquid electrolyte with a solid electrolyte will help create batteries that are significantly more energy dense, non-flammable, and faster charging than other lithium-ion battery chemistries. This is not a small field with recent public companies QuantumScape (QS), Solid Power (SLDP), and Mullen (MULN) all chasing the solid-state dream together with larger players like Toyota (TM) and dozens of private battery startups and academic institutions.

Dragonfly Energy Is An Uncertain Contestant In A Crowded Race

Dragonfly went public two months ago via a combination with a blank check company at a pro forma enterprise value of $500 million. This would be one of the few SPAC deals to close in a year that saw the once insatiable go-public tool collapse into just a handful of deals. The combination with Chardan NexTech Acquisition 2 Corp was completed with 79.4% of shareholders electing to redeem their shares. This reduced the money available in its trust by $21.4 million. However, the company was able to secure a $75 million loan to support the deal and refinance existing debt. Dragonfly also received $15 million via a stock purchase agreement with THOR Industries (THO). The partnership with THOR, a manufacturer of recreational vehicles, will see Dragonfly expand on a relationship supplying its lithium-ion batteries to THOR’s RV brands.

Reno, Nevada-based Dragonfly also expects to launch a $150 million equity facility backed by Chardan. This will see the company raise capital through the periodic sale of its common shares but has been confusingly billed as a Chardan equity facility rather than what is essentially a DFLI secondary offering. In total, Dragonfly expects to gain access to $250 million in gross proceeds by going public, the bulk of this obviously coming from stock sales which management stated will start once trading on Nasdaq commences.

Unlike some of its peers, Dragonfly already generates revenue. The company had sales of $78 million for its fiscal 2021 and adjusted EBITDA of $8.7 million in the same year, both representing a compound annual growth of 80% from 2018. Dragonfly last released earnings covering the nine months to the end of September 30 2022. This saw revenue come in at $66 million, up by 14.2% from $57.8 million in the year-ago comp. However, profitability dropped with gross profit margin falling by 1,100 basis points to 29.6% from 40.6% for gross profit of $19.6 million. This was down from $23.5 million in the year-ago comp. The company also realized a net loss of $7.5 million during the period, a marked deterioration from a profit of $4.4 million in the year-ago comp.

The bulk of revenue is currently generated from sales of their batteries to RV OEMs like THOR with the Keystone and Airstream brands being flagged as significant customers. The company also retails a line of deep-cycle lithium-ion battery packs under its Battle Born brand direct to consumers. Deep-cycle batteries are essentially designed to be regularly deeply discharged using most of their capacity. Hence, replacing traditionally deep-cycle lead-acid batteries with lithium-ion brings not only a longer life span with more than 16x more cycles, but it’s also more environmentally friendly and more reliable.

Hence, the slowdown in revenue compared to their historical CAGR can likely be partially explained by a decline in year-over-year RV sales as per THOR’s second and third quarters for fiscal 2022. I’d imagine RVs to be quite a discretionary-led spending item and the declining macroeconomic backdrop as well as higher auto interest rate would have driven a decline in sales.

The Solid-State Battery Hype

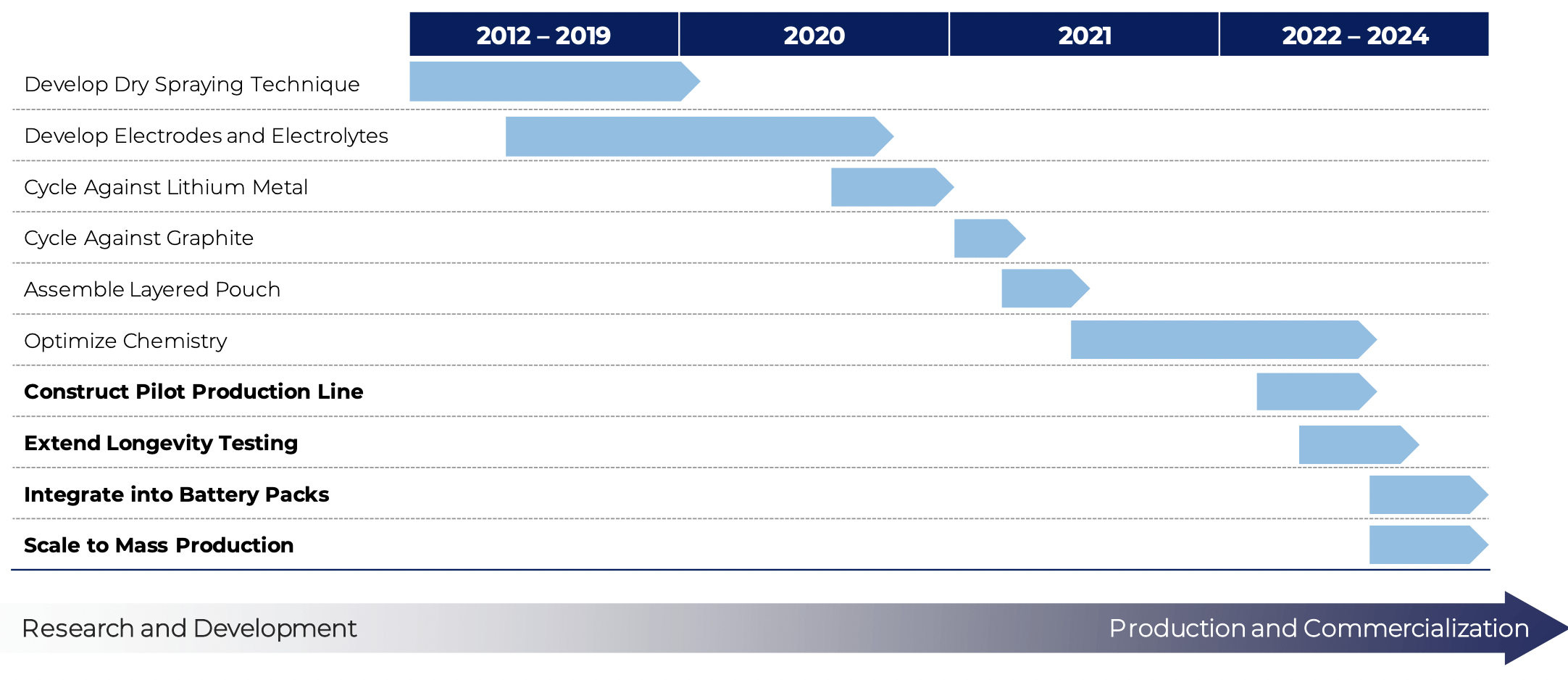

Dragonfly being granted a solid-state battery-related US patent would have likely sparked a rally in their common shares under more euphoric market conditions. Indeed, pre-revenue peer QuantumScape once had a market cap larger than General Motors (GM). The patent covers “systems and methods for dry powder coating layers of an electrochemical cell” and is described by management as a major step towards achieving their goal to commercialize solid-state batteries. Dragonfly quite ambitiously anticipates mass production by 2024, ahead of QuantumScape and Solid Power which are both targeting 2025 and 2026 respectively.

Dragonfly Energy

It’s important to note that Dragonfly does somewhat differ in its solid-state efforts as it is targeting other markets like deep cycle storage for grid, residential and industrial applications. Manufacturing a solid-state battery is no easy feat with lithium dendrite growth being a fundamental problem that has hamstrung efforts by similar companies. This would see Massachusetts-based SES AI (SES) lay off its solid-state battery manufacturing team with the CEO describing the technology as challenging to manufacture and impossible to commercialize.

Dragonfly’s drop yesterday likely reflects angst over its solid-state plans in a market that retreated on better-than-expected economic data. Interest rates will remain elevated for longer and sales of RVs are likely to remain depressed. The company has to be commended for finding itself a niche in the crowded lithium-ion battery space but there will likely be more downside ahead. I’m neutral on the stock.

Be the first to comment