gorodenkoff

Dover’s Drivers And Challenges

Dover Corporation’s Filings

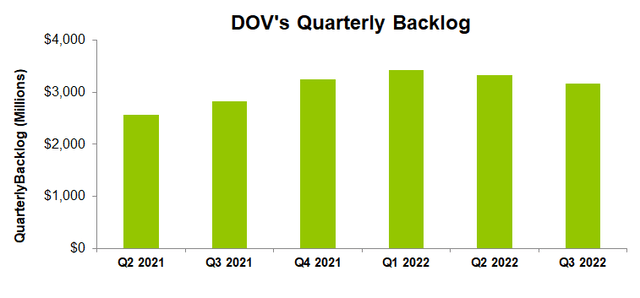

My previous article discussed Dover Corporation’s (NYSE:DOV) strengths and weaknesses. The company is bolstering its portfolio through bolt-on acquisitions. The Malema acquisitions have added the biopharmaceutical, semiconductor, and industrial end markets to its kitty. Although the order backlog decreased in Q3, ~70% of its Q4 revenue is booked with a healthy book-to-bill ratio. I expect the current improvements in the supply chain and available production capacity to meet demand in 2023.

However, DOV faces several challenges – an incoming global recession being the primary one. Given substantial working capital requirements, cash flows depleted severely in 9M 2022. Now, the company may reduce output in several businesses to draw down inventory balances. The stock is relatively undervalued versus its peers. Nonetheless, given the constraints in the near-to-medium-term, I would suggest investors hold the stock for now.

Acquisitions And Other Strategies

Dover Corporation’s product portfolio was substantially boosted through the Malema Engineering acquisition in July. Since then, it has continued to pursue bolt-on acquisitions. It brought in high-precision flow measurement and control instruments used in the biopharmaceutical, semiconductor, and industrial sectors. In December 2022, it acquired Witte Pumps & Technology which manufactures precision gear pumps for the chemical, plastic & polymer processing, food & beverage, and pharmaceutical industries.

Tradingeconomics.com

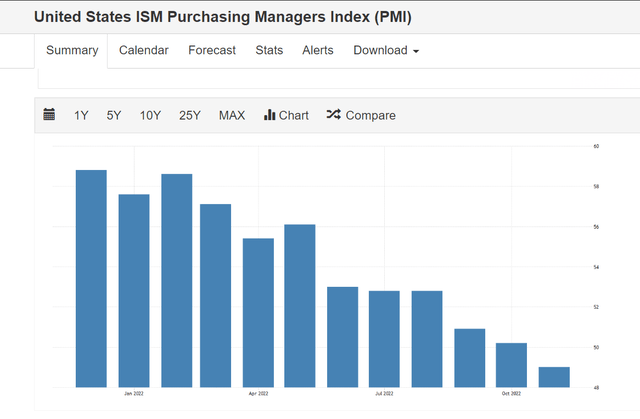

Two key issues that crippled the company’s growth and operating margin were macroeconomic uncertainty and supply chain disruptions. Several indicators signal that a recession is around the corner, as production and inventories have registered low growth in recent months. In November, the ISM Manufacturing PMI declined to 49, indicating a contraction in factory activity, lower orders, and supply deliveries. The U.S. unemployment rate again kept low (3.7%) in November, down from 4.2% a year ago. According to the FRED economic data, the new privately-owned housing units decreased by 16% in November 2022 versus a year ago. To counter this, it is deploying capital to drive productivity and expand capacity. So, the indicators signal a resilient outlook for the company in the short term.

The company may reduce output in several businesses to draw down inventory balances. It may also initiate cost-reduction measures. The current improvements in the supply chain and available production capacity would match production to meet demand in Q1 2023. The strengthening of the US dollar posed another challenge for DOV. The company estimates it can shave off $0.37 of its earnings in FY2022. To mitigate that, it has deployed several short-term cost containment measures, particularly in the Clean Energy & Fueling segment. These actions can offset $0.23 of net earnings during the year.

Bookings And Indicators

Dover Corporation’s Filings

In Q3 2022, DOV’s total backlog was 4.3% lower than a quarter ago. However, compared to a year ago, it was 12% higher. Its backlog allows it to manage working capital by adjusting production to the quarterly demand fluctuation. Approximately 70% of its Q4 revenue was booked at the end of Q3. In the key operating segment, its book-to-bill ratio varied between 0.91x to 1x in Q3, which indicates the steadiness in backlog points to a positive outlook in 2023.

In December, the company and Microwave Products Group received a U.S. DoD contract for $53 million to provide antenna interface units, communications trays, and other parts and services for the P-8A Poseidon communications suite. In 2023, its portfolio will have a healthy mix of short and long-cycle elements.

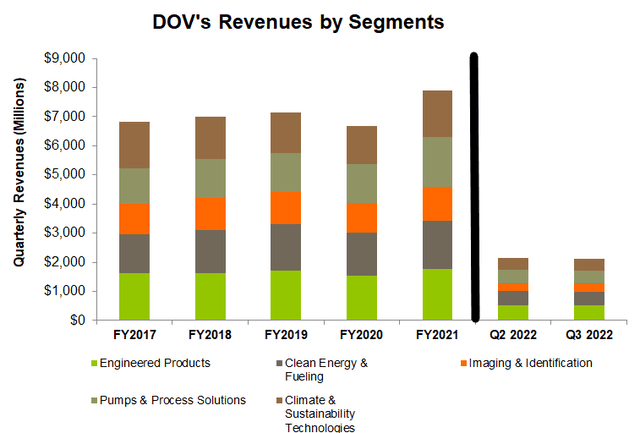

Performance: Engineered Products And Clean Energy & Fueling

Seeking Alpha

The Engineered Products segment accounted for 24% of Q3 revenues. Quarter-over-quarter, revenues in this segment did not change in Q3, although the EBITDA margin expanded by 160 basis points. Led by the capital investments in the prior quarters, the company’s productivity improved while the e-commerce platforms started driving aftermarket volume. In Q4, the company expects the margin to expand further due to higher volumes and better price-to-cost dynamics.

However, the Clean Energy and Fueling segment saw a 6% revenue dip in Q3 compared to Q2. Customer construction delays in North America and a weakening economy in Asia and Europe caused an activity drawdown. Despite that, the segment witnessed a steady performance in vehicle wash, clean energy components, and fuel transport, which partially offset the headwinds. So, the segment’s EBITDA margin decreased modestly in Q3.

The Outlook In Other Segments

The Pumps and Process Solutions segment saw a nominal topline fall (2% down) in Q3. Activity in the biopharma components business contracted the most as COVID vaccine demand receded. However, the non-biomedical and thermal connector business saw steady sales growth during the quarter. Higher demand for data center and electrical vehicle charger cooling applications will lead the segment to run up. The crude oil price steadied in Q4 after a moderation in Q3. The completed wells increased rapidly, while the DUC (drilled by uncompleted) wells declined. I think the segment will see growth in the coming quarters.

DOV’s Imaging & ID segment recovered in Q3 as volumes increased. Improved electronics input availability since the lift-off of COVID- protocols has eased the pressure on marking & coding printers and spare parts. This allowed pricing improvement in the segment, leading to a 410-basis point enhancement in the EBITDA Margin in Q3 compared to Q2. However, the company generated significant revenue in the non-U.S. dollar, which was adversely affected by the foreign exchange headwind in Q3.

Climate & Sustainability Technologies saw limited-to-no revenue and EBITDA growth among its segments in Q3 versus Q2. The company’s management sees significant growth opportunities and invests in capacity expansion programs and CO2 systems, and heat exchangers.

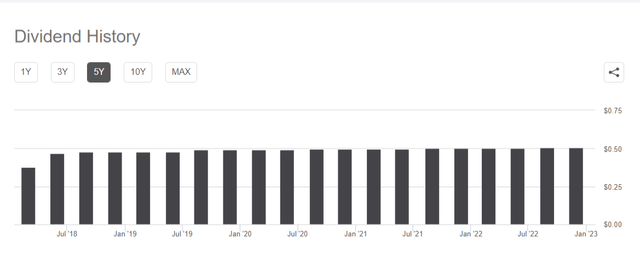

Steady Dividend

Seeking Alpha

In November, DOV announced a dividend of $0.505 per share, translating into a 1.49% forward dividend yield. Snap-on Incorporated’s (SNA) forward dividend yield is higher (2.84%), while Fortive Corporation’s (FTV) dividend yield is lower (0.44%).

Cash Flows And Debt

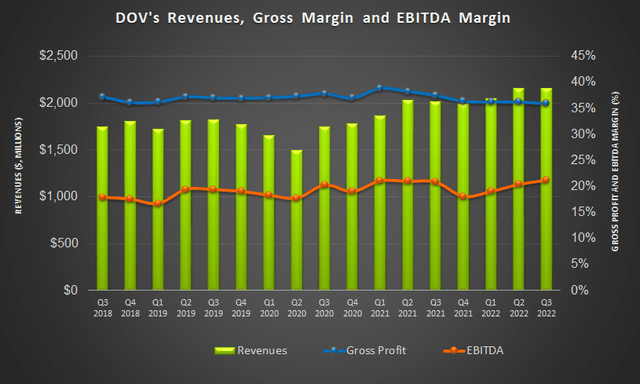

In 9M 2022, DOV’s cash flow from operations (or CFO) decreased by 41% compared to a year ago. Although year-over-year revenues increased mildly, a rise in inventory to service higher activity and mitigate potential inventory shortages led to the CFO’s fall. Higher compensation payouts also increased working capital requirements. Capex, excluding the acquisition part, went up in 9M in 2022, leading to a 54% decrease in free cash flow in the past year.

DOV’s liquidity (undrawn revolving credit facility plus cash) totaled $1.3 billion as of September 30. Its debt-to-equity ratio (0.91x) is higher than its competitors (SNA, FTV, and Ingersoll Rand Inc. (IR)) average of 0.32x. Since December 31, 2021, the company’s stockholders’ equity has decreased by $198.1 million due to share repurchases and dividends.

Returns Potential And Relative Valuation

Seeking Alpha

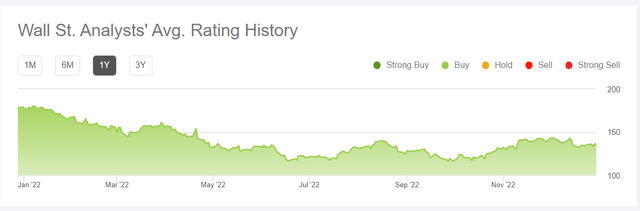

According to Seeking Alpha, ten Wall Street analysts rated DOV a “buy” in the past quarter (including a “strong buy”). Eight of them recommended a “hold.” None rated it a “sell.” The Wall Street analysts’ estimates suggest a 12% upside at the current price.

Seeking Alpha

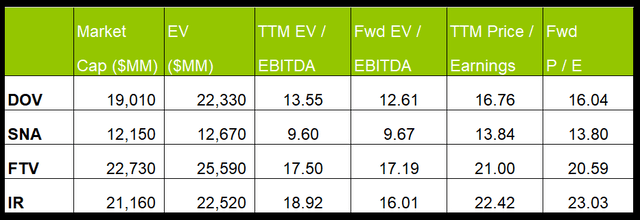

DOV’s forward EV-to-EBITDA multiple compresses more steeply versus the current EV/EBITDA than its peers, which implies its EBITDA can increase more sharply than its peers in the next 12 months. This typically results in a higher EV/EBITDA multiple. The stock’s EV/EBITDA multiple (13.5x) is lower than its peers’ (SNA, FTV, and IR) average of 15.3x. So, the stock is relatively undervalued versus its peers.

Why Do I Change My Rating?

I was positively optimistic about Dover in my previous article, where I explained:

While the supply chain disruptions have long pestered the company, it appears the issues are receding. The end of the pandemic has opened up the demand side, as reflected in the increased backlog and order rate over the past year. Strong US demand for garbage collection vehicles and parts has increased its sales. Higher productivity and improved price-cost spread would be margin accretive in 2H 2022.

Although the stock is still attractive from the valuation standpoint, I would exercise more caution. At this moment, some of the issues have weakened, namely, the supply chain problem and a few struggles appear to be on the near horizon. The recession and demand drawbacks are among the emerging issues.

What’s The Take On DOV?

Seeking Alpha

The inorganic growth route has bulked up Dover Corporation in recent times. It has added biopharmaceutical, semiconductor, and industrial markets through these purchases. Among the recent purchases are Malema Engineering and Witte Pumps & Technology. Although the order backlog decreased in Q3, ~70% of its Q4 revenue is booked with a healthy book-to-bill ratio.

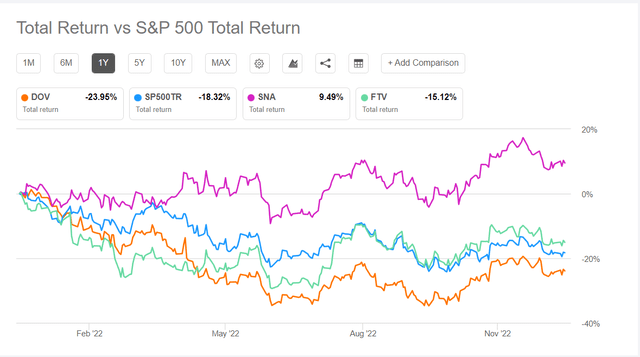

While the supply chain issue is fading, the global recession seems to be underway. Although the Dover Corporation balance sheet is leveraged, it has robust liquidity. So, it performed in line with the SPDR S&P 500 Trust ETF (SPY) in the past year. Given the relative valuation multiples, investors may hold Dover Corporation stock at this level.

Be the first to comment