gsheldon

What’s For Dinner?

Tyson Foods, Inc. (NYSE:TSN) released its FY2023 Q1 results yesterday, and investors were, let’s say, disappointed with the amount of chicken on the bone. Top line revenue for the protein giant grew 2% year-over-year to $13.2 billion. While this wasn’t stellar, it was all the lines below revenue that drew investor ire. In this article we’ll dive into the earnings, what we think it means for Tyson in the quarters ahead, and how we’re currently approaching an investment in Tyson’s troubled stock.

The Numbers

Tyson reported gross income of $941 (a staggering 52% decline in gross margin year-over-year) and operating income of only $453 million. That works out to an operating margin of around 3.4%.

We should point out that Tyson’s business is incredibly competitive, and that margins are historically quite thin. This level of margin collapse, however, was not what investors were expecting, and the stock plunged more than 8% on the news.

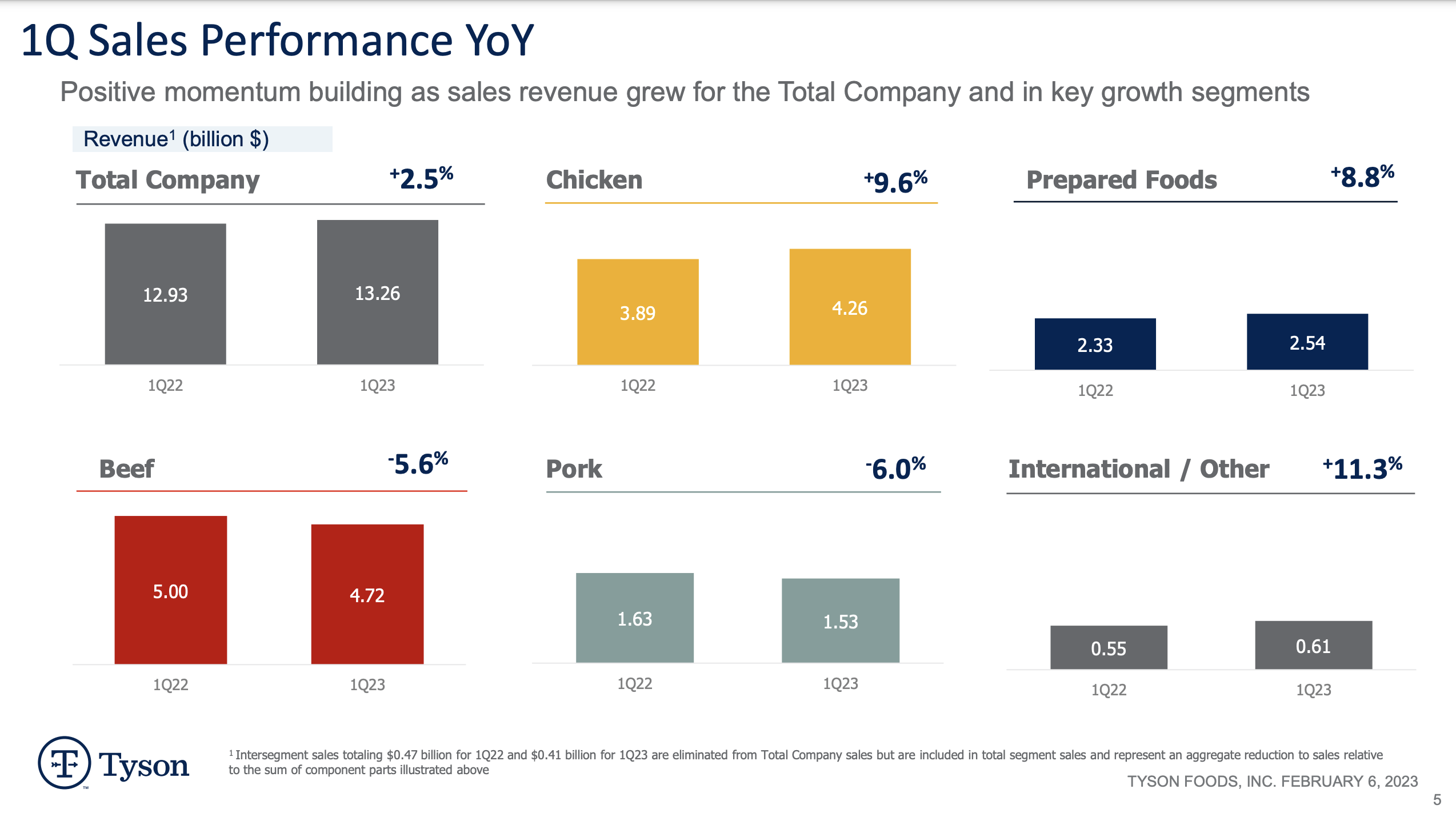

Tyson Sales (Company Presentation)

Tyson experienced stronger than expected headwinds in its beef and pork divisions. Both higher prices and lower demand hit the company in ways that executives did not expect (though this was particularly surprising in pork, CEO Donnie King noted in the Q1 conference call that the company had been expecting a slowdown in beef for some time, but not to the degree experienced).

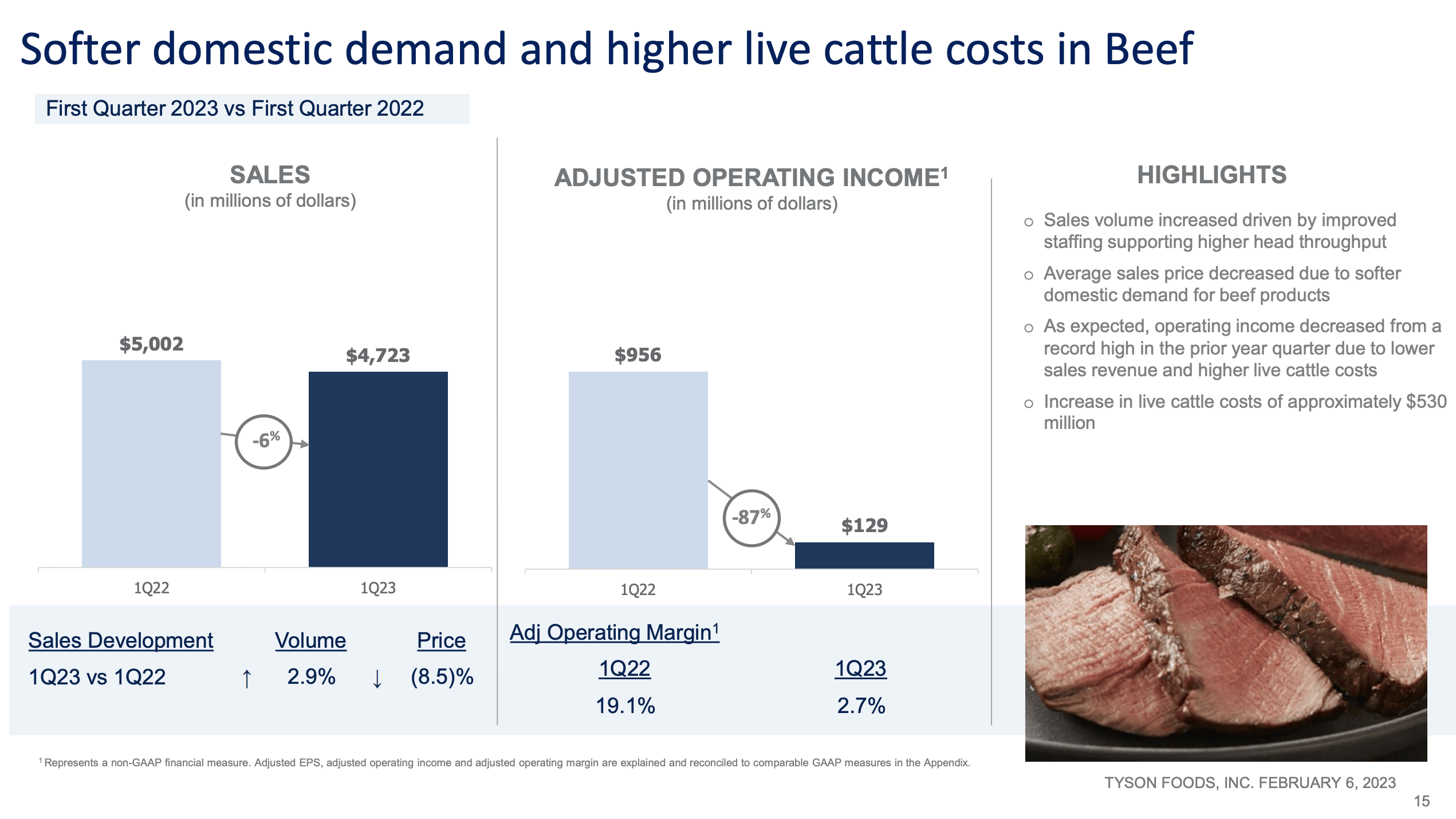

Tyson’s Beef Sales (Company Presentation)

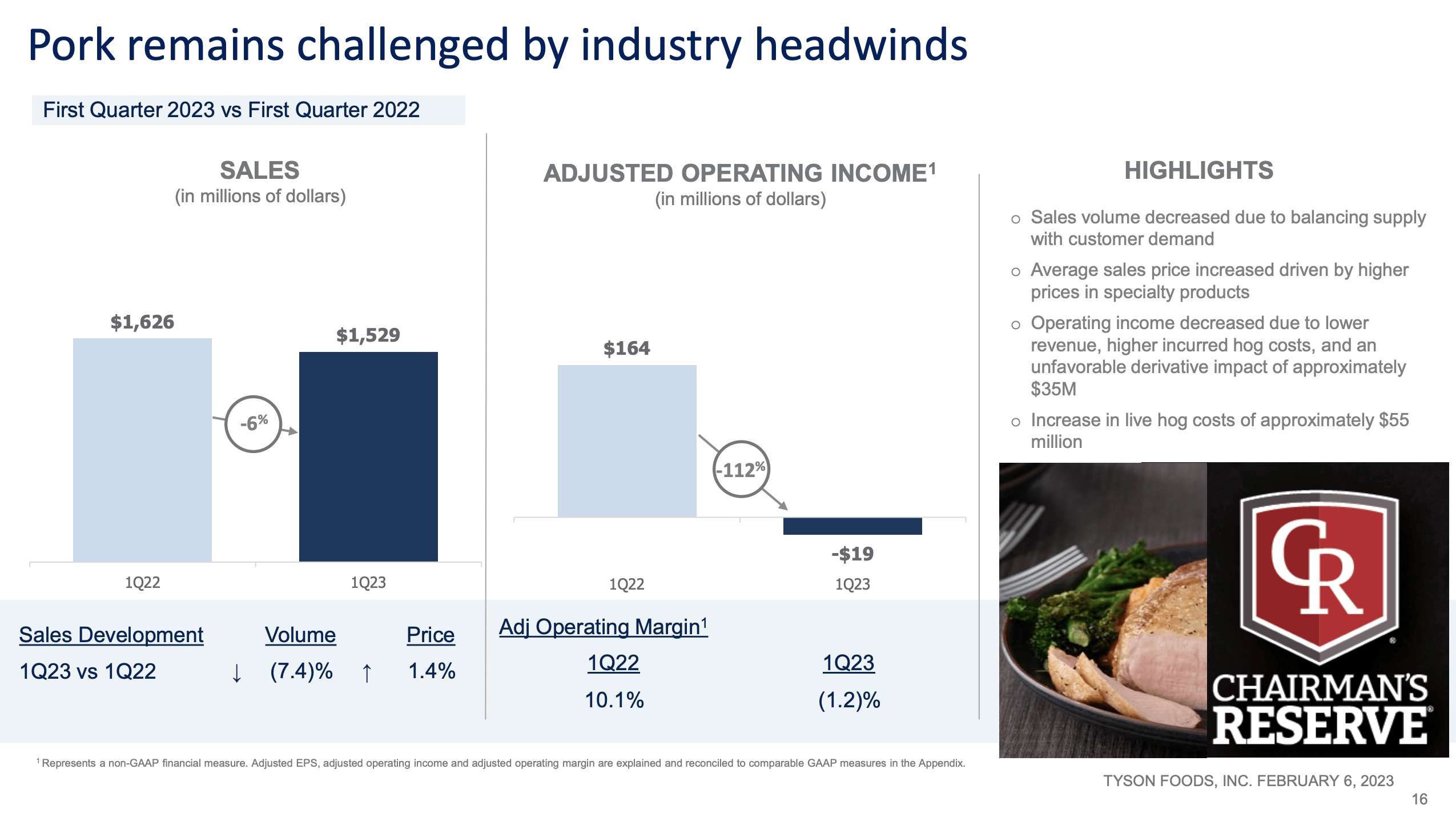

The results from Tyson’s pork division, however, were likely the toughest for investors to stomach.

Tyson Pork (Company Presentation)

Margins collapsed so far in pork that they went negative, falling 112% year over year to negative 1.2%. Most curious in the results is that while hog prices indeed rose, Tyson incurred a negative derivative impact of $35 million. It’s not unusual for a company like Tyson to hedge its exposure to lean hogs, beef, and feed by utilizing various hedges, but it was a surprise to see that the hedges worked against the company in this instance.

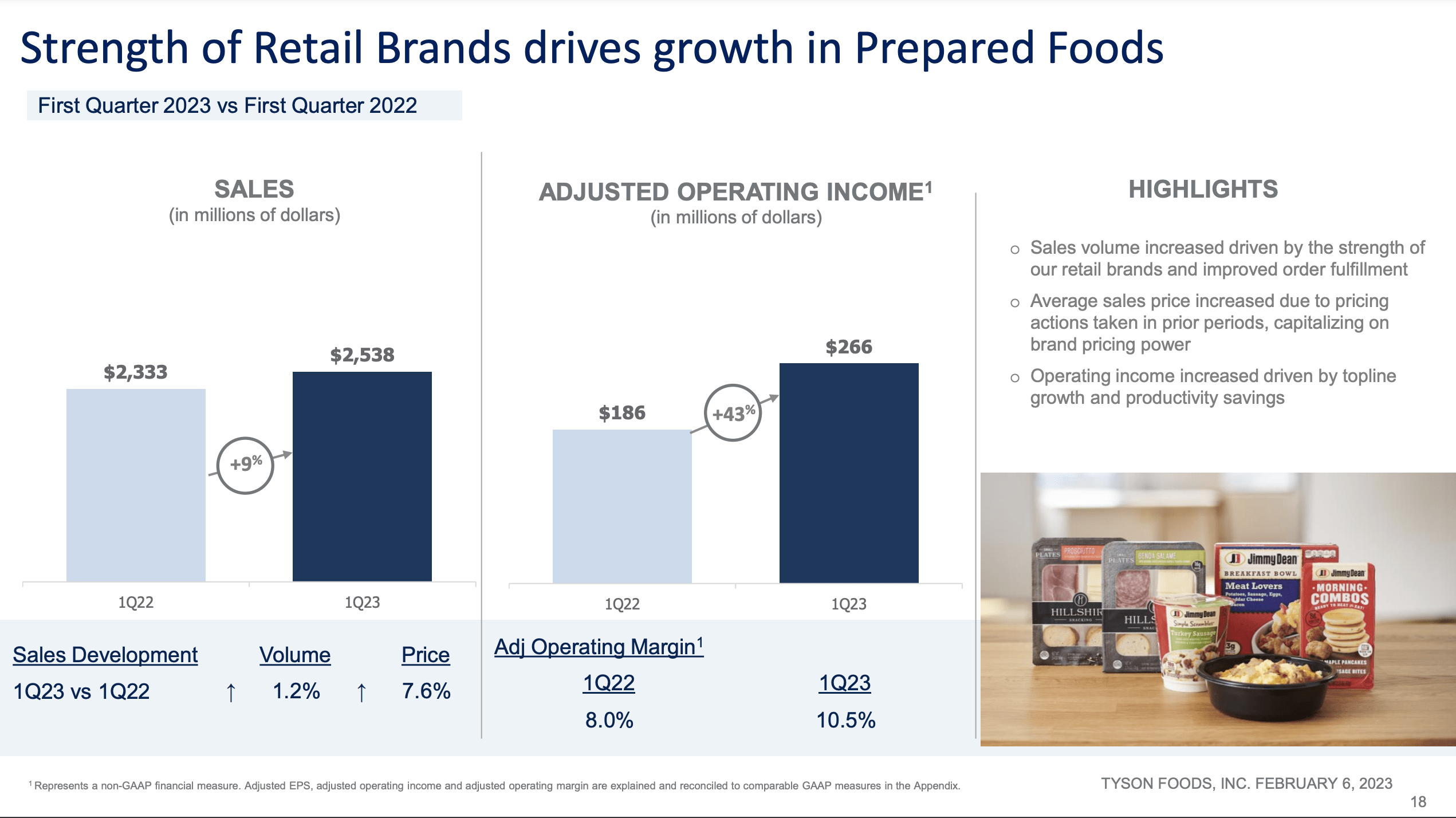

Tyson’s Processed Foods (Company Presentation)

A bright spot in the earnings was the company’s processed food, with sales up 9% and adjusted operating income up 43%. Tyson has performed well in this market, and it owns multiple household-name brands in the space, such as Hillshire Farms, Jimmy Dean, and Ball Park hotdogs. These retail categories are performing well, and management was upbeat on the conference call, noting that shelf-fill levels and replenishment rates are improving.

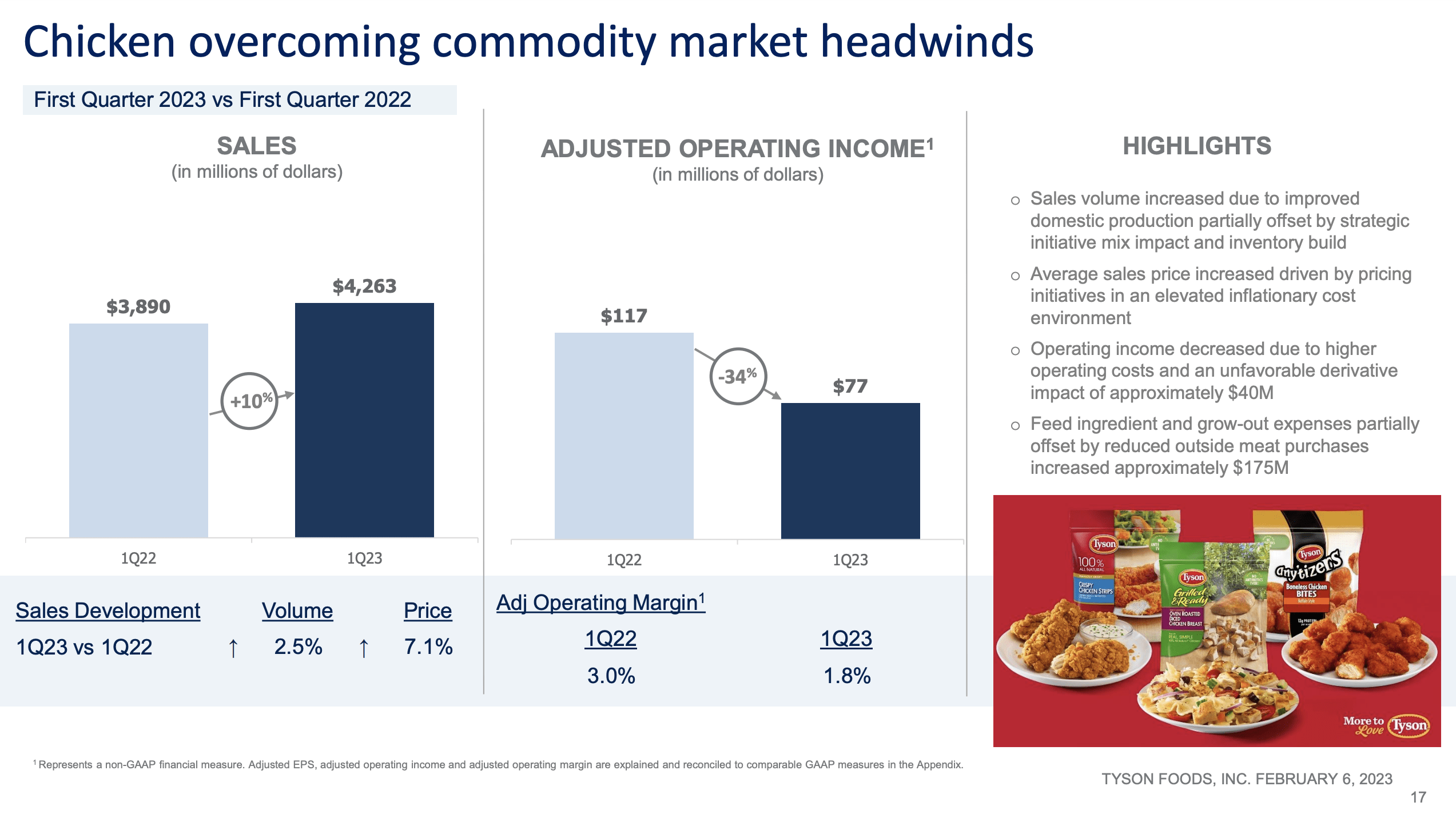

Tyson Chicken (Company Presentation)

Tyson has been on a long journey to restore its chicken operation to its former dominance, and top line sales in the division were up a solid 10% year over year as consumers shun more expensive beef cuts and stock up on chicken. Costs for the company were another body blow to earnings, however, with margins collapsing 35%. Once again, the company was impacted by its derivative positions which, like pork, cut negatively against operating income, this time to the tune of $40 million.

Longer Term Concerns

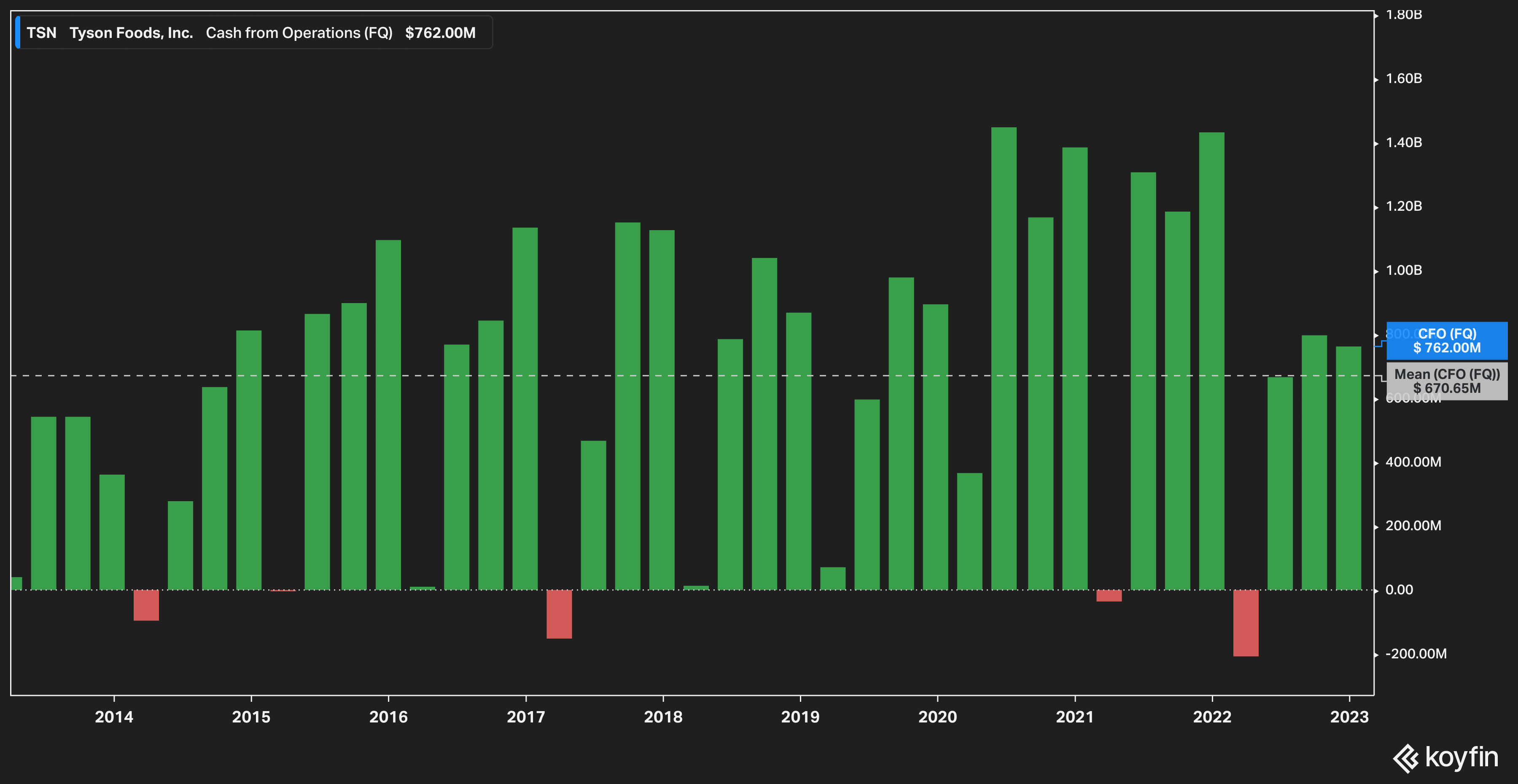

With a tough quarter in the rearview mirror, we are unfortunately left to conclude that more pain is ahead for investors. Let’s look at Tyson’s operating cash flow over the last ten years.

Koyfin

In Q1, Tyson delivered operating cash flow of $762 million, but a quick glance at the chart shows that the company’s cash-generating abilities have been squeezed in the last year.

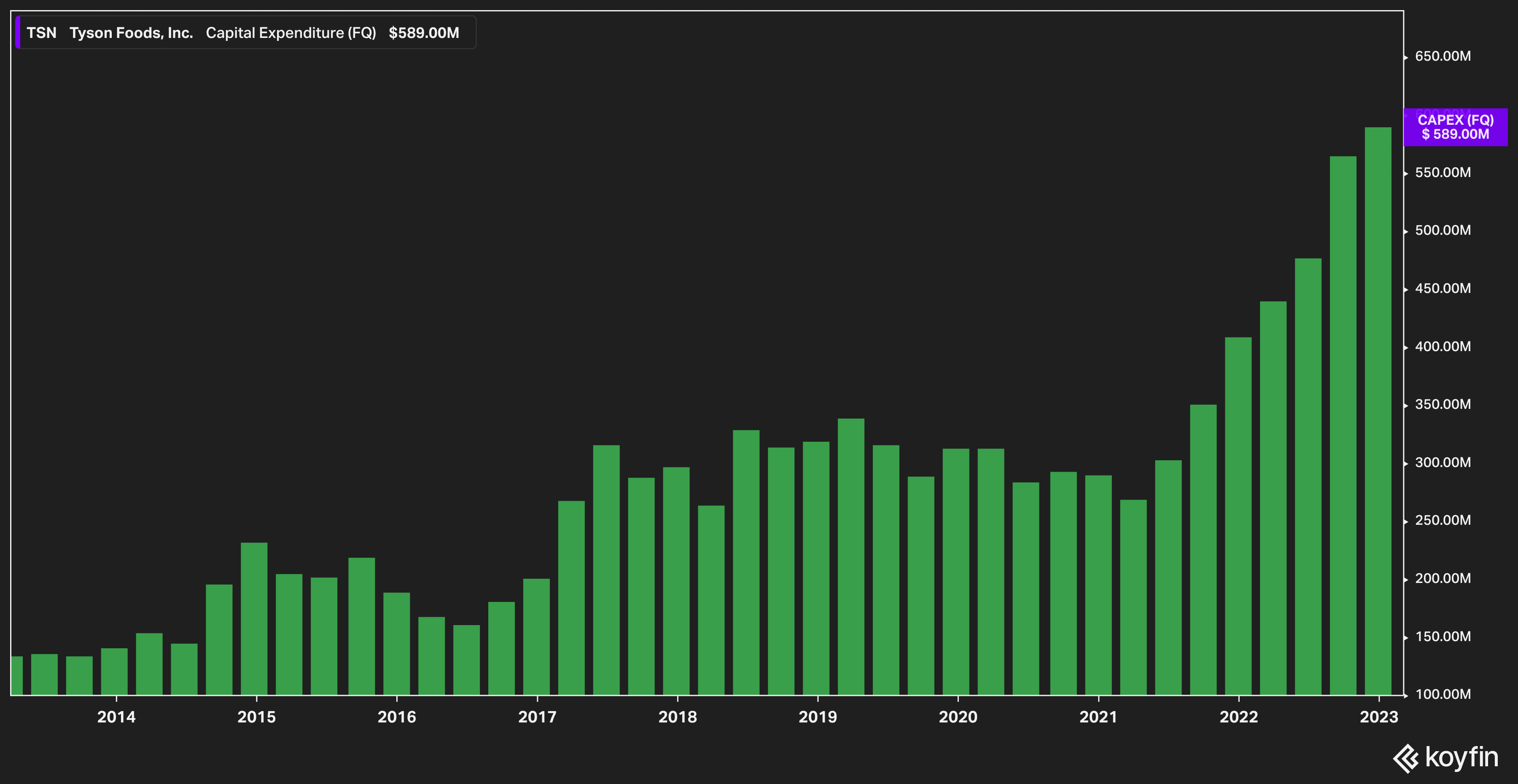

When we compare this against the company’s capital expenditures, we see that free cash flow has been similarly squeezed.

Koyfin

It’s clear to see that in the last two years, Tyson has embarked on a capital expenditure campaign unlike any other the company has had before. These expenditures largely relate to automation of operations, and the company has no plans to slow down–CFO John Tyson reiterated that the company expects to incur $2.5 billion in capital expenditures in FY 2023.

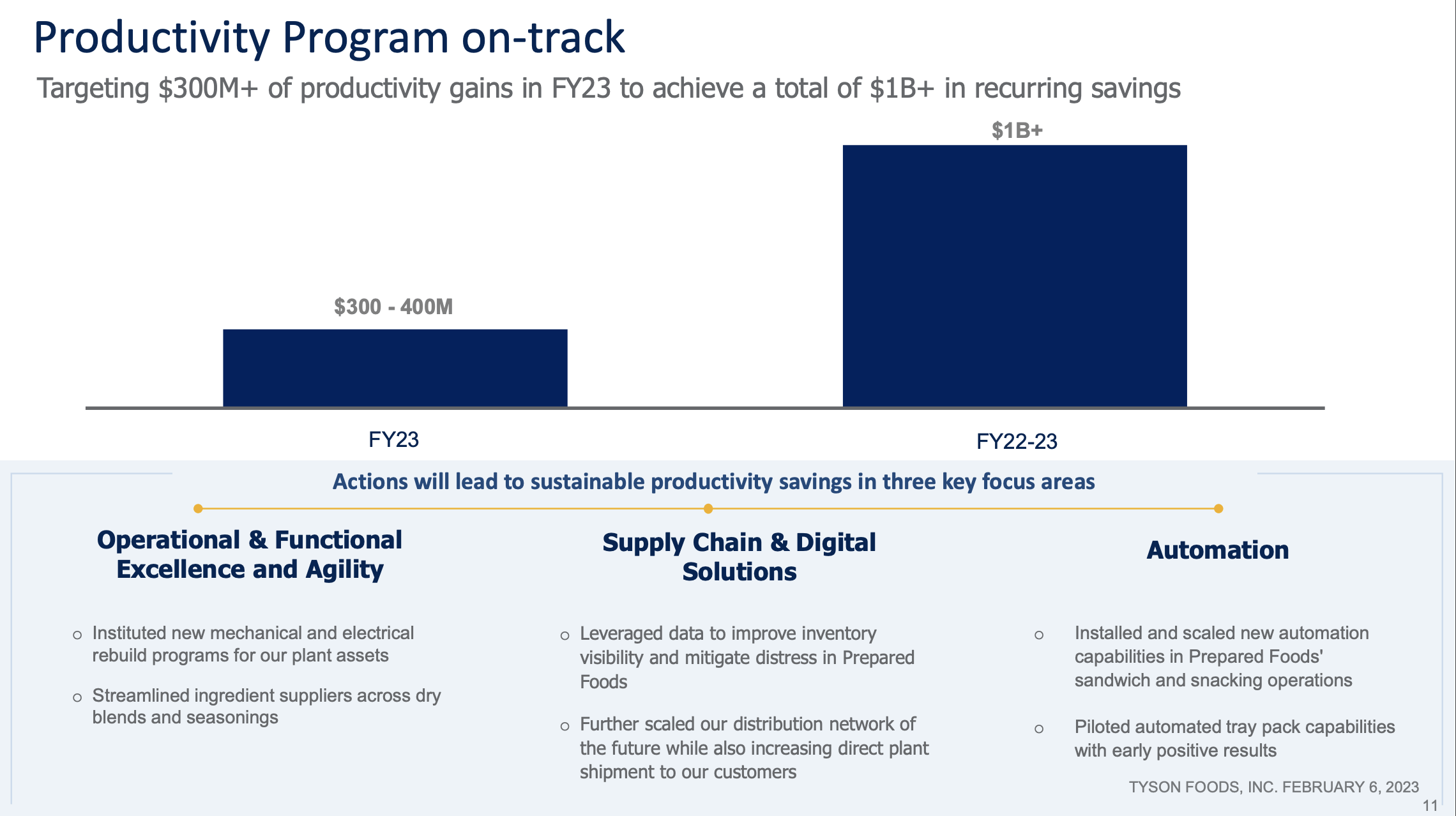

Company Presentation

The company estimates that these rising capital expenditures will begin to pay off in the near future–generating $1 billion in recurring operational cost savings after FY 2023.

This may be true–the results of the expenditures remain to be seen. However, we are of the opinion that these costs are coming at a precipitously bad time for the company.

As we pointed out previously, Tyson’s margins are traditionally thin. We also believe that the results from this quarter are not a fluke, but that the same forces which created the disappointed Q1 results will persist.

The job market remains strong, and businesses continue to de-globalize supply chain, which raises costs. These large-scale forces are powerfully inflationary, and will continue to provide headwinds for Tyson, we believe, for at least the remainder of this FY. To boot, interest rates are forecasted to continue to rise, which lowers the attractiveness of financing these investments.

Thus, while the effort itself of streamlining the business is laudable, the timing is, in our view, quite bad. Unfortunately, investors won’t have the ability to vote their views on the company’s direction as the Tyson family exerts majority control over the stock. The only way investors can express an opinion on Tyson, then, is to buy or sell.

The Bottom Line

Tyson Foods, Inc. delivered tough results for Q1 that drove the stock to fresh lows. We believe that the headwinds that Tyson experienced will continue, and that its plans to embark on multi-billion spending plans to improve operations will have the potential to severely impact investors over the next 12-24 months.

We concede that if macro conditions shift dramatically, much of our concerns will be relieved. As of this writing, however, there appears to be few signs of that happening.

Further, it is no guarantee that Tyson’s promised savings will occur. Switching operational modes from manual to automated incurs new costs that didn’t exist before–maintenance, servicing, down-time–and these new expenditures will have to be accounted for. If the company cannot deliver great execution in this CAPEX cycle–while it faces multiple business headwinds, mind you–then investors could feel the pain.

Tyson Foods, Inc. may be a tasty opportunity in the future, but today we will wait on the sidelines and observe management’s ability to execute.

Be the first to comment