claudiodivizia/iStock via Getty Images

Alpine Income Property Trust, Inc. (NYSE:PINE) is a triple-net lease retail REIT externally managed by CTO Realty Growth (CTO). It boasts 100% occupancy at its recent update, with an implied cap rate of 7.3%.

56% of its annualized base rent (ABR) is accounted for by ten of its so-called “top tenants,” including Walgreens (WBA) at 11% of its ABR. The company’s active management of its portfolio termed “accretive retail asset recycling,” is a mainstay of the REIT’s strategy.

Accordingly, management highlighted that it had proved the soundness of its strategy, as it has achieved an average positive spread of 145 bps between its acquisition and disposition cap rates.

The company’s latest transaction update for FY22 indicates that it surpassed the midpoint ($180M) of its revised acquisitions outlook range of $170M-$190M. Accordingly, Alpine posted a total acquisition volume of $187.4M for FY22, with a cap rate of 7.1%.

However, its dispositions came in below the midpoint of its guidance range, as Alpine posted a disposition volume of $154.6M, with an exit cap rate of 6.5%.

Alpine guided for FY22 AFFO per share of $1.75 (midpoint), with the consensus estimates suggesting $1.76. Hence, Street analysts are confident that the company could finish 2022 well.

However, the company could likely continue to face macroeconomic challenges relating to weaker consumer discretionary spending. As such, analysts have already penciled in a weaker FY23, with Alpine’s AFFO per share projected to fall by 8.6%.

As such, the bar has been set lower for Alpine to cross, which has likely been implied in its valuation, which is lower than its direct peers. Accordingly, PINE last traded at an NTM AFFO per share multiple of 12.2x.

However, it has already normalized from the dislocation that occurred at its October lows (pre-Q3 earnings), as the market volatility induced by the Fed’s hawkish cadence likely forced sellers to bail out in early October.

Therefore, the company’s robust Q3 earnings release likely calmed investors’ nerves, as PINE recovered nearly 27% (price-performance terms) toward its December highs.

As such, PINE’s NTM dividend yield of 6% has also normalized toward its 10Y average of 5.8%. Hence, the apparent undervaluation relative to its historical mean has already been seized astutely by dip buyers in October.

Management remains confident that its undervaluation against its peers is an advantage, seeing a “significant implied valuation upside.” However, we believe it’s appropriate to accord it lower valuation multiples to justify higher execution risks about its asset recycling strategy.

Notably, the company’s updated FY22 disposition volume was markedly below the midpoint of its guidance range ($160M). As such, we believe it indicates that the company has continued to see downside risks, given the current market conditions. Management also articulated in its Q3 earnings commentary indicating that “broader markets have less of that larger transaction stuff going on.”

Hence, we believe investors need to consider factoring in such headwinds, coupled with its external management structure. Despite that, the company highlighted its well-laddered debt maturity through 2026, and the relatively long average lease term remaining (7.6 years) helping provide earnings visibility for investors.

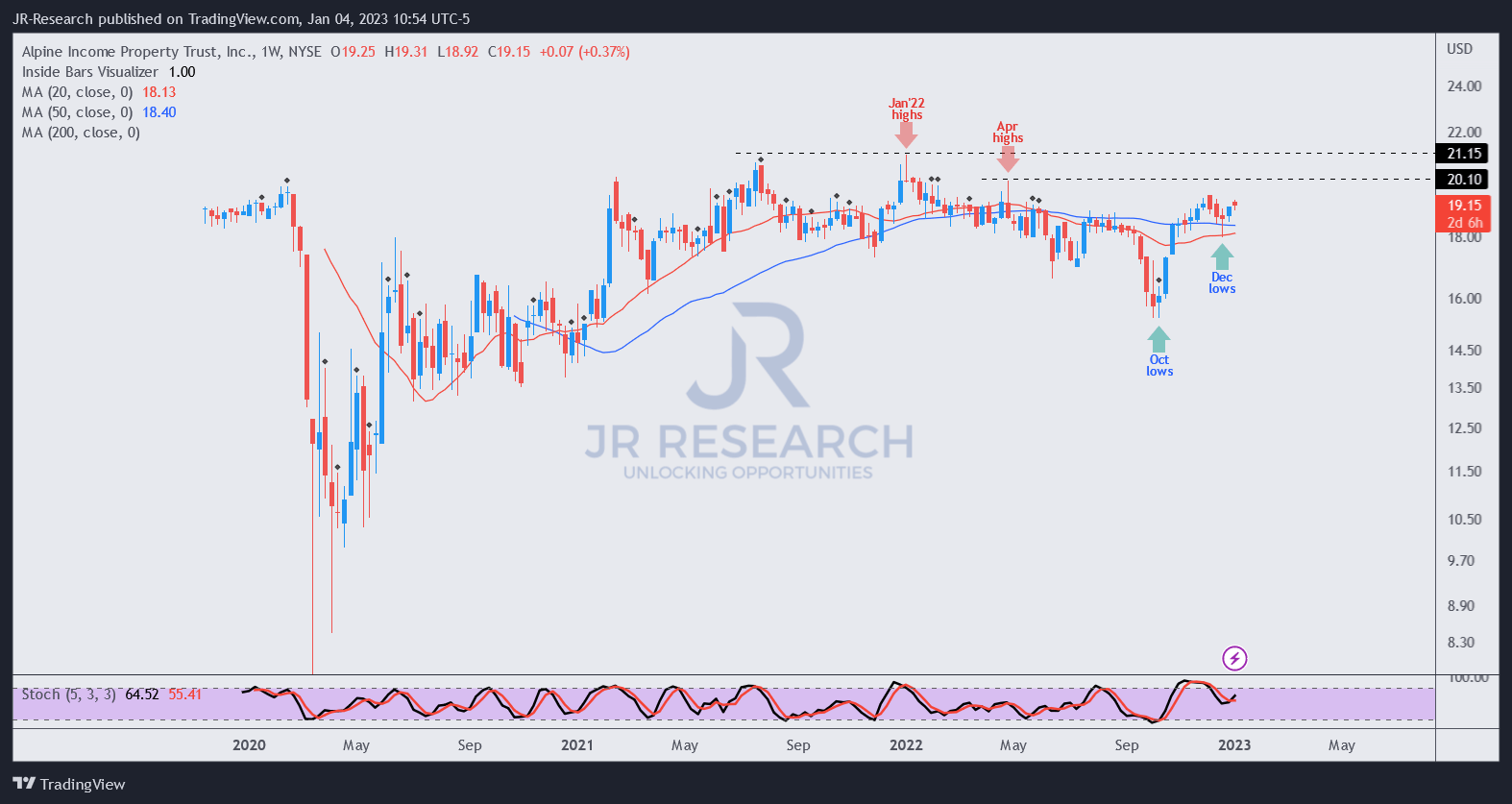

PINE price chart (weekly) (TradingView)

As seen above, PINE has recovered remarkably from its October lows, as buyers bought the panic selling forced by market operators.

Hence, we view the reward/risk from the price action perspective as well-balanced, with a view toward a likely pullback. Coupled with a normalized valuation, we encourage investors to wait for a better entry point.

Rating: Hold.

Be the first to comment