Bastiaan Slabbers

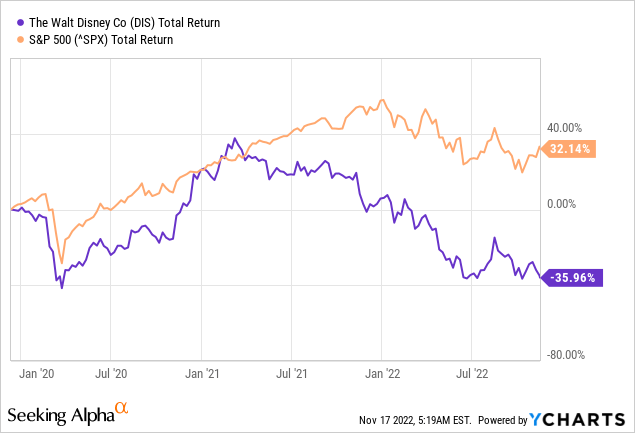

After losing more than a third of its value over the past 3 years, experiencing enormous volatility and suspending its dividend, Walt Disney Co. (NYSE:NYSE:DIS) has turned into a bitter disappointment for investors.

The reason why I use the past 3 years as a comparison is that back in December of 2019, at the time when hype around DIS was running near all-time high, I warned of the trilogy of problems that the company was facing.

At the time, it was extremely hard to envision a negative scenario going forward as Disney was capitalizing on its Direct-to-Consumer strategy and recent acquisitions. Unfortunately, however, it was at that time when Disney share price was not pricing in future risks and profitability has already peaked.

New Red Flags Emerging

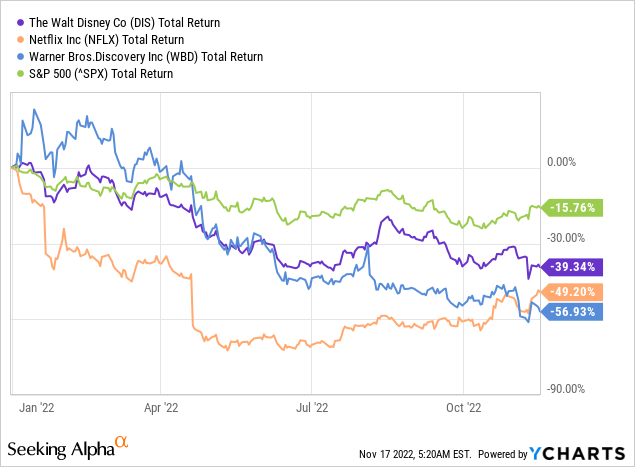

So far 2022 has been a rough year for equities overall, although growth stocks suffered far more when compared to value. The good news was that Disney fared slightly better than its peers – Netflix (NFLX) and Warner Bros Discovery (WBD) since the beginning of the year.

However, the 39% decline in DIS share price was more than twice that of the broader market. This results in a significant underperformance of Disney on a risk-adjusted basis, given the media company 5-year beta of 1.25.

On one hand this devastating performance of media companies during 2022 could be associated with their more cyclical business models and the lofty valuations at the beginning of the year. More importantly, however, has been the intensifying competition in the space which brought new entrants, consolidation and skyrocketing content costs.

While the cyclical downswing of the equity market could reverse in the coming years, the intense competitive pressures will not go away in the short to medium term. This makes future returns on capital highly uncertain for Disney, which went all-in its strategy of a massive increase in content spend across all of its brand portfolios.

Disney Investor Presentation

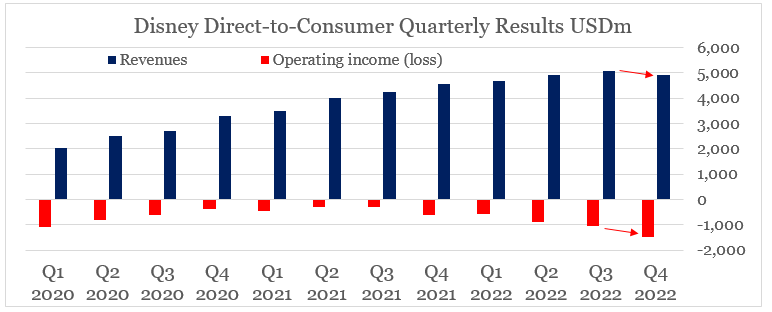

This now puts enormous pressure on the company’s DTC segment, which to the surprise of many noted a decrease in revenue over the last quarter, alongside record high losses.

prepared by the author, using data from SEC Filings

To reduce losses, management is now prompted to introduce price increases of its DTC offerings and a rollout of Disney+ ad tier.

First, our recently announced price increases across our Direct-to-Consumer offerings in the U.S. should begin to modestly benefit ARPU and subscription revenue in the first quarter. However, given that the Disney+ price increase will not go into effect until towards the end of Q1, this benefit will be realized more fully in the second quarter.

Source: Disney Q4 2022 Earnings Transcript

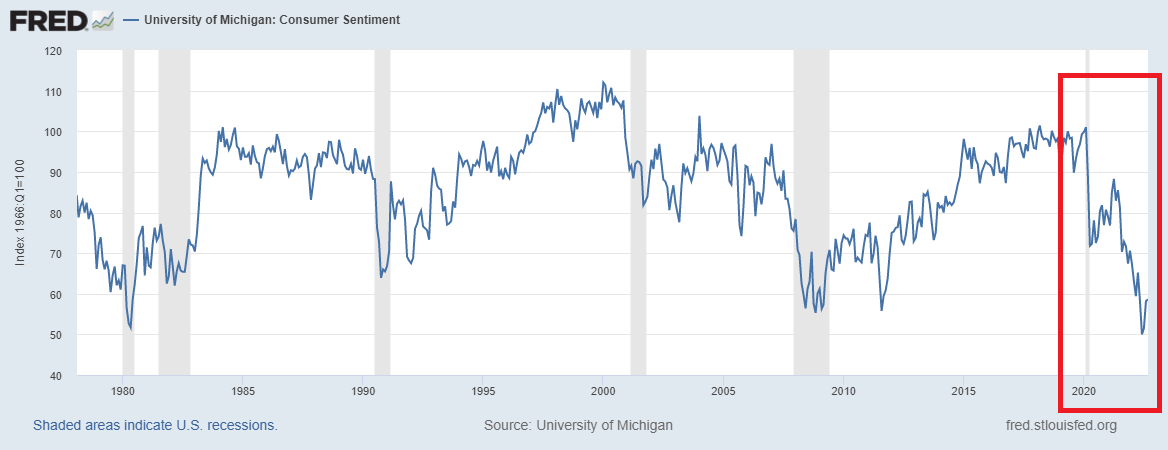

The overall impact of this strategy, however, remains highly uncertain in the very competitive streaming space at a time when consumer sentiment is near multi-decade lows.

FRED

The much awaited profitability of the DTC segment is still expected to occur at some point in 2024, but Disney’s management recently added an important caveat that this goal will largely depend on “health of the consumer” in 2023.

But we just think in abundance of caution, we really have to keep the health of the consumer in mind when we think about achieving all of our goals this upcoming year.

Source: Disney Q4 2022 Earnings Transcript

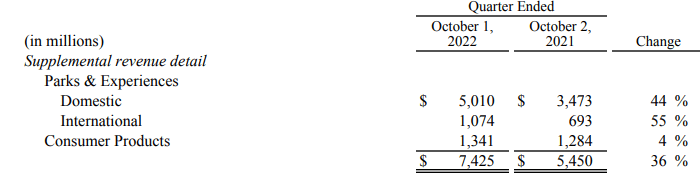

As if all that was not enough for Disney, but problems begun to emerge in its highly profitable Parks and Experiences segment. Expectations around the business unit have been running high in 2022 as pent-up demand from the pandemic lockdowns was expected to make up for its poor performance over fiscal years 2020 and 2021.

The total revenue of $7.4bn within the segment is already higher than the pre-pandemic levels of Q4 of fiscal year 2019.

Disney Earnings Release

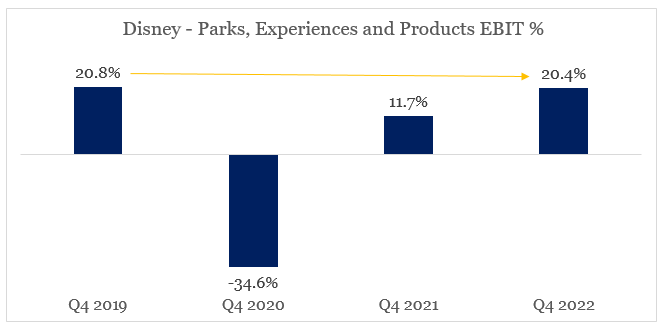

Topline recovery was high in both domestic and international markets, but profit margins did not exceed their pre-pandemic levels even at the much higher revenue base.

prepared by the author, using data from SEC Filings

All these developments now point to more uncertainty regarding Disney’s profitability as the company entered its fiscal year 2023.

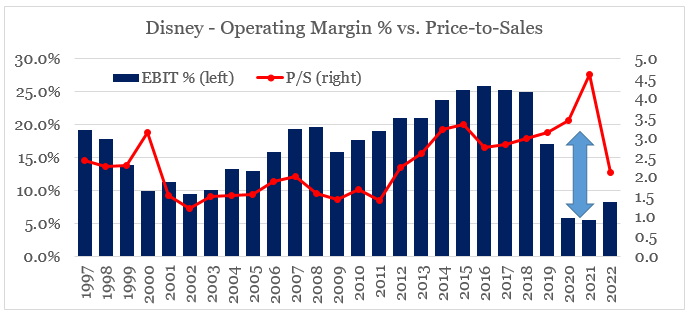

On a positive note, the massive decline in Disney’s share price has now brought the company’s price-to-sales multiple more in line with its operating profitability.

prepared by the author, using data from SEC Filings

It is by no means a definitive sign that Disney’s share price is now trading at fair value, but it is a major improvement since February of this year.

Conclusion

Disney share price will likely remain under pressure over the coming year, even though the share price lost more than a third of its value so far in 2022. The level of profitability that could be achieved by its DTC segment is still highly uncertain and there are early signs that shareholders might need to adjust their expectations of future margins. Deteriorating consumer sentiment makes the matters even worse as the recovery of the theme parks and resorts is now under scrutiny. Having said all that, however, the massive drop in DIS share price over the past year has taken some risk off the table and the bear case is now far less attractive than it was back in 2019.

Be the first to comment