Natee Meepian

It may be argued that the past is a country from which we have all emigrated, that its loss is part of our common humanity.” ― Salman Rushdie

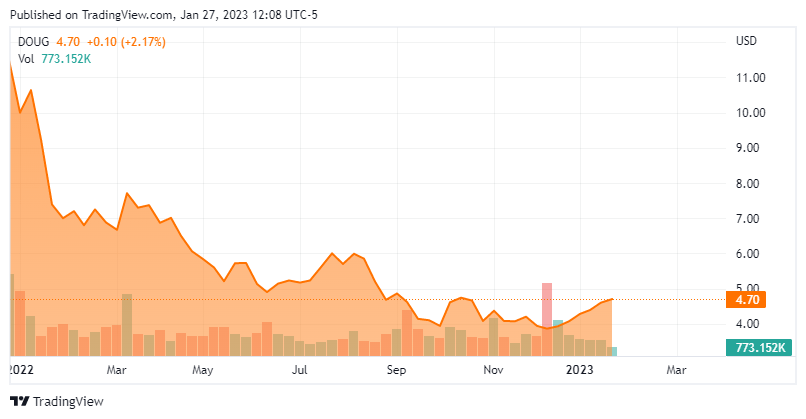

Today, we put Douglas Elliman Inc. (NYSE:DOUG) in the spotlight for the first time. This housing related concern came public just as the tides were turning in the housing sector as average 30 year mortgage rates doubled in 2022. However, the company has managed to stay profitable even with these headwinds and the stock pays north of a four percent dividend yield. The shares appear to be trying to put in a floor here (below). Better tidings on the horizon for 2023 for Elliman’s shareholders? An analysis follows below.

Seeking Alpha

Company Overview:

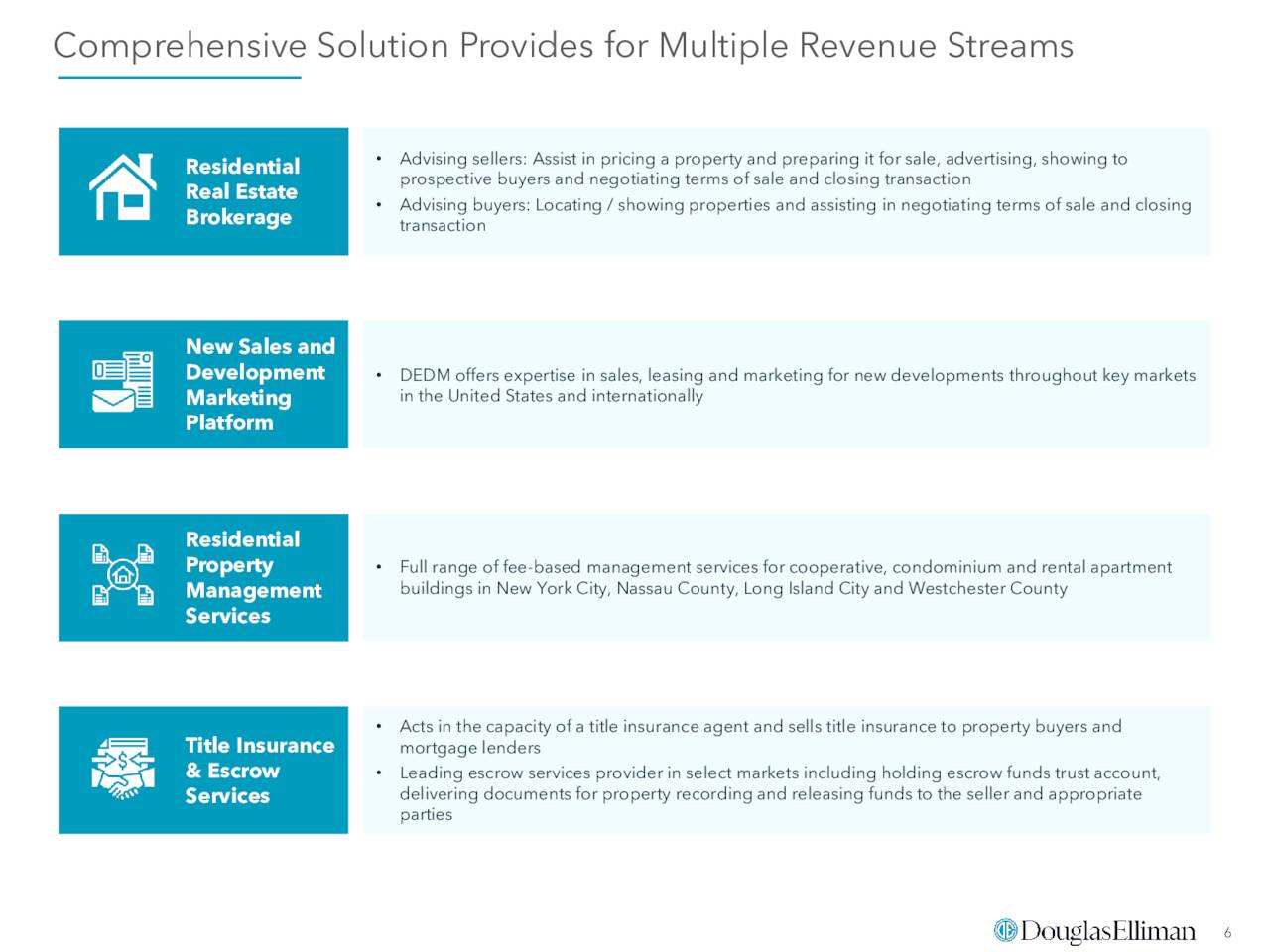

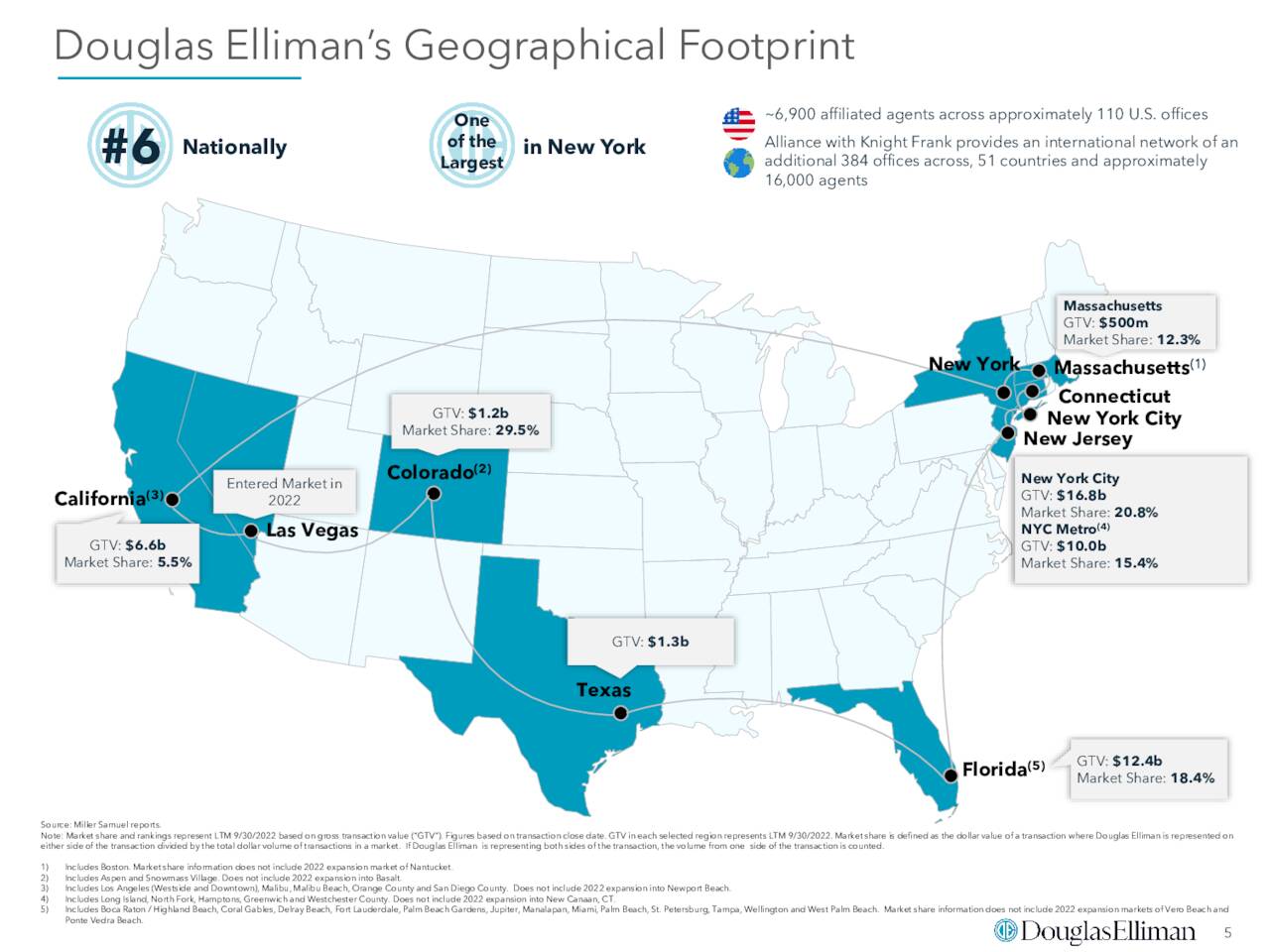

Douglas Elliman, Inc. is headquartered in Miami, FL about an hour north of me as the crow flies. It offers traditional real estate services via approximately 100 offices and 6,500 agents in New York, Florida, California, Connecticut, Massachusetts, Colorado, New Jersey, and Texas. Douglas Elliman focuses on the top end of the luxury market and is known for its outstanding service. The company has become the sixth largest real estate brokerage in the country. In addition, this brokerage firm manages over 350 buildings with just over 55,000 units in the New York City area.

November Company Presentation

The company also has a property technology investment business. Douglas Elliman gets over 90% of its overall sales from real estate commissions. The stock currently trades just above five bucks a share and sports an approximate market capitalization of $385 million.

November Company Presentation

Third Quarter Results:

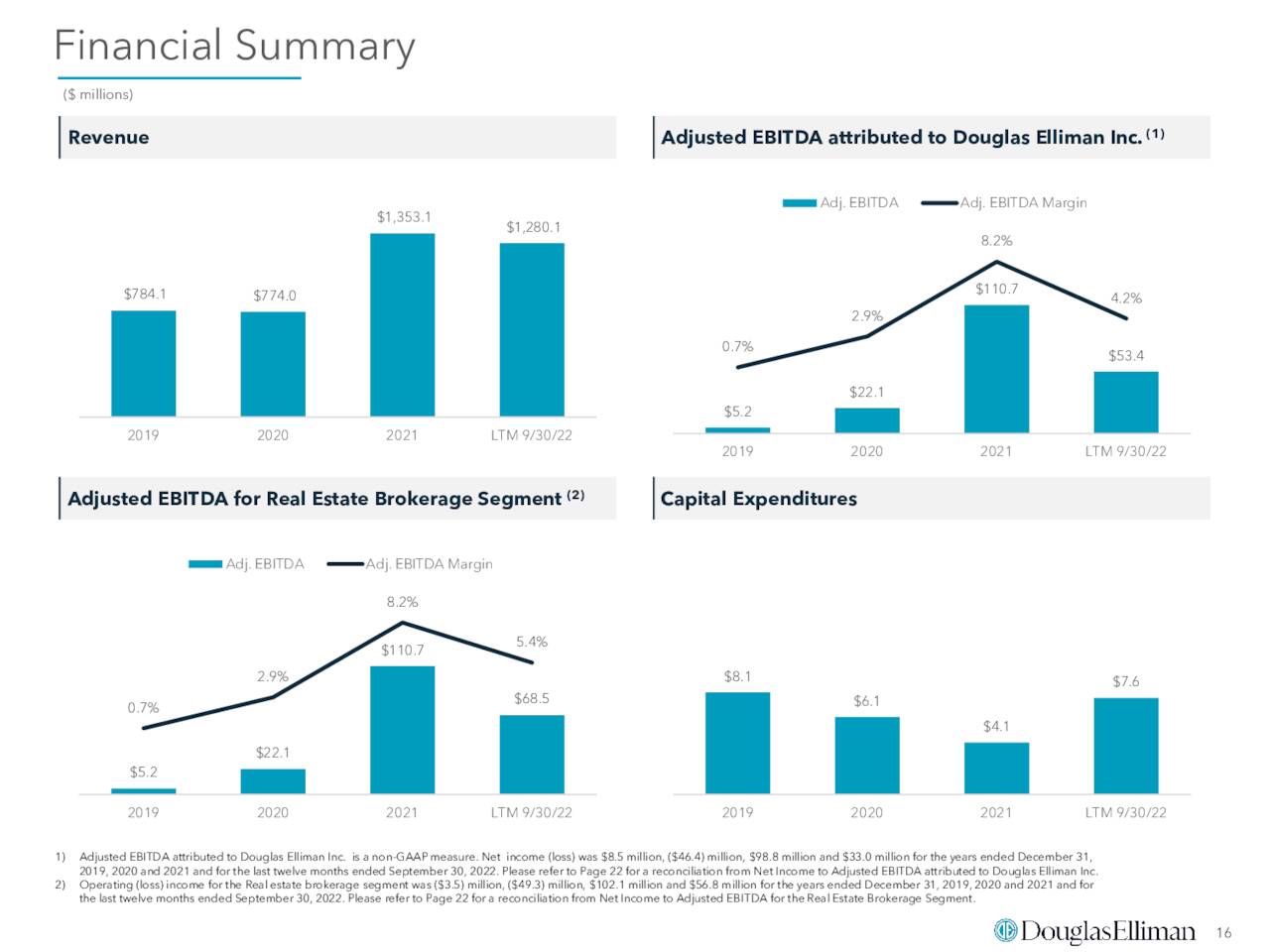

The company posted third quarter numbers on November 3rd. Douglas Elliman had a non-GAAP loss of a nickel a shares as revenues dropped 23% on a year-over-year basis to $272.6 million. Both top and bottom line results badly missed expectations.

November Company Presentation

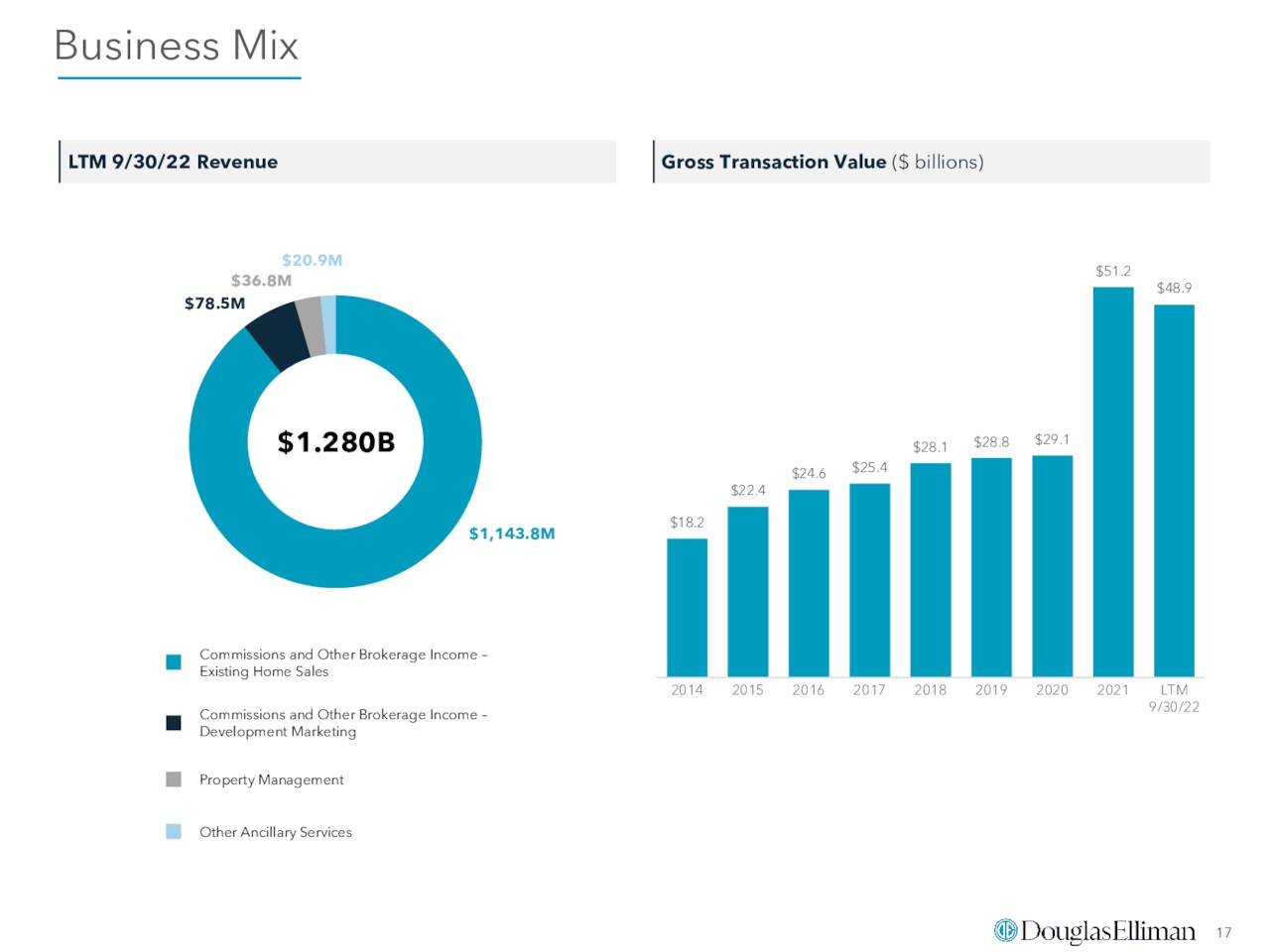

Gross transaction value came in at approximately $11 billion for the quarter down from $13.4 billion in the same period a year ago. The average transaction in the quarter was $1.53 million. Management attributed the decline in revenues and is net loss to ‘limited listing inventory and significantly increased mortgage interest rates‘ which is currently endemic across the industry at the moment. Adjust EBITDA shrunk to just $124,000 from over $27 million in 3Q2021.

November Company Presentation

Analyst Commentary & Balance Sheet:

I can find only one analyst firm chiming in on Douglas Elliman over the past year. On November 7th, Jefferies reissued its Buy rating and $6 price target on the shares.

November Company Presentation

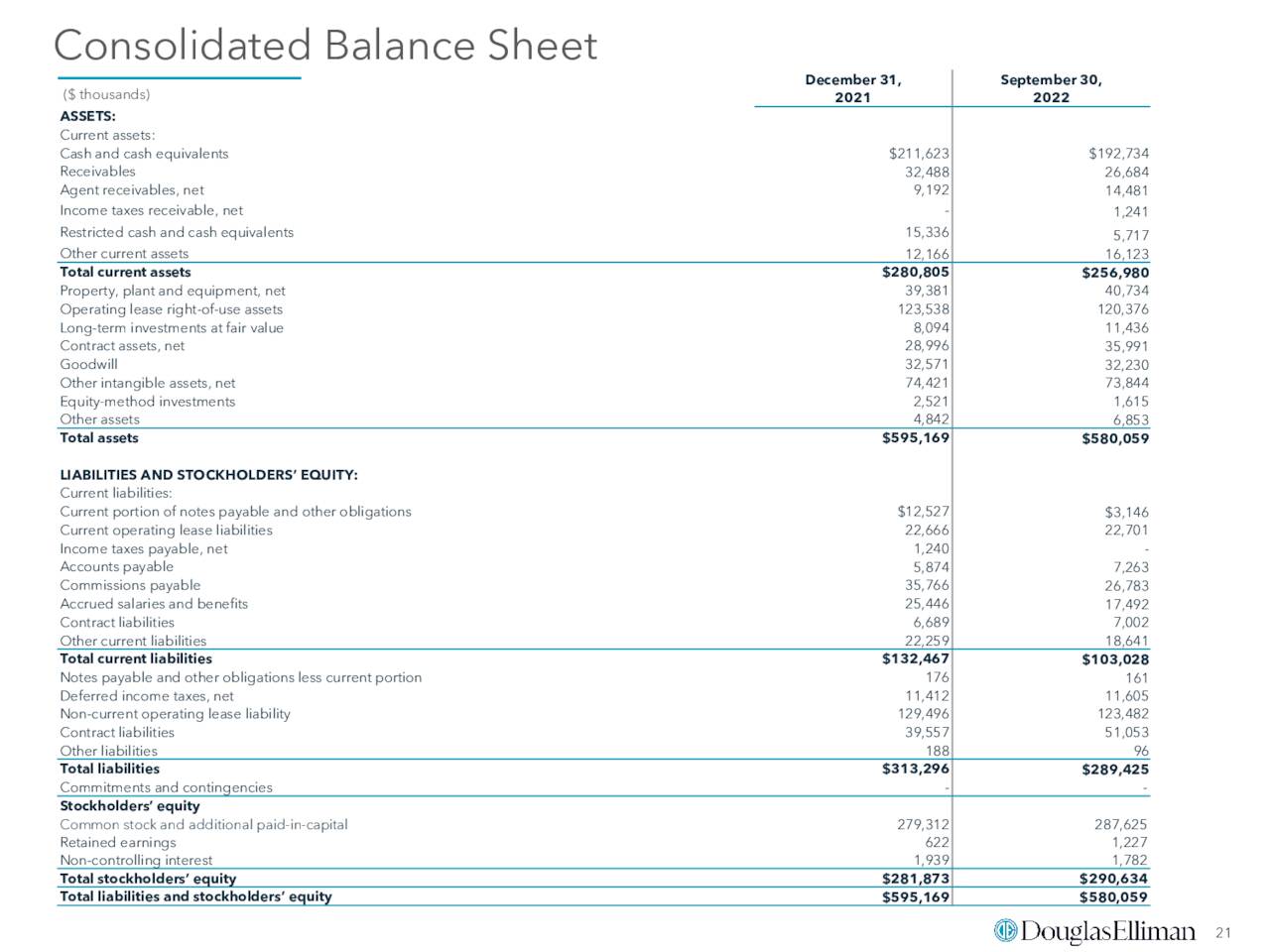

Several insiders bought just over $1 million worth of news shares collectively from March to September of last year. There has been no insider activity since then, however. Approximately two percent of the outstanding float is currently held short. The company ended the third quarter with just under $195 million of cash and marketable securities on its balance sheet against negligible long term debt.

November Company Presentation

Verdict:

The current analyst firm consensus has the company earning 12 cents a share even as revenues decline 10% in FY2022 to $1.2 billion. In FY2023 both sales and earnings are projected to drop ever so slightly.

November Company Presentation

The higher end of the real estate market has outperformed the lower and middle ends of the housing market to this point. That made not continue to be the case as we are seeing accelerating layoffs in high paying industries such as technology and Wall Street. Bonuses also have been cut dramatically in the latter, which should have at least a marginal impact on the New York City region were Douglas Elliman has an approximate 20% market share.

U.S. Census

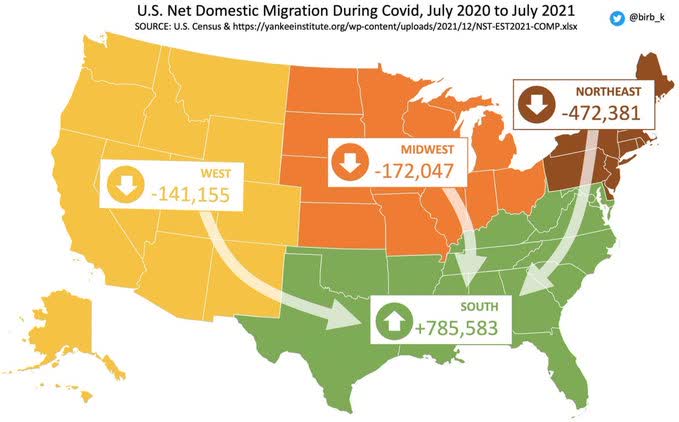

While the company has been prudent to expand outside of the Big Apple, especially doubling its footprint in red hot Florida in recent years, it is likely to remain impacted by the deteriorating economic health of Gotham as well as the continued exodus out of the region since the pandemic (Just under 65,000 New Yorkers got new Florida license plates in 2022).

The stock trades at 40 times earnings but at a much more reasonable valuation of one third of annual revenues. Both metrics are much cheaper if an investor equates for the net cash on the company’s balance sheet. The 4.3% dividend yield also is a positive for the investment thesis around DOUG. It is hard to see dividend payouts increasing until earnings growth returns but the dividend is more than safe given the company’s fortress balance sheet.

With earnings and sales projected to be flattish in FY2023, the stock could be dead money until the housing sector noticeably picks up, which might not be until 2024. The dividend payout does pay an investor to wait for a turnaround. That return can be enhanced by taking an initial stake in DOUG via a covered call strategy which also provides some downside risk mitigation as well. If I was an income investor looking for more exposure to this part of the market, that is how I would take an initial ‘watch item‘ holding in Douglas Elliman.

Do not swallow bait offered by the enemy. Do not interfere with an army that is returning home.“― Sun Tzu, The Art of War

Be the first to comment