Introduction

For the past two years, I have been warning investors about the dangers of overvalued, high-quality stocks and sharing a long-only rotational strategy to help mitigate the dangers of these highly-priced stocks. The basic idea is that when the expected 10-year forward returns of the target stocks (in this case Stryker (SYK)) get low enough, one rotates out of the stock and into a pair of ETFs with the goal that the ETFs will be more defensive during a downturn. Then, when the price of the target stock falls more than the defensive ETFs, the investor who likes the target company can rotate back in and own more shares than they would have had if they just held the stock the entire time.

In my October 17th, 2019 article, “Stryker: A 10-Year, Full-Cycle Analysis”, I made the case that Stryker was a Sell. At the time, my two standard alternative “default ETFs” were the Invesco S&P 500 Low Volatility ETF (SPLV) and Invesco Equal-Weight S&P 500 ETF (RSP). I tracked the results of my strategy (along with what would eventually become 42 other stocks I suggested selling due to high valuation this past year). The goal was to rotate half the funds back into Stryker once one could achieve a 20-25% “free share gain” and to rotate the other half of the funds back into Stryker once the stock was trading at fair value again. (For me, fair value, in this case, was an expected 10-year CAGR of 8%).

In this article, I’m going to examine whether it is time for investors who were bullish on Stryker’s long-term prospects who rotated out of Stryker back in October, to now rotate back in.

“Free Share Gain” Returns

Normally, this is a fairly simple process of checking the results of the default ETF versus the target stock, but we had a rare event take place at the end of February where it became clear we were headed for a recession. When that happens, we move all of our “default ETF money” into cash. I meticulously documented that in my last update article, “Going To Cash: Rotational Strategy Update (February 2020)”. The way I’m tracking the results now that the default money has been moved to cash is to calculate the returns on a theoretical $10,000 up to the point it was moved to cash, and then to compare that cash amount (which does not grow when it is held in cash) to the theoretical growth of $10,000 kept in the target stock.

In this case, when the money from SPLV and RSP was moved to cash, it would have been worth $9,580, so it would have lost money (about -5%) over the holding period. But the primary goal of this strategy was to increase our shares in Stryker for free, so let’s see what Stryker would have returned.

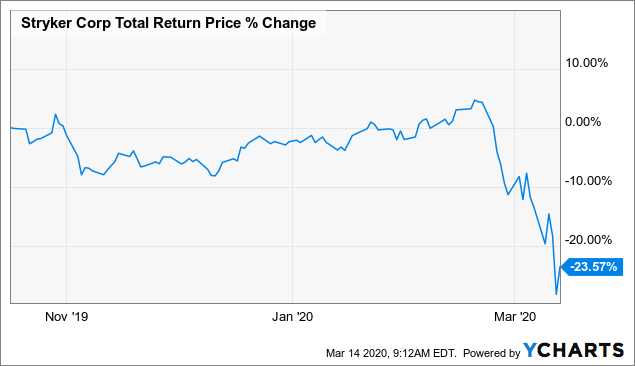

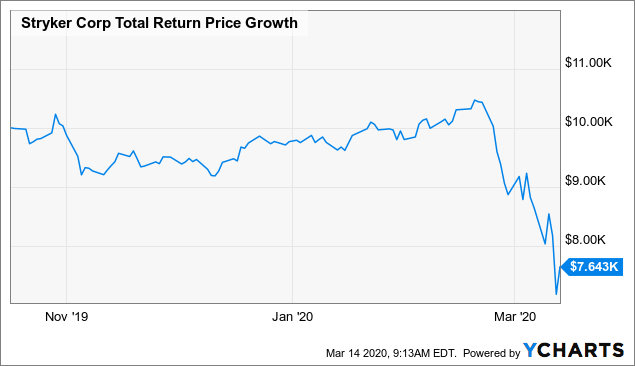

Stryker stock has fallen about -23% since my warning article and a $10,000 investment would now be worth $7,643. The money that was first put in SPLV and RSP, then into cash, would now be worth $9,580. An investor who followed this strategy could now take that $9,580 and buy +25.34% more Stryker stock than they owned back in October. In other words, an investor who owned 100 shares of Stryker stock on October 17th, 2019, could now buy 125 shares of the stock without spending any more money. This is on the high end of our 20-25% “free share gain” goal for the first part of the strategy, and so this part of the rotation is now complete.

Stryker now joins seven previous “free share gain” winners in the series so far.

What about the second half of the money?

We are using what I describe as a “simple mixed strategy” as a way to demonstrate my overall rotational approach. You can read about the strategy in these three articles: Part 1 “Ignore Sentiment Cycles At Your Own Risk,” Part 2 “Mitigating Sentiment Cycles” and Part 3 “Sentiment Cycles: When To Sell And When To Buy Back Again.”

The first part of the approach was to rotate back in after a 20-25% “free share gain” was possible. The second half of the money is to be rotated back in when the forward 10-year full-cycle CAGR estimate is near fair value at about 8%. So, next, I’m going to run what I call a “Full Cycle Analysis”, which is the same analysis I performed back in October that identified Stryker stock as being overvalued enough to sell. As part of the analysis, I calculate what I consider to be the two main drivers of future total returns: Market Sentiment returns and Business returns.

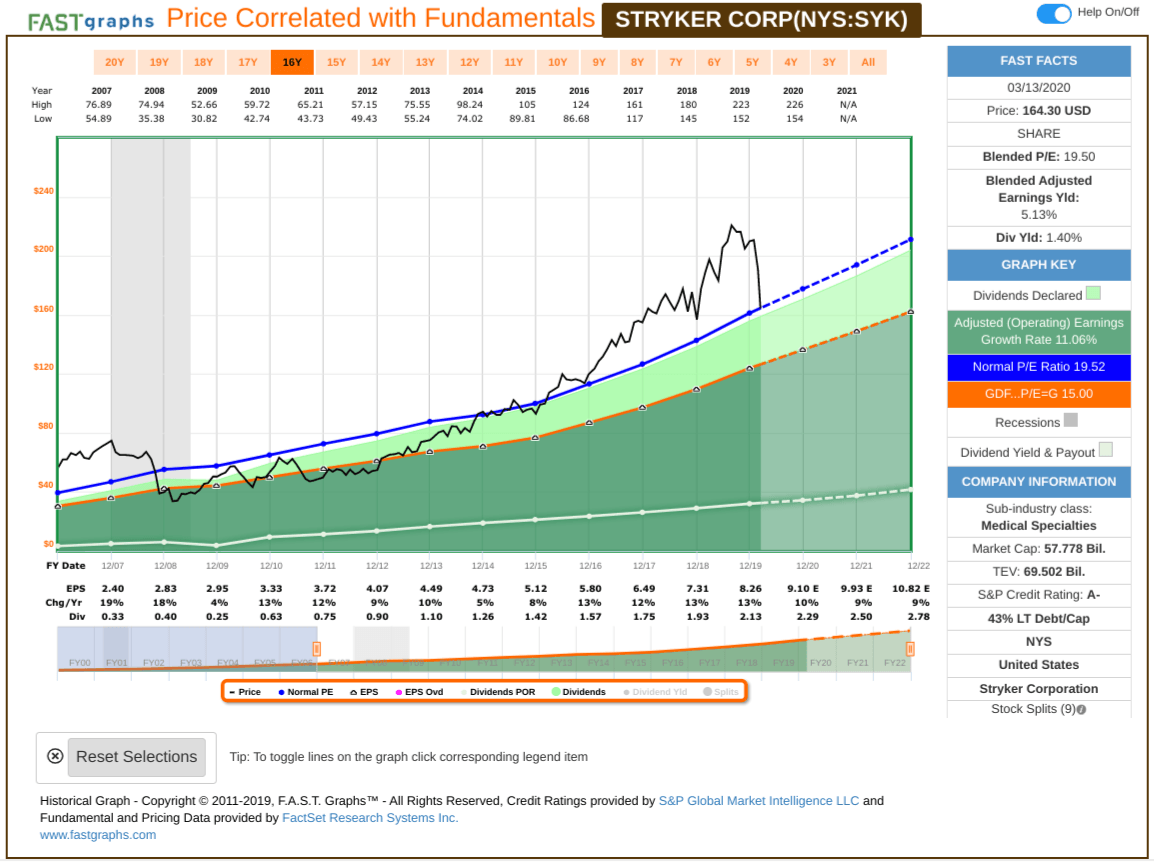

In order to estimate what sort of returns we might expect over the next 10 years, let’s begin by examining what return we could expect 10 years from now if the P/E multiple were to revert to its mean from the previous economic cycle. I start the previous cycle around 2007, about a year before the last recession.

As I write this, Stryker’s forward PE is 18.05 while its normal P/E this past cycle has been 19.52. With most stocks, unless there is a dramatic change in their business over time, the P/E will fluctuate up and down around their long-term mean, which F.A.S.T. Graphs labels “normal” P/E in blue. If, over the course of the next 10 years, Stryker’s P/E were to revert to its normal 19.52 level and everything else was held equal, it would produce a 10-year CAGR of about +0.78%. (At the time of my original analysis, this return was expected to be -3.28%.)

As I write this, Stryker’s forward PE is 18.05 while its normal P/E this past cycle has been 19.52. With most stocks, unless there is a dramatic change in their business over time, the P/E will fluctuate up and down around their long-term mean, which F.A.S.T. Graphs labels “normal” P/E in blue. If, over the course of the next 10 years, Stryker’s P/E were to revert to its normal 19.52 level and everything else was held equal, it would produce a 10-year CAGR of about +0.78%. (At the time of my original analysis, this return was expected to be -3.28%.)

Current and Historical Earnings Patterns

We previously examined what would happen if market sentiment reverted to the mean. This is entirely determined by the mood of the market and is quite often disconnected, or only loosely connected, to the performance of the actual business. In this section, we will examine the actual earnings of the business. The goal here is simple: We want to know how much money we would earn (expressed in the form of a CAGR %) over the course of 10 years if we bought the business at today’s prices and kept all of the earnings for ourselves.

There are two main components of this: the first is the earnings yield, and the second is the rate at which the earnings can be expected to grow. Let’s start with the earnings yield.

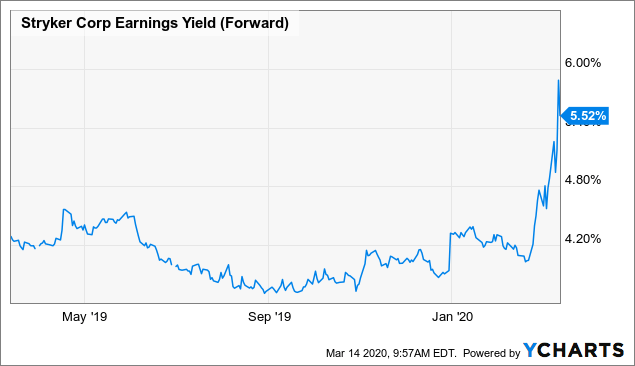

Stryker’s forward earnings yield is currently +5.52%. The way I like to think about this is, if I bought the company’s whole business for $100, I would earn $5.52 per year on my investment if earnings remained the same for the next 10 years.

Business earnings do not typically stay the same every year, however. Sometimes earnings grow, sometimes they shrink, and sometimes they fluctuate both up and down. So, in order to estimate how much money the business might earn over 10 years, one needs to estimate how the annual earnings might change over that time period.

Earnings Growth

Now we know what Stryker is currently earning. The next step is to estimate its earnings growth during this time period. I do that by figuring out at what rate earnings grew during the last cycle and applying that rate to the next 10 years. This involves calculating the EPS growth rate since 2007, taking into account each year’s EPS growth or decline, and then backing out any share buybacks that occurred over that time period (because reducing shares will increase the EPS due to fewer shares).

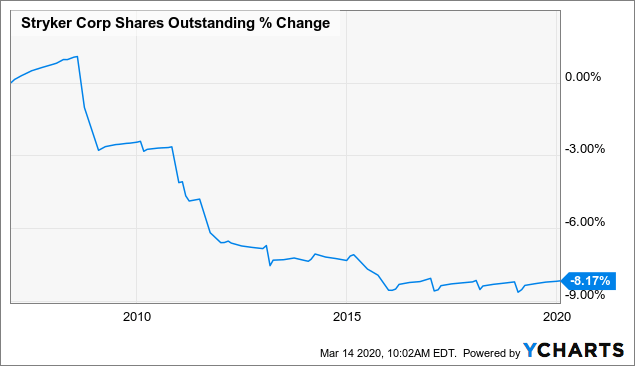

Let’s start by looking at how much shares were reduced since 2007.

Stryker has reduced its shares outstanding by about -8% over the course of this cycle. I’ll back these out for earnings growth estimates. When I go back to 2007 through today, I get a cyclically adjusted earnings growth rate for Starbucks of +10.50%, which is a very good growth rate.

Next, I’ll apply that growth rate to current earnings looking forward 10 years in order to get a final 10-year CAGR estimate. The way I think about this is, if I bought Stryker’s whole business for $100, it would pay me back $5.52 the first year, and that amount would grow at +10.50% per year for 10 years. I want to know how much money I would have in total at the end of 10 years on my $100 investment, which I calculate to be about $199.91. When I plug that growth into a CAGR calculator, that translates to a +7.17% 10-year CAGR estimate for the expected earnings returns.

10-Year, Full-Cycle CAGR Estimate

Potential future returns can come from two main places: market sentiment returns or earnings returns. If we assume that market sentiment reverts to the mean from the last cycle over the next 10 years, it will produce a +0.78% CAGR. If the earnings yield and growth are similar to the last cycle, the company should produce somewhere around a +7.17% 10-year CAGR. If we put the two together, we get an expected 10-year, full-cycle CAGR of +7.95%. Since this expected forward 10-year return is almost right at 8%, Stryker is now trading near “fair value”, and for the purposes of this demonstration of the rotational strategy, an investor could now rotate the second half of the money back into Stryker. Next, let’s see how the “fair value” portion of the rotational strategy performed.

“Fair Value” Returns

Sometimes, the “free share gain” portion of the rotation and the “fair value” portion of the rotation meet their goals at different times, and so the returns are different. In this case, the stock price has moved so much, they met their goals at the same time, thus producing identical gains for both parts of the rotation at +25.34%.

Stryker will now join five previous rotational “fair value” winners.

| Ticker | Free Share Gains from Full-Cycle Analysis |

| UNP | 19% |

| EXPE | 41% |

| CSX | 21% |

| NSC | 21% |

| SBUX | 35% |

| SYK | 25% |

And now, this completes the demonstration of the rotational strategy with Stryker. The first half of the rotation gained about 25% more free shares, and the second half also gained about 25% more free shares. I have 37 additional high-quality stocks I’m still tracking, though, so we should have a fairly large sample from which to judge and analyze the strategy in the future.

Additional notes

There are several goals of this series of articles. The first goal is to warn investors when I think certain stocks are overvalued enough to sell. The second goal is to provide a simple, long-only strategy that an average retail investor could use to address the problem of high-quality, overvalued stocks in their portfolio. And the third goal is to test these approaches in real-time to see what we can learn, thereby making the strategy even better.

Even though this part of the demonstration is complete and the goal of gaining 20-25% worth of free shares was a success, I am not actually buying Stryker stock yet because I prefer to have a margin of safety along with high expected future returns. So, personally, I will wait until Stryker has an expected 10-year CAGR over 12% before I consider buying the stock. Currently, I estimate that threshold would be crossed at about $125 per share. In the Cyclical Investor’s Club, I now have 200-300 stocks I track using this approach, and another 100 or so more cyclical stocks I track using a different method. The data for these now updates in real-time, which is quite handy in volatile times like we are currently experiencing.

If you have found my strategies interesting, useful, or profitable, consider supporting my continued research by joining the Cyclical Investor’s Club. It’s only $29/month, and it’s where I share my latest research and exclusive small-and-midcap ideas. Two-week trials are free.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Be the first to comment