Charley Gallay

If you had invested in Disney (NYSE:DIS) at the beginning of 2015 holding the position until today, you would have earned zero dollars. So a strong competitive advantage was not enough for this company to turn out to be a good investment.

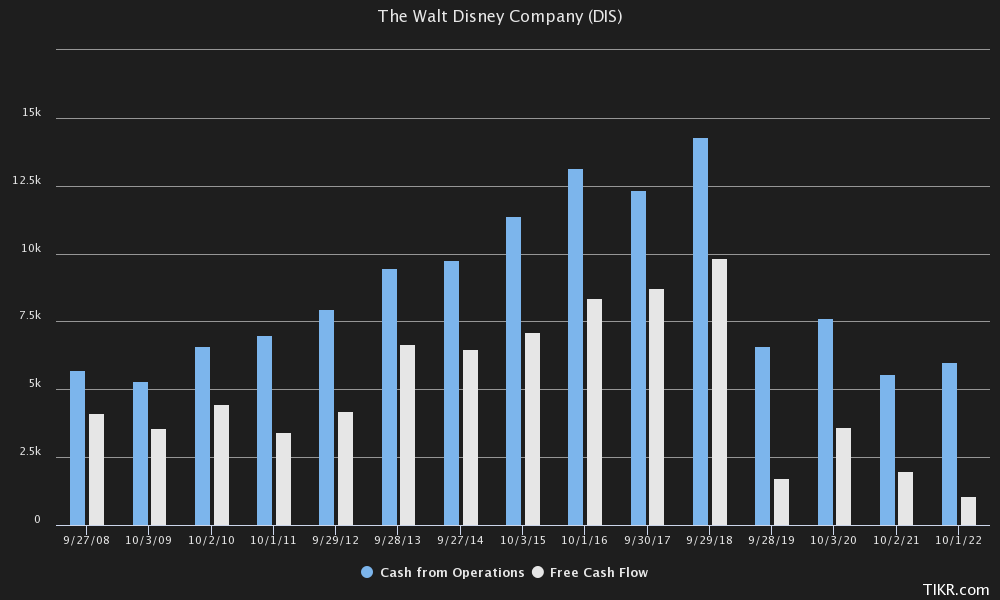

TIKR Terminal

The effects of Covid-19 have completely disrupted the continuity of this company, whose current free cash flow is nowhere near that of its golden years. With the parks closed for months such a meltdown was to be expected, however, today we are almost back to normal but Disney’s numbers are still underwhelming.

The decision to fire Bob Chapek for a return of Bob Iger was well received by the market, but I don’t think we should get too excited. Bob Iger left the company in one way, and today almost 3 years later, a lot has changed. There are several problems that need to be solved, and in this article I will lay out the two that I think are most urgent.

1st problem: Disney+ burns more and more money

Since the parks were closed during the pandemic, Bob Chapek during his tenure focused mainly on developing the Disney+ streaming platform.

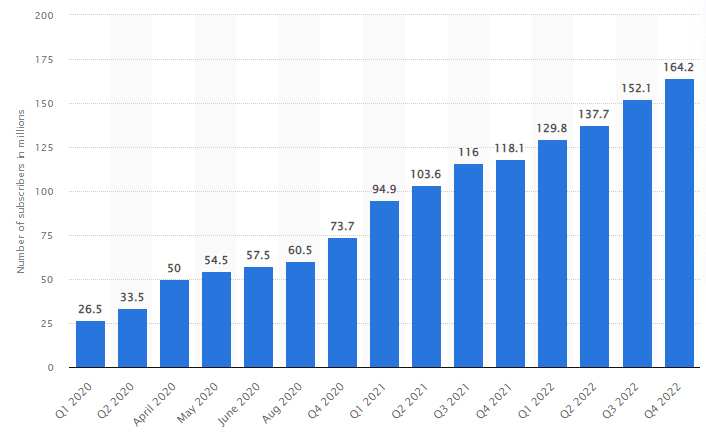

Statista

That platform in a short time has gained a great response from the public, and in just under 3 years has reached 164.2 million subscriptions. Currently, it is the third largest streaming platform by subscriptions, behind Amazon Prime (200 million) and Netflix (223.09 million). Certainly a great result, but there is one problem, however: Disney+ is unprofitable and the company does not seem too concerned.

Our fourth quarter saw strong subscription growth with the addition of 14.6 million total subscriptions, including 12.1 million Disney+ subscribers. The rapid growth of Disney+ in just three years since launch is a direct result of our strategic decision to invest heavily in creating incredible content and rolling out the service internationally, and we expect our DTC operating losses to narrow going forward and that Disney+ will still achieve profitability in fiscal 2024, assuming we do not see a meaningful shift in the economic climate.

Former CEO Bob Chapek with this commentary on Q4 2022 highlighted the growth in subscriptions and also exposed his confidence that Disney+ can become profitable in FY2024.

Regarding subscription growth, nothing to say. They are increasing very fast and I would not be surprised if Disney+ hits 200-220 million subscriptions in the next 2 years. On the other hand, I would be definitely surprised if Disney+ becomes profitable by FY2024, and now I will explain why.

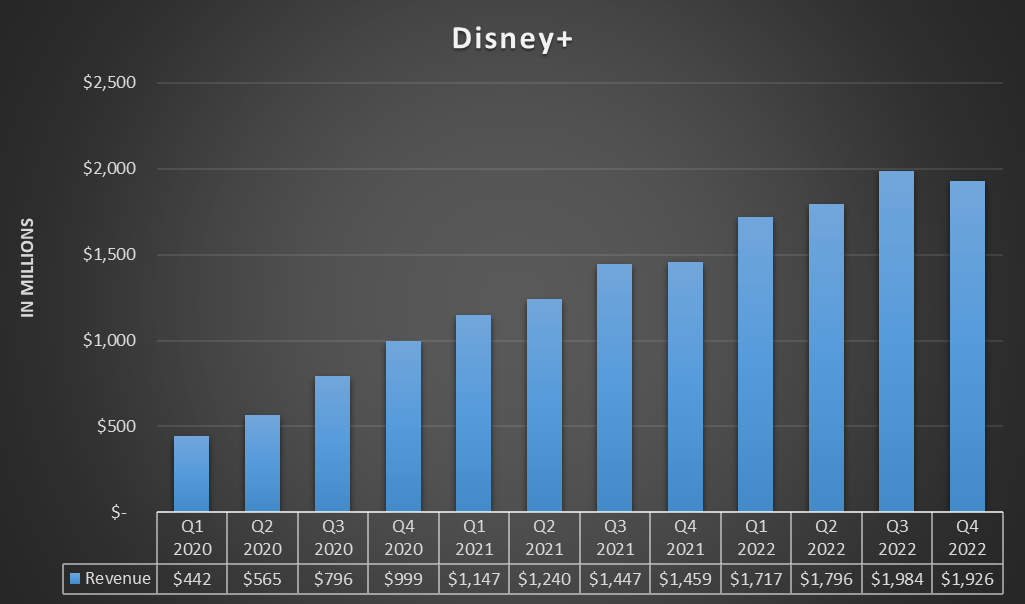

Company data

This chart shows Disney+ quarterly revenues from Q1 2020. The first thing that jumps out is that for the first quarter, revenues declined and therefore we are seeing a slowdown in growth. This result, in contrast to that of new subscriptions, is mainly due to the year-over-year deterioration in average monthly revenue per paid subscribers.

Statista

Overall, in FY2020-FY2021-FY2022 Disney+ revenues were $2.80 billion, $5.20 billion and $7.40 billion respectively.

So, objectively, revenues have grown a lot in 3 years although they are facing a stagnant period in the last quarter. The problem is that despite such marked growth, Disney+ continues to burn money because of operating costs that are growing more than revenues themselves. The result is that Disney’s revenues increase but operating income decreases.

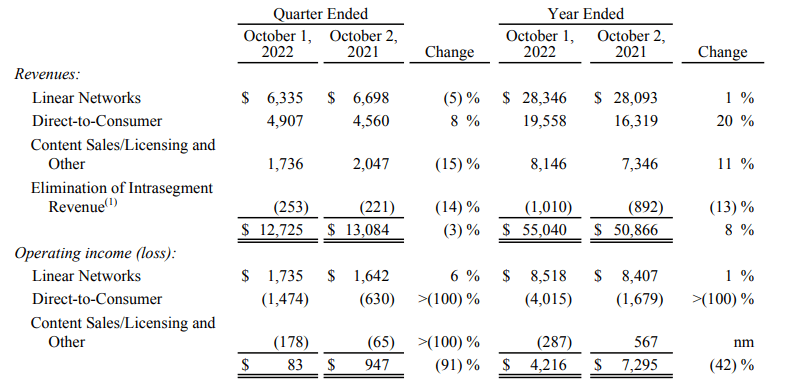

Disney FY 2022

In fact, as can be seen from this image, the direct-to-consumer segment, (which is the one that includes Disney+, Hulu, and ESPN+) experienced a larger operating loss in FY2022 than in FY2021 despite revenues increasing by 20%. In my view, it is worrisome how a segment that continues to grow rapidly posted an operating loss of $4 billion despite the fact that revenues generated were $19.55 billion. The impression is that the more Disney+ grows, the more Disney loses money.

So, in light of these considerations, I do not see how Disney+ can be profitable by FY2024 by continuing in this way. What is needed is a change in the business model that can either reduce operating costs or increase revenues. All of this, however, without reducing subscriptions.

Personally, I believe that Disney+ is unlikely to become profitable by FY2024 given the current situation, but I would not rule it out entirely; in fact, there will be important news soon.

CFO Christine McCarthy has stated a willingness to “rationalize the cost base” now that the launch of Disney+ has been completed globally. So, I expect that as early as next quarter the company will spend less on licensing new content within Disney+, as well as spend less on advertising the platform.

Moreover, the changes are not only in operating costs, but also in revenues.

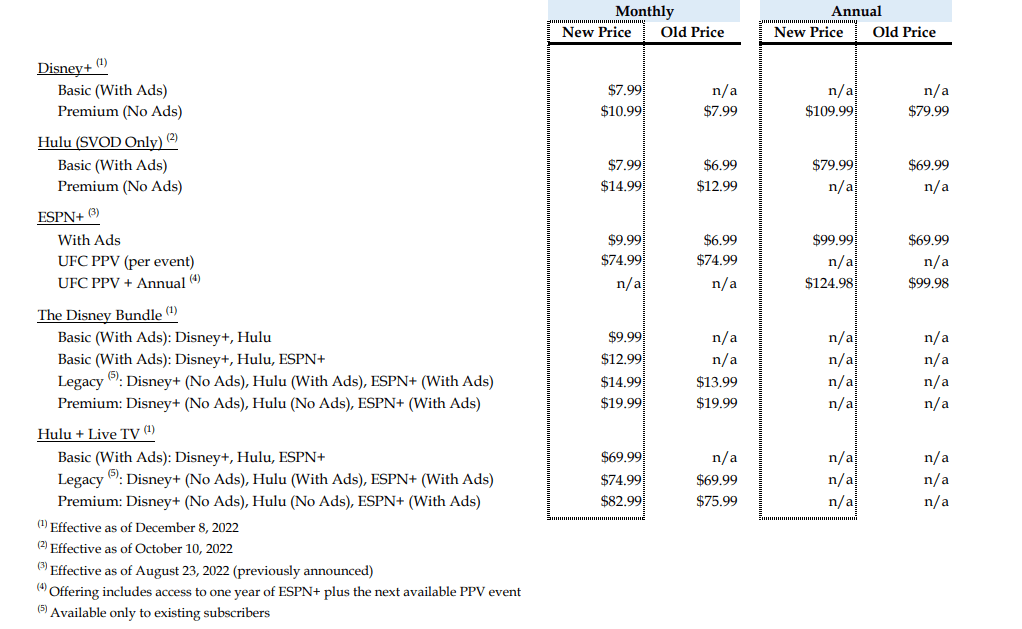

thewaltdisneycompany.com

This is the new price list related to direct-to-consumer platforms, where the biggest change is not the price increase, but the possibility of an ad-free or ad-supported Disney+ subscription. The new subscriptions will be available from December 8.

So, the news about the Disney+ business model is there, which is good because the previous situation was not sustainable, but we do not yet know how consumers will react to this. There could be a sharp increase in revenues due to the new low-cost subscription that includes advertising, just as there could be a decrease due to people’s reluctance to pay for a subscription that does not exclude advertising. At the same time, the reduction in operating costs as a result of the decrease in content within the platform could be an additional incentive for subscribers to flee. It is very complex to understand how the situation will evolve after these changes, but I think that as early as the next quarterly report we may know more. For sure, it will not be easy for Bob Iger to find a way to make Disney+ profitable by FY2024.

2nd problem: Disney parks are too expensive

Disney FY 2022

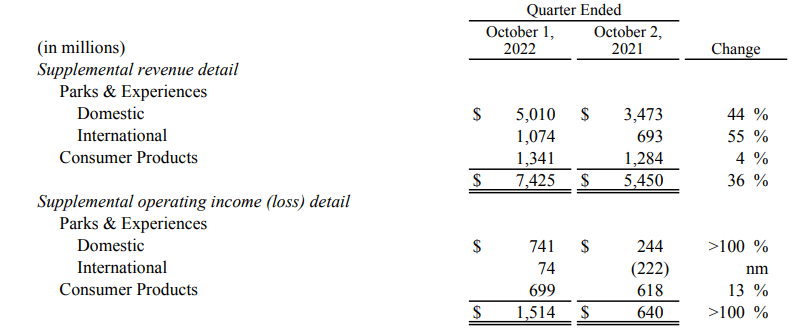

Looking at the results achieved in Q4 2022 we can see that there was a clear improvement over Q4 2021. The reduction of restrictions related to Covid-19 meant that Disney could make the most of what it has to offer within its parks. The sharply rising revenues were not only due to this aspect, however, but also to an increase in park prices. Ticket prices have increased and with it all the costs associated with the experience itself.

If we were based on the Q4 2022 results, the price increase was a good move as the demand was such that it supported them, however, I have concerns about whether this is sustainable for the next few years.

This 2022 was a record year in terms of vacations, and the reason for this is mainly because in the previous 2 years Covid-19 limited people’s ability to be able to travel. Many trips that should have taken place in 2020 or 2021 were postponed to 2022, the first year where Covid-19 was not so limiting. This situation obviously also applies to the Disney parks, where people were also willing to spend more after two years of waiting. The year 2022 was basically one of the best years where the Disney parks were very crowded.

From a revenue standpoint, 2022 was a success for the parks, but we often tend to overlook something that is perhaps even more important. In fact, it would seem that the parks’ high prices have disappointed fans’ expectations. Here are the results of a survey issued by time2play based on 1,927 Disney World fans:

- 92.6% believe that the cost of a vacation to Walt Disney World Resort is out of reach for the average American family.

- 68.30% believe Disney World has lost its magic due to excessive costs.

- 66.90% believe that they will not get the full Disney World experience unless they upgrade to Genie+ and purchase additional admissions to Lightning Lane.

Overall, these results indicate a tendentially negative experience in Disney parks for those who are not willing to spend an exorbitant amount of money. This may be a sign that fans will think twice before taking another vacation to a Disney park. In my last article on Disney I detailed what changes are hurting the overall experience, if you want to learn more about this I encourage you to read it.

In addition to rising prices, the current macroeconomic situation should also be considered since we are probably on the verge of a recession. In order to combat inflation, the major central banks around the world have raised interest rates a lot, which has restricted access to credit and slowed down the economy. During recessions, of course vacations are not the priority, and expensive parks like Disney’s could become a luxury. Here is what happened in the last major recession.

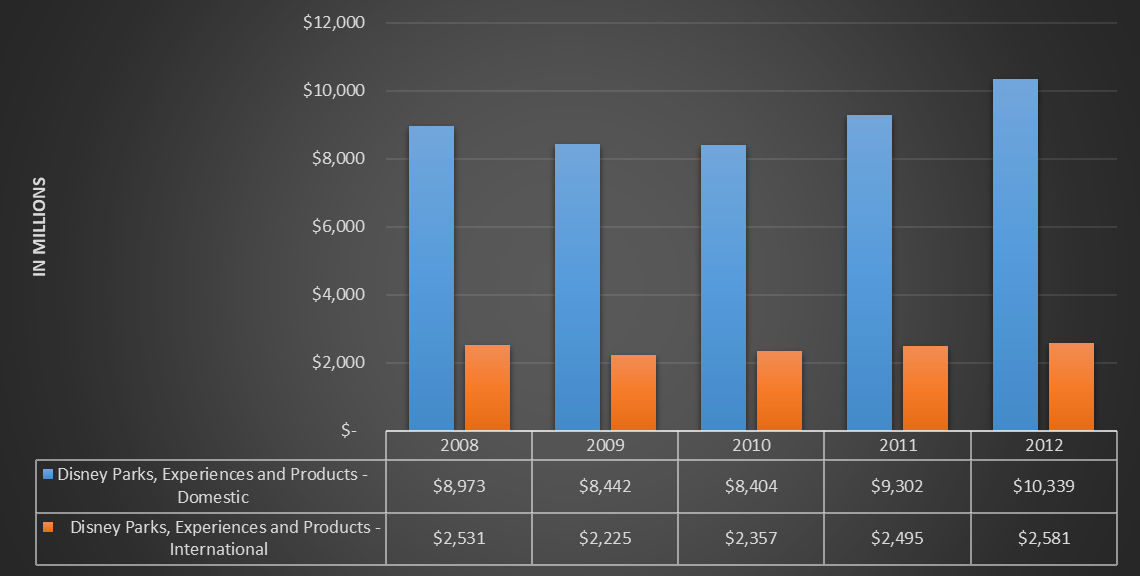

TIKR Terminal

As for the domestic segment, parks experienced a decrease in revenues in 2009 and 2010, recovering only in 2011. The international segment had more difficulties, and only in 2012 reached the peak of 2008. My guess is that in the next 2-3 years a similar situation may arise again, but it depends a lot on how severe the recession will be and how Disney will react. If significant discounts were to be introduced there would probably still be good park attendance, but it is by no means a given.

After a good 2022 in terms of park revenues, it will not be easy for Bob Iger to improve on this result at the doorstep of a recession and with fans unhappy with their last Disney parks experience.

Although the outlook is not rosy, I am changing my rating for Disney from sell to hold. The reason for this is due to the recent change of CEO which gives me hope for how Disney will be managed in the future since I personally did not like the choices made during Bob Chapek’s tenure. Bob Iger has already managed this company excellently for 15 years, and I believe he will be able to make Disney+ profitable (although I doubt by FY 2024) and find the right compromises to bring back enthusiasm among disappointed fans. As of today, 52% far from an all-time high and with Bob Iger’s return, one might even consider making an initial entry. Personally, I will think about it around $80-85 per share.

Be the first to comment